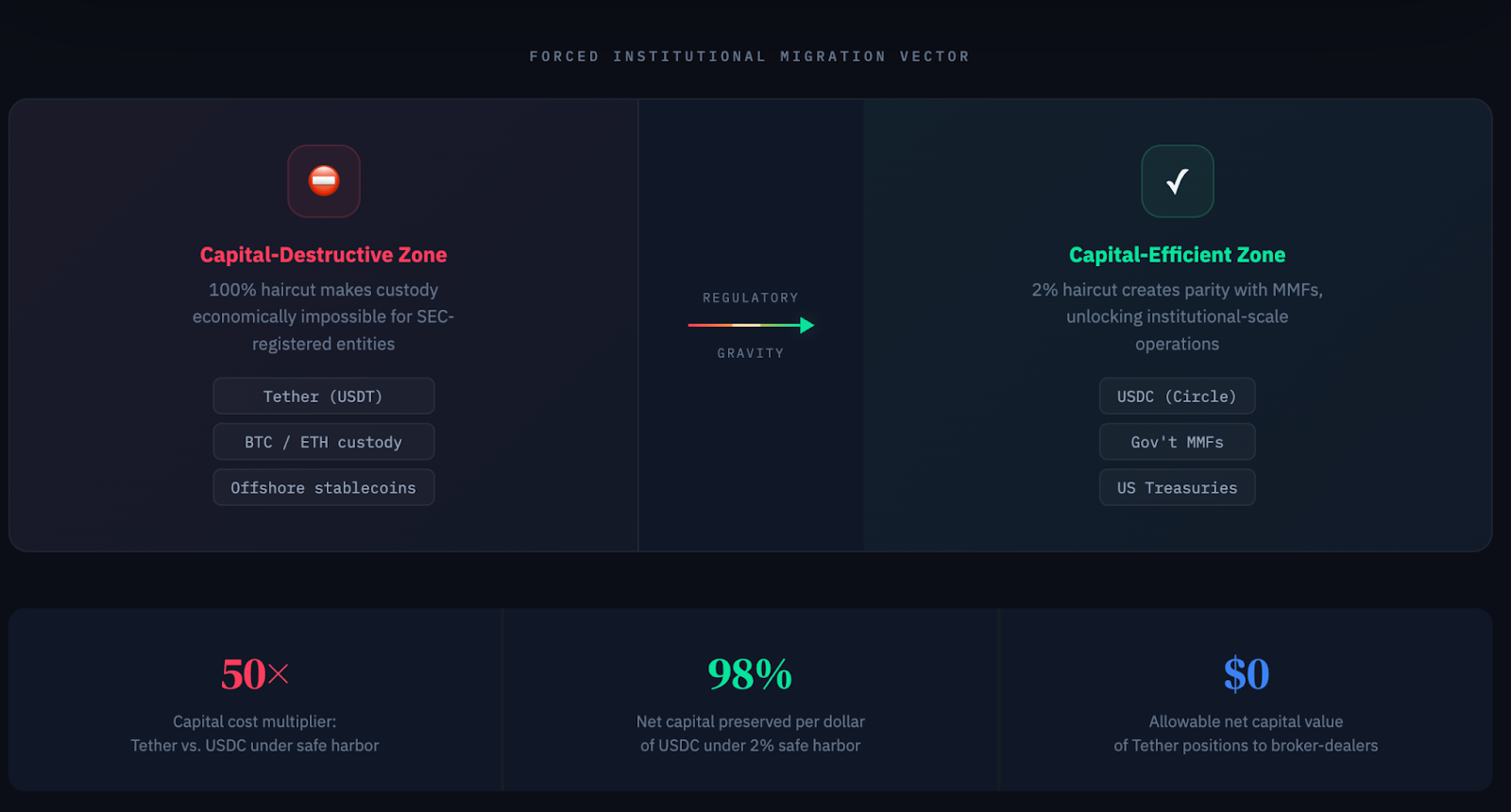

From 100% to 2%

You know what’s more powerful than a 1,000-page regulation? A two-page FAQ.

On February 19, the SEC’s Division of Trading and Markets quietly dropped guidance that slashes the capital charge on stablecoins from 100% to 2% for broker-dealers.

That’s the same haircut as money market funds. This makes stablecoins near-cash working capital and it might be the single most important regulatory shift for Wall Street in 2026. [RELEASE] [FAQs]

👉PRO: Download the PDF at the bottom

👉Need it simple? Read my post here.

What happened

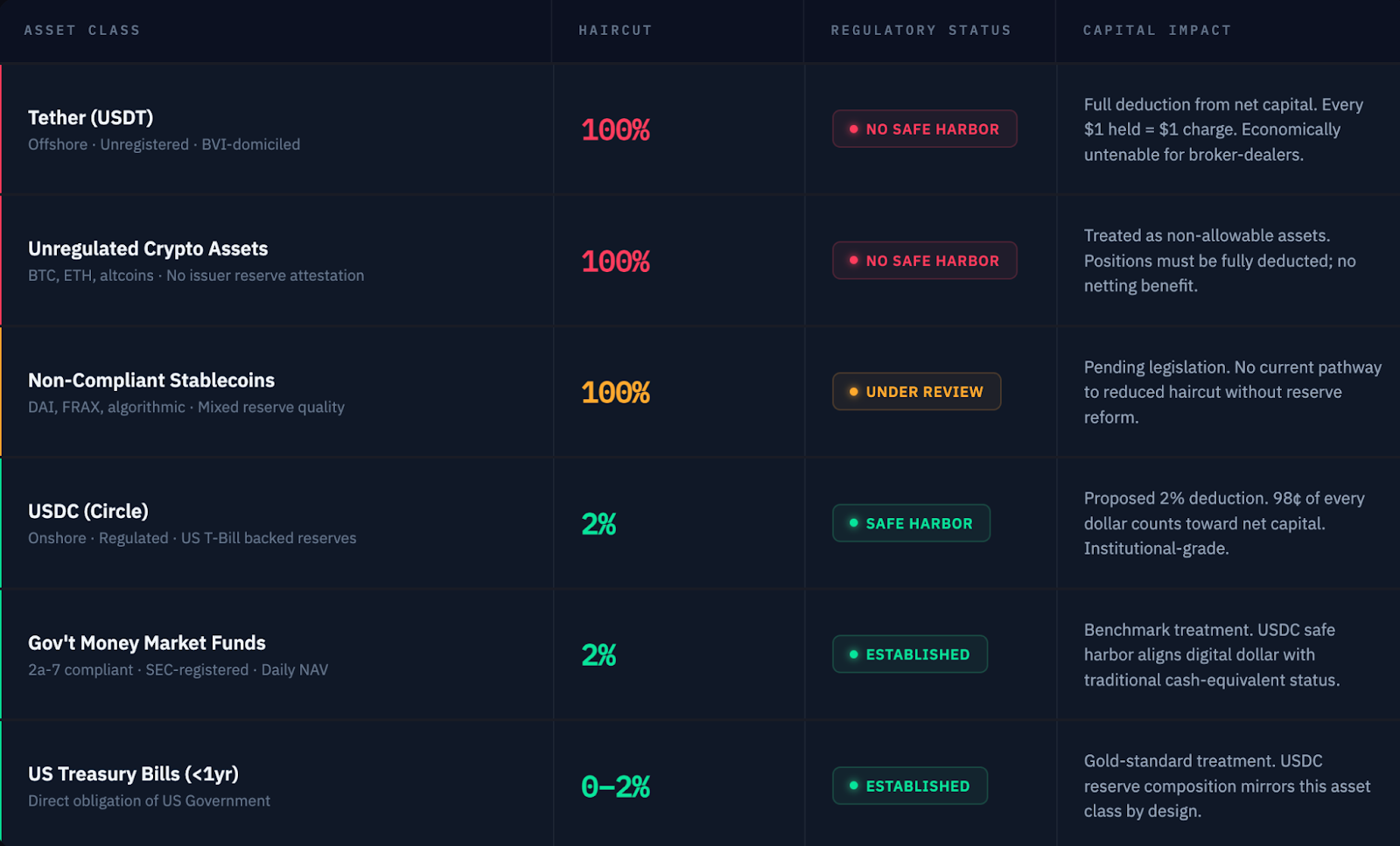

The SEC issued an FAQ clarifying that broker-dealers can now apply a 2% capital haircut to qualifying payment stablecoins under Exchangule 15c3-1, the net capital rule that governs how much liquid capital Wall Street firms must hold. [RELEASE]

But there’s a catch: the “no-netting” sting. The 2% charge applies to the gross market value of the greater long or short position, preventing delta-neutral offsetting. To qualify, stablecoins must meet strict GENIUS Act criteria: U.S.-regulated issuers, 100% USD/T-bill backing, and monthly AICPA-standard attestations.

Zooming in: Under Rule 15c3-1 (Net Capital Rule), broker-dealers must apply risk-based “haircuts” (deductions) to balance sheet assets when computing regulatory net capital, ensuring liquidity buffers against potential losses. Previously, most stablecoins lacked “ready market” status, triggering a 100% haircut that excluded them entirely from capital calculations.

Here’s the math and why it’s a big deal:

→ A 100% haircut means a firm holding $100M in stablecoins counts $0 toward capital. Every dollar of stablecoins was dead weight.

→ A 2% haircut means that same $100M counts as $98M.

Be smart: Qualifying stablecoins must be USD-denominated, backed by cash/short-term Treasuries (per 12 U.S.C. 5903 standards), issued by regulated entities (e.g., state money transmitters), with public redemption policies and monthly CPA-attested reserves; post-GENIUS Act, they align with that law’s “permitted payment stablecoin” definition.

Marc Baumann

Marc Baumann

Why 2%: The logic is simple. Stablecoin reserves are T-bills, cash, and short-duration government paper: the exact same assets sitting inside a government money market fund.

Commissioner Hester Peirce called the old 100% charge “unnecessarily punitive.” The 2% captures residual redemption risk, operational risk, and potential de-peg scenarios, but treats stablecoins as fundamentally low-risk.

What they’re saying:

“Stablecoins are essential to transacting on blockchain rails. Using stablecoins will make it feasible for broker-dealers to engage in a broader range of business activities relating to tokenized securities and other crypto assets.”

– SEC Commissioner Hester M. Peirce

And the downstream effect is massive. If broker-dealers can hold stablecoins cheaply, they can

- settle trades on blockchain rails

- offer tokenized securities

- move money 24/7 instead of waiting for banking hours.

Devil’s advocate: Of $35T in 2025 stablecoin volume, only $390B represents genuine economic activity (remittances and payroll), while 92% of stablecoin volume remains crypto trading.

Marc Baumann

The analysis that follows is for PRO subscribers.

You just saw the rule change. What you haven't seen is who wins, who's dead, and how to position before the rest of the market catches up. PRO ONLY:

- Why it matters (instant settlement unlock, USDT kill switch, the netting catch, banks terrified)

- Investor Alpha (Circle, Coinbase, onshore challengers, allocator advice, M&A wave)

- Watchlist + Full PDF

Why it matters

- This unlocks instant settlement. Right now, settling a tokenized security on-chain requires two things moving at once: the asset and the cash. If broker-dealers can’t hold digital cash without wrecking their capital, that second leg doesn’t work. The 2% haircut fixes that. BlackRock and Apollo are already pushing tokenized money market funds into DeFi as collateral, using them as high-quality collateral for stablecoin borrowing on protocols like Morpho and UniswapX. Now broker-dealers can actually sit in the middle of those flows without bleeding capital. That’s the unlock.

- The USDT kill switch? Let’s be precise here. The FAQ doesn’t kill Tether, it forces Tether to play by American rules. USDT doesn’t qualify. It’s not issued by a U.S.-regulated entity and it doesn’t meet the monthly audit standards the GENIUS Act requires. Broker-dealers holding USDT still eat the full 100% haircut. But Tether saw this coming. In January, it launched USAT, a compliant stablecoin issued through Anchorage Digital Bank with Cantor Fitzgerald as custodian. So now we have a two-track market: USDT keeps its $184B dominance offshore and in emerging markets. USAT and USDC fight for the regulated U.S. institutional business. The rotation is already happening. Bernstein projects USDC surges from $74B today to $220B by 2027, capturing a third of the global stablecoin market.

- There’s a catch. The 2% haircut sounds generous, but netting is prohibited. A broker with a perfectly hedged $100M USDC position still pays a $2M capital charge. In traditional fixed income, you’d offset that to nearly zero. This means wider spreads in institutional stablecoin trading, a higher bar for on-chain arbitrage, and a natural cap on DeFi leverage. The SEC gave with one hand and took with the other.

- Banks should be terrified. Banks lobbied (led by the American Bankers Association (ABA) and Banks lost the war they thought they won. The banking lobby fought hard to block yield-bearing stablecoins in the GENIUS Act – and they succeeded for now. The law bans direct yield payouts. But that was the wrong battle. The 2% haircut makes stablecoins the best tool for 24/7 wholesale settlement, cross-border payments, and tokenized securities clearing. The Bank Policy Institute warned Congress that $6.6T in deposits are at risk if stablecoins become cash-equivalent in institutional workflows. With this FAQ, they just did.

Investor Alpha

Here’s the bottom line. By making offshore stablecoins capital-toxic and giving compliant ones near-cash status, Washington just picked its winners. The trade is straightforward.

- Circle (CRCL) is the clearest beneficiary. The SEC essentially gave U.S.-regulated stablecoin issuers a state-sanctioned advantage in institutional settlement. Circle has the compliance infrastructure, the distribution network, and years of liquidity depth that no competitor can replicate overnight. Bernstein’s $220B USDC supply target by 2027 looked aggressive six months ago. It looks conservative now.

- Coinbase (COIN) benefits twice. USDC was co-founded by Coinbase, which still earns economics on Circle’s reserve fund. More institutional USDC flowing through the system means more T-bill yield hitting that revenue line. On top of that, Coinbase Custody becomes a natural settlement node for every broker-dealer building on-chain infrastructure. Two revenue streams, one catalyst.

- Watch the onshore stablecoin challengers. USAT, PYUSD, FIDD and other GENIUS Act-compliant tokens will see a bump in institutional demand for B2B payments and settlement. But none of them have Circle’s head start. The real question is whether Tether’s brand and Cantor’s distribution can close the liquidity gap fast enough to make USAT a credible competitor. We’re skeptical in the near term.

- If you’re an allocator or hedge fund COO, renegotiate now. The 2% haircut fundamentally changes the cost of carrying digital assets on a prime brokerage balance sheet. Your fee structures were priced for a 100% capital charge world. That world no longer exists. Move quickly, the brokers who figure this out first will repricing before you ask.

- The M&A wave is coming. The SEC’s innovation exemption requires strict KYC/AML whitelisting through registered transfer agents. Legacy custodians like State Street and BNY Mellon need this capability and don’t have it natively. Expect aggressive acquisitions of crypto-native transfer agents over the next 12 months. That’s where the on-chain tokenization bottleneck sits and big institutions will pay up to own it.

Watchlist:

- Feb 17–21: ETHDenver 2026

- Feb 18: FOMC minutes for Jan 27–28 meeting

- Feb 19: Fed Gov. Bowman Speech

- Mar 1–2: Crypto Expo Europe (Bucharest)

- Mar 11: US CPI (Feb) release – critical for Fed rate cut expectations

- Mar 17–18: DC Blockchain Summit (Chamber of Digital Commerce)

- Mar 18: FOMC Interest Rate Decision & Summary of Economic Projections

That’s it for now.

Missed last week? Access all our CEO notes here.

Marc & Team

Download the PDF