the SEC sorts its tokens

Hey, it’s Marc,

For the first time ever in their combined 183 years of existence, the SEC and CFTC published a joint document agreeing on what crypto actually is.

They named 16 specific tokens as commodities. They said staking isn't a security. And they formally acknowledged that a security can stop being a security.

That last part is the one that changes everything. [RELEASE]

The Signal: Most crypto tokens aren’t securities by default, and their regulatory status depends on how they’re used, and can change over time.

👉PRO: Download the PDF below

Marc Baumann

Marc BaumannAn exclusive offering for 51 readers:

✅ Register for Consensus Miami, May 5-7, 2026, and get in the room where the people moving that money actually meet.

🎟️ 20% Discount Code: MARC

🔗 Auto-applied discount link: https://go.coindesk.com/3NLCAAd

(get up to $900 off)

I’ll be there too, and I want to meet you!

What happened

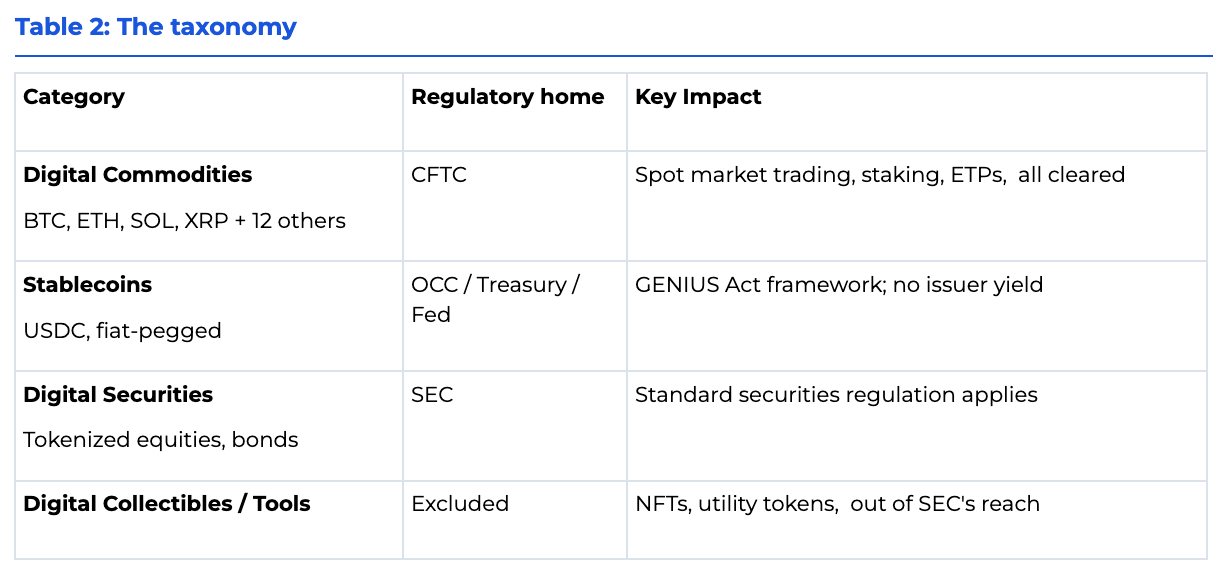

The SEC and CFTC issued a landmark 68-page joint interpretation on March 17, 2026, establishing the most significant overhaul of U.S. capital markets infrastructure since the Securities Act of 1933. The release introduces a five-pillar token taxonomy, explicitly names 16 crypto assets as digital commodities, and formally ends the SEC’s “regulation by enforcement” doctrine.

It is a final agency statement of position, effective upon publication in the Federal Register.

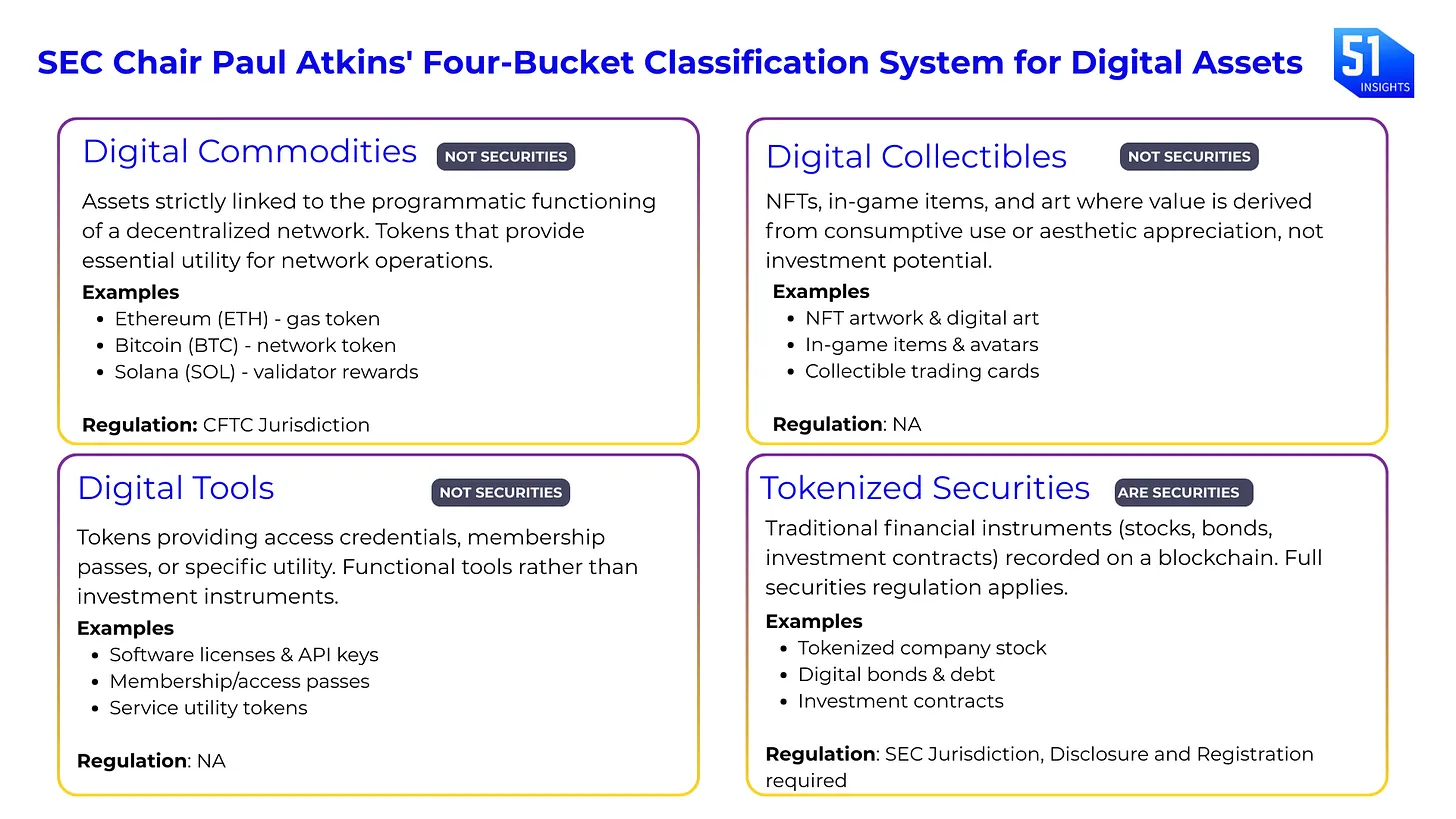

The interpretation establishes five token categories: digital commodities (BTC, ETH, SOL, XRP, DOGE, ADA, AVAX, LINK, DOT, HBAR, LTC, BCH, and others), digital collectibles (NFTs, meme coins), digital tools (memberships, credentials, identity badges), stablecoins (non-securities under the GENIUS Act), and digital securities (tokenized traditional securities, which remain under SEC oversight).

Watch our recent podcast with SEC Commissioner Hester Peirce:

Stepping back: Six days earlier, on March 11, the SEC and CFTC signed a Memorandum of Understanding establishing a Joint Harmonization Initiative to coordinate oversight across policymaking, examination, and enforcement.

Zooming in: The taxonomy is the product. The interpretation provides explicit guidance on staking, mining, airdrops, and token wrapping. Protocol staking and mining are classified as “administrative or ministerial” activities, not securities transactions. Airdrops, because they involve no investment of money, fail the Howey test. Wrapped tokens derive value from the underlying asset, not from managerial efforts.

Meme coins got the same legal status as Bitcoin. By classifying Dogecoin and Shiba Inu as commodities, the SEC formally said: decentralization and market-driven price discovery matter more than “utility.”

What they’re saying: The timing is great. We just interviewed the SEC Commissioner and the crypto mum Hester Peirce at Fiftyone Podcast. She said,

“We’ll help people understand how we’re thinking about what an investment contract is, when it ceases to travel with a token.”

Previously, the digital assets were divided into four buckets and now it has also expanded to Stablecoins, with Genius Act framework and OCCas the main regulator.

Here’s what this unlocks…

- The Howey test just got an expiration date. The SEC now formally recognizes that investment contracts can terminate. A token sold in an investment contract does not remain a security forever. Once the issuer fulfills its promises, or the network reaches maturity and control disperses, the Howey test no longer applies. Commissioner Peirce framed it well:

“A token is no more a security because it was once part of an investment contract than a golf course is a security because it used to be part of a citrus grove investment scheme.” - Tokenization is growing across all domains. Broadridge’s Distributed Ledger Repo (DLR) platform is now processing $362B in average daily volume. Standard Chartered and DBS Bank are getting stablecoin licenses in Hong Kong. Mastercard is acquiring BVNK. We are entering the era of atomic settlement. With these regulatory clarity, the acquisitions and partnerships will move even faster.

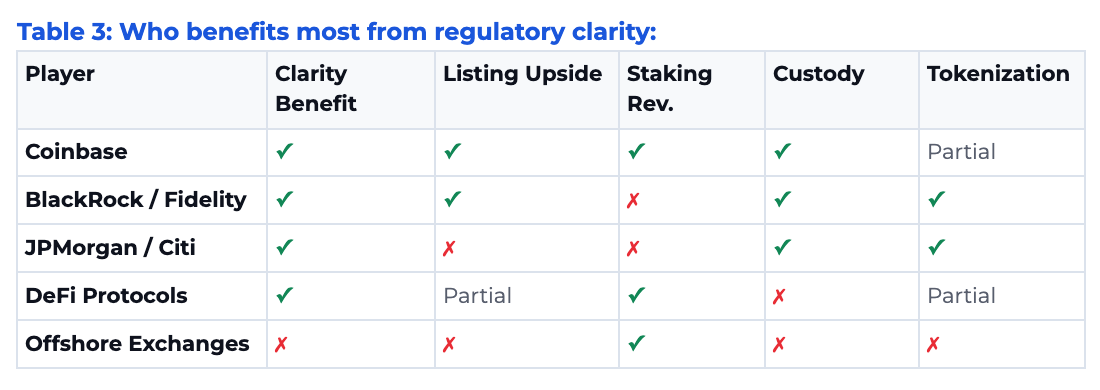

- Staking is now an institutional product. The SEC explicitly said staking is "administrative or ministerial," not a securities transaction. This is the precondition for yield-bearing ETPs. Expect staking-enabled ETH and SOL ETFs within months. The revenue model for exchanges, custodians, and asset managers just expanded. Coinbase, Lido, and Figment are the first-order beneficiaries.

Investor alpha

Global banks will now focus on capturing the liquidity.

- HSBC: Building proprietary, permissioned ledgers via HSBC Orion. They recently facilitated a $1.3B digital green bond for Hong Kong and hold over $1B in tokenized physical gold.

- Standard Chartered (The Bridge): Deploying an agile venture model via SC Ventures. Their platforms, Zodia Custody and Libeara, just crossed $1B in on-chain real-world assets (RWAs), including the AAA-rated ULTRA tokenized T-bill.

- Long Ethereum / Solana Staking Proxies: The SEC explicitly stated staking isn’t a security offering. Expect a tsunami of “Staking-as-a-Service” ETPs. Many investors will aggressively rotate out of pure spot ETH/SOL ETFs into yield-bearing wrappers to capture that native protocol revenue. 👉 Trade on Robinhood

Our take

This is the most important U.S. crypto regulatory event since the Bitcoin ETF approvals. Now, the space is moving towards infrastructure partnership and acquisitions and compliant infrastructure buildout. BlackRock, JPMorgan, Fidelity, and the entire tokenization stack are the first-order beneficiaries.

The most underappreciated part of the March 17 interpretation is the “investment contract lifecycle” formalization. The SEC now acknowledges that a security can stop being a security. It creates a defined regulatory exit for early-stage token investors who previously had no clean path to secondary market distribution. This changes everything from DeFi to VCs. HSBC and Standard Chartered are the two most important banks you’re probably not watching closely enough, beyond US regulations.

Keep in mind, though: This is an interpretation, not legislation. A future SEC chair can reverse it. The CLARITY Act, which would make this permanent, is still stuck in the Senate Banking Committee. And the 400-page rulemaking coming in two weeks could introduce friction the interpretation doesn’t anticipate.

Watchlist:

- Mar 1–2: Crypto Expo Europe (Bucharest)

- Mar 11: US CPI (Feb) release – critical for Fed rate cut expectations

- Mar 17–18: DC Blockchain Summit (Chamber of Digital Commerce)

- Mar 18: FOMC Interest Rate Decision & Summary of Economic Projections

- Apr 28–29: FOMC meeting. Second rate decision window

- Jul 1: MiCA universal deadline

- Q1-Q2 2026: SEC final decision on Nasdaq tokenized trading rule change (SR-NASDAQ-2025-072)

- H2 2026: DTCC tokenization pilot launch

That’s it for now.

Missed last week? Access all our CEO notes here.

Marc & Team