Wall Street just put stocks on a blockchain

Hey, it’s Marc,

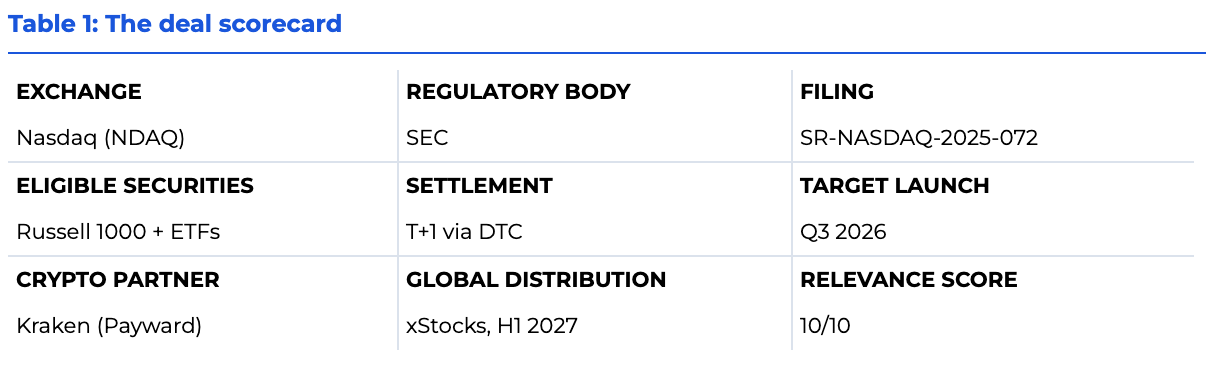

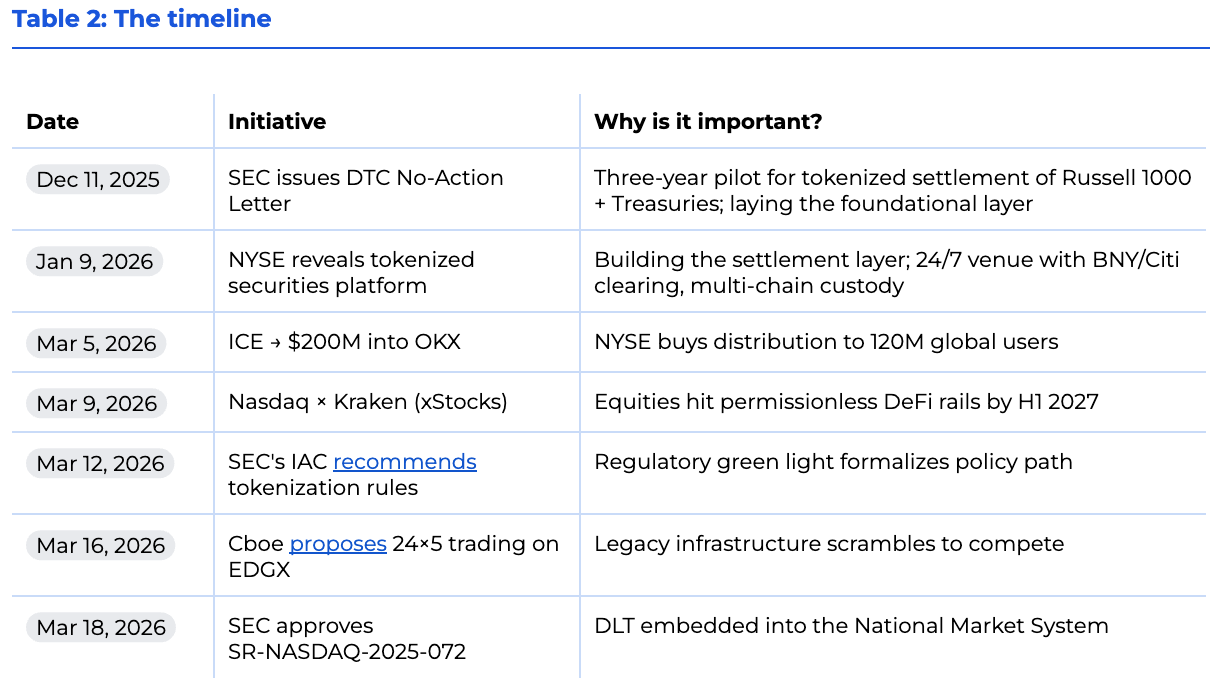

For most of its history, buying a stock meant trusting a long chain of banks, brokers, and clearinghouses to sort out who owns what, a process that still takes two full days to complete. On March 18, the SEC approved Nasdaq to trade and settle U.S. equities as blockchain tokens, baked directly into the National Market System. [FILING]

The Signal: The $126 trillion global equity market has started moving on-chain. The last time American equity markets underwent a structural shift of this magnitude was decimalization in 2001.

👉PRO: Download the PDF below

Marc Baumann

Marc BaumannWhat happened

The SEC approved SR-NASDAQ-2025-072 (rule change proposal by the Nasdaq to enable the trading of securities in tokenized form) on March 18, allowing Nasdaq to trade and settle eligible U.S. securities as blockchain tokens via the DTC’s Digital Omnibus Account.

Initial scope: Russell 1000 stocks, S&P 500 and Nasdaq-100 ETFs.

Tokens are minted one-to-one against real shares held at Cede & Co., tracked via the DTC’s LedgerScan system with the same CUSIP (uniquely identify North American financial securities (stocks, bonds, municipal bonds) to facilitate accurate trading, clearing, and settlement), voting rights, dividends and order book without price fragmentation. First trades could occur by Q3 2026.

Stepping back: Nasdaq originally filed SR-NASDAQ-2025-072 in September 2025, then replaced it entirely with Amendment No. 2 on January 30, 2026.

Zooming in: The groundwork was laid on December 11, 2025, when the SEC’s Division of Trading and Markets issued a no-action letter to DTC permitting a three-year voluntary tokenization pilot for Russell 1000 securities, major index ETFs, and U.S. Treasuries. That letter gave DTC the regulatory cover to build. Nasdaq’s approval gives it the first venue to go live. [CEO notes]

Meanwhile, Intercontinental Exchange (NYSE’s parent) dropped $200M into OKX, 120M users, 14.3% global derivatives market share, targeting H2 2026 for tokenized NYSE equity access. [CEO notes]

Nasdaq signed a parallel deal with Kraken (Payward), targeting H1 2027 via Kraken’s xStocks framework, which has already cleared $25B in transaction volume with 85,000+ holders. [CEO notes]

By the data: The global equity market is valued at approximately $126T. NASDAQ comprised 29.5% of U.S. equity options (equity derivatives) in Q4 2025 and 49.1% of industry on-exchange volume in cash equities.

Why it matters

- Nasdaq chose integration. NYSE is building a separate venue for tokenized securities, subject to its own regulatory approval. Nasdaq took a fundamentally different approach: same order book, same price, same ticker. This eliminates the fragmentation risk that has killed every prior attempt at “alternative” trading venues. There is no liquidity split, or basis split or price dislocation between tokenized and non-tokenized shares. Nasdaq’s model preserves the single most valuable feature of its exchange: the depth of its existing order book.

- The new combination: traditional + crypto exchanges. Nasdaq picked Kraken and NYSE picked OKX. And, this is not just any other alliance. Kraken’s xStocks platform has already processed $25B in tokenized equity volume since June 2025, with $3.5B on-chain and 80,000+ unique holders. OKX brings 120M accounts and global distribution to ICE. The real race is which exchange-crypto pair captures the 24/7 global trading flow first. Nasdaq gets U.S. production rights now; NYSE gets the larger international user base. While CME is going to offer crypto derivatives trading 24 hours a day, 7 days a week, the traditional stock is moving at the same pace. Quantitative funds are already modeling this liquidity to time premium. The edge is distribution and time-to-market.

- The weekend gap between the market and the infrastructure. When Nasdaq closes at 4PM Friday, tokenized shares keep trading. But arbitrageurs can't mint or redeem tokens with the DTC after hours, so prices float freely. A weekend macro shock could drive violent divergence between the token price and Friday's closing NAV. Researchers at the Federal Reserve Bank of New York have flagged exactly this run-risk dynamic in tokenized investment funds.

Investor alpha

The moment tokenized equities can be posted as margin in 24/7 DeFi protocols, the total addressable market for stablecoins and blockchain-native custody explodes. The alpha also extends from traditional exchanges to underlying stablecoin settlement layers and the custodians holding the physical keys. The right trade is going long the two things tokenization structurally rewards: distribution scale and settlement infrastructure.

- Long Intercontinental Exchange (ICE): By securing a $200M stake in OKX, ICE bypassed a decade of retail acquisition costs. As they funnel tokenized NYSE equities to 120M global users by H2 2026, their distribution dominance will command a massive premium over pure-play traditional exchanges. 👉 Trade on Robinhood

- Long Standard Chartered (STAN.L): Standard Chartered’s program lets institutions trade crypto globally while keeping their actual assets held separately, in a major regulated bank, legally ring-fenced so that if the exchange goes under, the assets don’t go with it. That structure, known as off-exchange collateral mirroring, is exactly what every serious institution needs to enter this market. And Standard Chartered is one of the only G-SIB-tier banks offering it. 👉 Trade on Robinhood

- Long BlackRock (BLK): Tokenized stocks need tokenized cash to settle. You can’t finalize a trade in seconds if payment still takes two days to clear through a traditional bank, so this new market runs on stablecoins, digital dollars that move instantly on-chain. Stablecoins need reserve management. USDC (USD Coin), the management of a significant portion of its reserves is handled by BlackRock. So here’s the trade: as tokenized equity markets grow, they need more stablecoin liquidity. More stablecoins in circulation means a larger pool of Treasuries backing them. A larger pool means more assets under management, and more management fees flowing to BlackRock, quietly, in the background. 👉 Trade on Robinhood

- Long Coinbase: Coinbase Custody is the dominant institutional digital asset custodian in the U.S. As tokenized equities require registered wallet infrastructure and DTC-approved custody solutions, Coinbase is structurally positioned to capture a portion of the $126T market’s custody revenue layer, on top of existing exchange and stablecoin (USDC). 👉 Trade on Robinhood

Our take

In 98 days, the U.S. moved from a no-action letter to a production-approved tokenized settlement system. That’s a regime change.

The infrastructure race is already underway. NYSE is building multi-chain custody with BNY and Citi. Nasdaq is bridging permissioned and permissionless markets through Kraken. Whoever controls these rails controls something more valuable than settlement, every tokenized trade generates a data trail of wallet addresses, blockchain preferences, and settlement patterns. The post-trade layer is becoming an intelligence layer.

Regulation has flipped from blocker to enabler, but it’s still fragile. Chairman Atkins and Commissioner Peirce are pushing the SEC Crypto Task Force; the CFTC has new leadership moving in the same direction. But a future SEC chair can reverse course. What locks it in is legislation, specifically, something like the Clarity Act.

And even with the right rules, execution is hard. ICE’s Bakkt proved that policy wins don’t automatically translate into working systems. Brokers have to be onboarded. Blockchain and wallet compatibility has to be verified trade by trade. The gap between approval and adoption is where most of this gets decided.

Watchlist:

- Mar 1–2: Crypto Expo Europe (Bucharest)

- Mar 11: US CPI (Feb) release – critical for Fed rate cut expectations

- Mar 17–18: DC Blockchain Summit (Chamber of Digital Commerce)

- Mar 18: FOMC Interest Rate Decision & Summary of Economic Projections

- Apr 28–29: FOMC meeting. Second rate decision window

- Jul 1: MiCA universal deadline

- Q1-Q2 2026: SEC final decision on Nasdaq tokenized trading rule change (SR-NASDAQ-2025-072)

- H2 2026: DTCC tokenization pilot launch

That’s it for now.

Missed last week? Access all our CEO notes here.

Marc & Team