The GENIUS Act’s first victims

The traditional banking system just lost control of its most important moat: exclusivity. For decades, the OCC’s charter approval process was the ultimate gatekeeping mechanism, determining who could offer trust services and custody to America’s institutions.

But on December 12, 2025, the regulator changed the rules. It approved five national trust bank charters for digital asset entities, cracking open an $85T institutional custody market without traditional banks’ permission. [RELEASE]

Let’s unpack.

Download the PDF

Today’s Market signals

- Aave, the biggest DeFi lending protocol, is entering governance war. Link

- Pro-crypto Michael Selig sworn in as new CFTC Chair. Link

- JPMorgan is considering offering crypto trading for institutional clients. Link

Get your brand in front of 100k+ decision makers in digital assets.

What happened

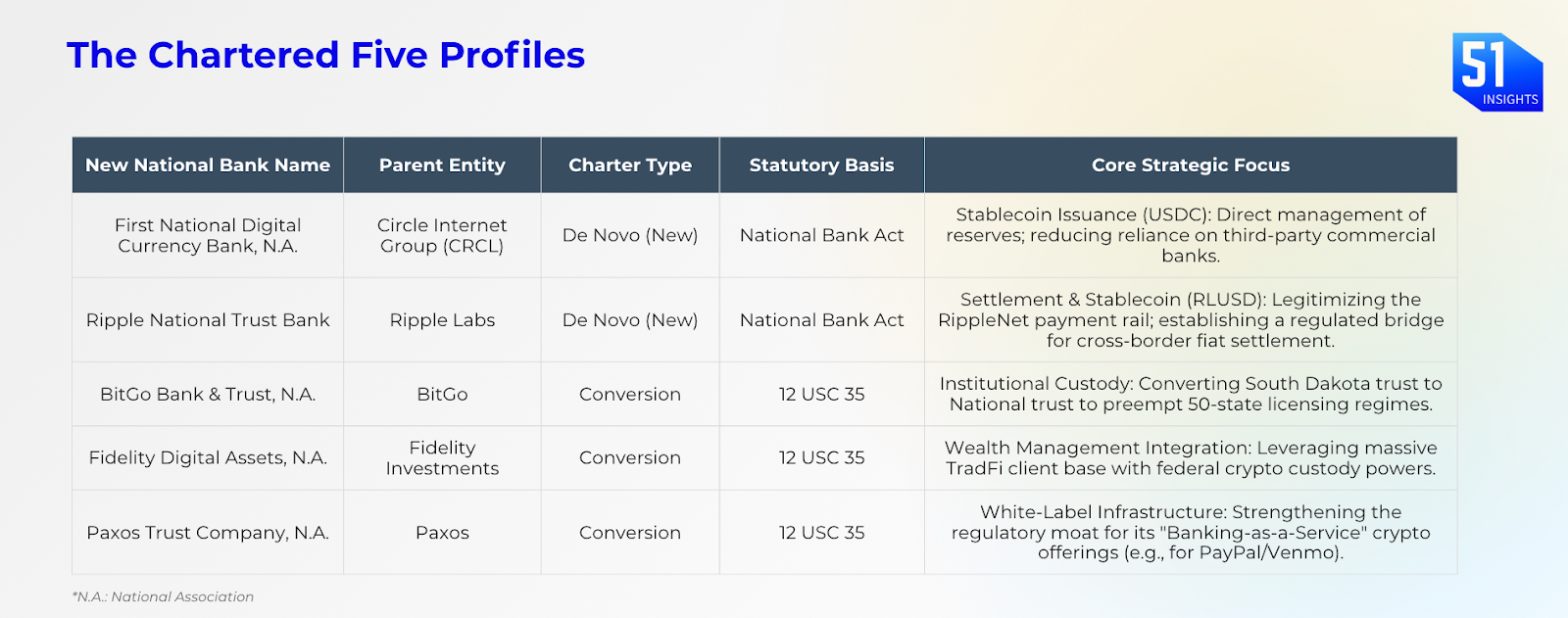

The U.S. banking regulator OCC (Office of the Comptroller of the Currency) has approved five crypto-focused firms to operate as national trust banks, pending final conditions. This move is the executive implementation of the GENIUS Act, passed in July 2025. The approvals include:

New charters:Ripple and Circle (operating as “First National”)BitGo, Fidelity Digital Assets, and Paxos converted existing state charters into federal ones under 12 U.S.C. § 35.

These banks are “narrow banks”—they do not lend or gamble with customer funds. They must maintain full reserve backing, typically in U.S. Treasuries, and hold enough cash to cover months of operating expenses to ensure an orderly wind-down if needed.

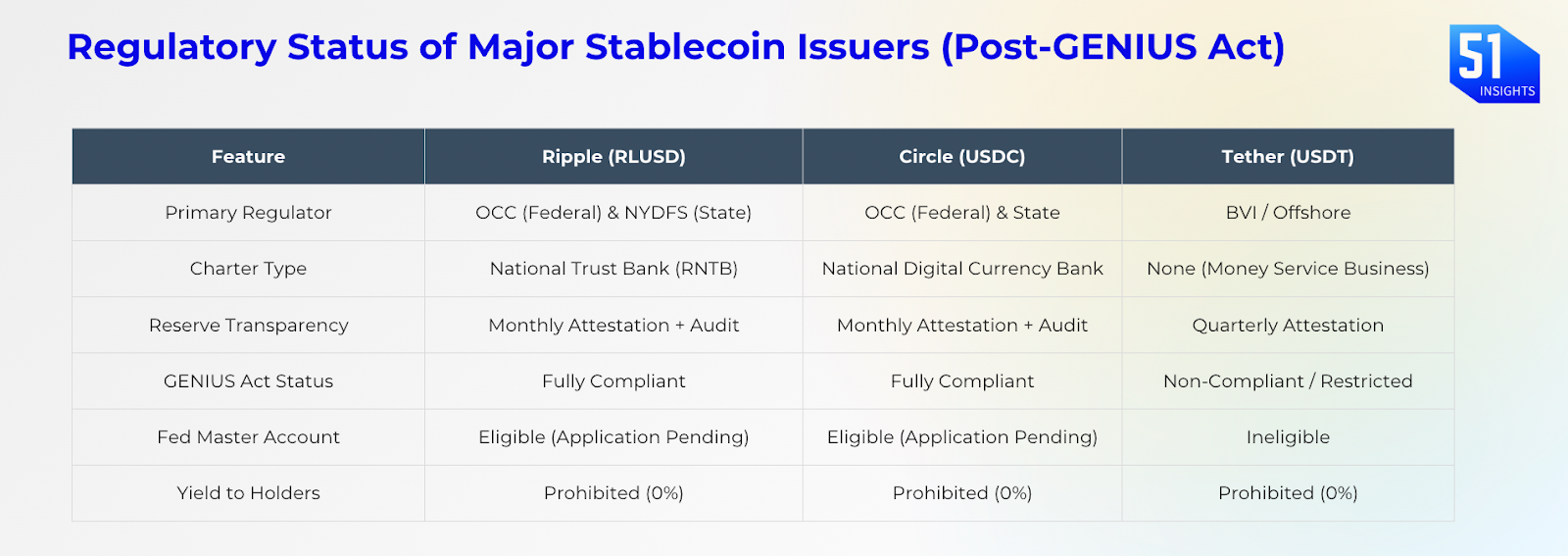

- Circle: By launching a brand-new national bank and calling it “First National,” Circle is framing USDC not as just another product, but as a federally aligned digital dollar, with the bank directly managing its reserves in New York.

- Ripple: For Ripple, the charter seals years of regulatory battles. Its national trust bank will manage RLUSD reserves under both federal and New York oversight, creating a level of credibility and scrutiny most offshore rivals cannot match.

- Notably, Coinbase’s application stalled due to fierce opposition from groups like the Independent Community Bankers of America (ICBA), who raised concerns over mixing trading, custody, and yield activities.

- Tether took a different route: Unable to qualify for a U.S. charter, it created a separate, U.S.-based stablecoin (USAT) run through regulated partners, while keeping its main business offshore. The strategy is simple: comply just enough to stay in the U.S., and continue scaling globally where rules are looser.

Why this is allowed: Regulators are treating stablecoin management like a traditional trust service. It’s an old legal framework being adapted to fit a new type of money.

The threat

Traditional banks despise the stablecoin model because it represents a “narrow bank,” an institution that takes deposits (via stablecoin purchases) and parks them in Treasuries, bypassing the lending function of commercial banks.

- Liquidity drain: The ICBA warns that if billions of dollars move from commercial bank deposits to Circle/Ripple Trust Banks, it drains the liquidity available for small business loans and mortgages.

- Regulatory arbitrage: The Bank Policy Institute argues that these trust banks get the benefits of the banking system (preemption, potentially Fed access) without the obligations (CRA lending, deposit insurance premiums).

Incumbent moves: On Dec 15, JPMorgan launched the “My OnChain Net Yield Fund” (MONY) on Ethereum, allowing tokenized investment. [RELEASE]

That’s basically: “We don’t need a crypto bank charter; we are the bank, and we will adopt the tech.”

Visa also launched a “Stablecoin Advisory Practice” to help its bank clients integrate stablecoins on Dec 15. [NEWS]

Why it matters

- Regulation by integration: This puts major digital-asset players under the same federal framework as traditional trust banks. The regulator is signalling that crypto custody and settlement can sit inside the mainstream banking system, not outside it, with the creation of First National Digital Currency Bank (Circle) and Ripple National Trust Bank.

- Valuation driver: The charter is a massive long-term value driver. It reduces OpEx (by consolidating compliance) and solidifies Ripple’s and Circle’s status as a regulated issuer and USDC and RLUSD as the safe stablecoins. They are now technically peers of JP Morgan and Bank of America, creating significant friction and competitive response from the incumbents.

- ROI of political spending: For years, the SEC’s lawsuit against Ripple (alleging XRP was an unregistered security) cast a pall over the company. The lawsuit was settled in August 2025 after the passage of the GENIUS Act. Ripple spent heavily on politics, and it paid off. By backing pro-crypto candidates through Fairshake and hiring Ballard Partners, a firm closely tied to the Trump administration, Ripple ensured direct access as new rules were written. That influence coincided with the GENIUS Act and the appointment of Jonathan Gould as Comptroller, giving Ripple the regulatory clarity it had long sought.

Investor Alpha

- Circle ($CRCL): Many investors view Circle as the primary beneficiary of the “First National” launch in Q1 2026. By operationalizing as a bank, Circle is expected to expand margins significantly by retaining a higher percentage of net interest income from reserves that previously went to partner banks.

- Ripple (XRP): If RLUSD gains traction within the new National Trust Bank framework, it creates a “regulated leg” for ODL (On-Demand Liquidity) transactions. Some analysts suggest XRP is undervalued relative to its new status as a peer to JPMorgan in the payments corridor.

- The Master Account Catalyst: Watch for Circle and Ripple to apply for Federal Reserve Master Accounts in early 2026. Approval would allow them to settle directly with the Fed, bypassing the commercial banking system entirely and effectively making them “Tier 1” financial infrastructure.

Watchlist:

- Dec: USAT launch by Tether (expected)

- Dec: Clarity Act (H.R.3633) Senate vote (expected)

- Dec 31: Europe’s MiCA full enforcement (Austria, Germany, and Spain) ends

- Jan 1: Basel Committee crypto capital standards implementation in Hong Kong

- Jan’26: SEC Crypto Innovation Exemption

- Jan’26: Spot crypto ETF approvals for altcoin

- Q1’26: Kraken IPO

- Q1’26: Hong Kong Stablecoin licensing

- Q1’26: Singapore Stablecoin framework

That’s it for now.

Marc & Team

Download the PDF