How the SEC is rewriting capital markets

For a decade, the SEC waged war on crypto through enforcement. Now Paul Atkins is doing something far more dangerous to the old guard: he’s winning.

Last week, the SEC Chair announced an ‘innovation exemption’ coming in January 2026, the formal end of a decade-long regulatory war that cost American venture capital billions. [ANNOUNCEMENT]

Let’s unpack.

Download the PDF

Today’s Market Signals

Robinhood will introduce crypto staking for all New York customers. Link

Circle has partnered with privacy blockchain Aleo to launch USDCx, a privacy-enhanced stablecoin. Link

EU plans 2027 reforms centralizing market and crypto oversight under ESMA. Link

What happened

The “regulation by enforcement” era officially ends. After a brief delay due to the government shutdown, SEC Chair Paul Atkins confirmed the “Innovation Exemption” launches in January 2026. This directive—part of “Project Crypto“—allows digital asset firms to launch on-chain products under a temporary “sandbox” without immediate registration, provided they meet specific guardrails.[Update]

“ICOs transcend all four topics. Three of those areas are on the CFTC side, so we’ll let them worry about that, and we’ll focus on tokenized securities.”

– Paul Atkins, SEC Chair

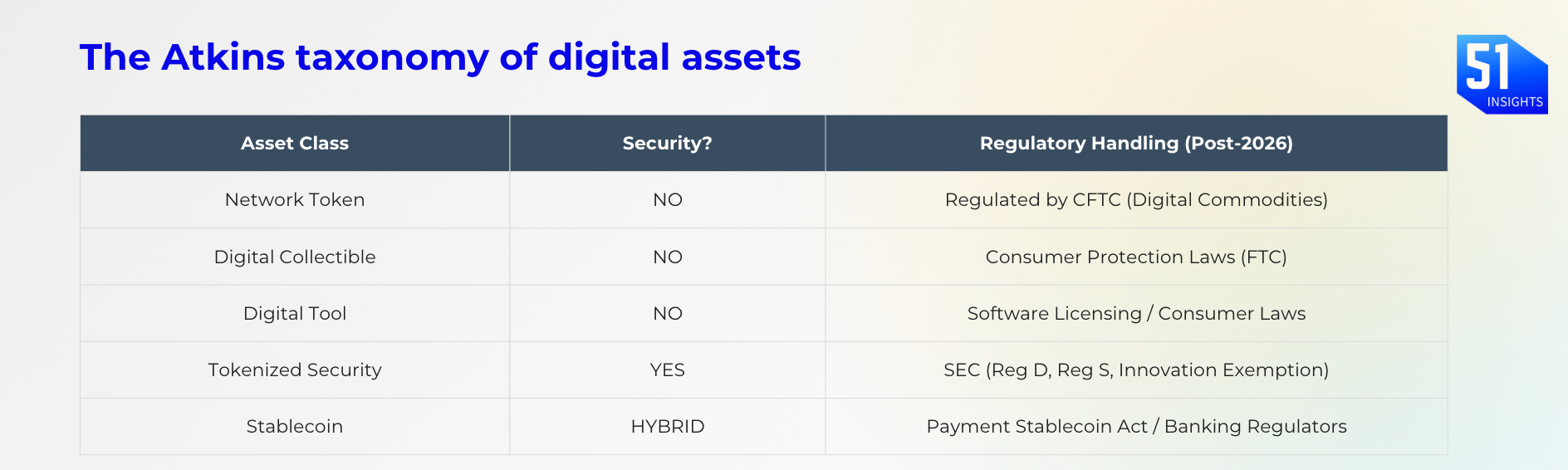

Zooming in: For years, regulators have assumed that most crypto tokens are securities, primarily because many originated from initial fundraising deals. This view focused on how a token was created, not how it is used today. Paul Atkins’ appointment as SEC Chair and the launch of Project Crypto in mid-2025 marked a major shift in how the agency thinks about digital assets.

Now, the SEC is actively rewriting the rules for market structure:

The SEC is developing a formal token taxonomy using the Howey test to clarify whether crypto assets are securities.

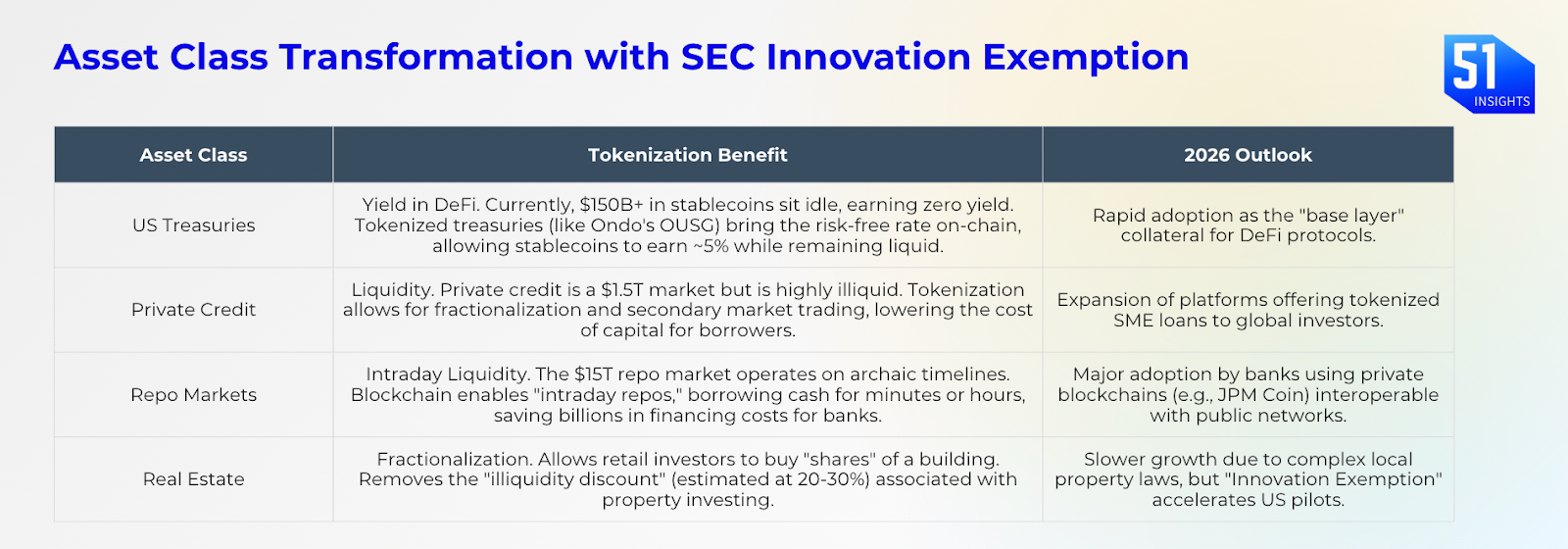

They have formally closed the investigation into Ondo Finance without charges, tacitly endorsing its SPV-based tokenization model.

On November 27, the Commission proposed a framework to allow tokenized Treasury bills and stablecoins as collateral for 24/7 derivatives trading, aiming to close the dangerous “weekend gap” in traditional banking settlement.1

“Tokenisation of U.S. equities is already happening.”

– Hester Peirce, SEC Commissioner

Key ideas in Atkins’ approach:

- Atkins rejected the idea that a token is a security forever just because it began in a fundraising deal. Once the original team’s promises are fulfilled and the network runs on its own, the token should no longer be treated as a security.

- A stock is still a stock whether it’s on paper or on a blockchain. But a decentralised token used for payments, access, or utility is not the same as a claim on a company’s profits.

- The new policy direction aims to let platforms trade crypto assets, stocks, and commodities in one place under a single license, instead of forcing activity into separate SEC and CFTC buckets.

What’s next: The SEC’s Crypto Task Force is holding a roundtable on financial surveillance and privacy on Dec. 15.

Sandbox architecture

The exemption lets qualified firms launch tokens without going through the full SEC registration process, as long as they follow specific guardrails. A defined “sandbox period” (typically 3 years) during which the network can mature.

A key part of the exemption is the “Exit Ramp.” The exemption is temporary. When the trial period ends, every project must show one of two results:

- If the network is truly decentralised, the token becomes a “digital commodity” and moves under CFTC oversight.

- If the network is still centrally controlled, the issuer must complete full SEC registration or shut the project down.

Why it matters

- The death of the middlemen: The SEC’s proposal to use tokenized collateral for derivatives highlights a deeper disruption: the obsolescence of the clearing layer. In a tokenized model, trade execution and settlement happen simultaneously (atomic settlement). This removes principal risk and drastically reduces the need for central clearing houses, depositories, and custodians.

- The $16 Trillion Bridge. The strategic implication here is binary: digital assets are graduating from a speculative asset class to the operating system of capital markets. By establishing a clear taxonomy (distinguishing “Tokenized Securities” from “Network Tokens” and “Digital Commodities”), Atkins is unlocking the $16 trillion opportunity in Real World Assets (RWA). Today, tokenised RWAs sit at a meagre $36B. The Innovation Exemption is the regulatory unlock required to move bonds, real estate, and private equity on-chain at scale.

Marc Baumann

Marc BaumannInvestor Alpha

The winners of the 2026 cycle will not be the “crypto-native” casinos, but the compliant infrastructure that bridges Wall Street to the blockchain. We believe the market is severely underpricing the value of regulatory moats.

Key companies to watch:

Tokenization:

Ondo Finance: By closing the probe without action, the SEC has tacitly endorsed Ondo’s architecture as a compliant model for tokenisation. Trade

Securitize: Major asset managers like BlackRock have already partnered with Securitize. With this regulatory clarity, they can now accelerate their tokenisation plans, which will push Securitize as the prominent infrastructure for tokenisation. They will go public next year through a SPAC deal with Cantor Equity Partners.

Superstate: Superstate, founded by Robert Leshner, an early DeFi founder, acts as an SEC-registered digital transfer agent, ensuring regulatory compliance is embedded within the on-chain process.

The connectivity layer: Chainlink. The “TCP/IP” of tokenisation. Banks will likely build on private blockchains (for privacy) but need to connect to public markets (for liquidity) and real-world data (interest rates). Chainlink’s Cross-Chain Interoperability Protocol (CCIP) is the industrial standard for this connectivity.

Keep an eye on super-apps: Coinbase & Robinhood. These firms are the most likely to become the first “Super-Apps.” Regulatory clarity allows them to list tokenised securities and offer high-yield on-chain savings accounts to retail users.

Watchlist

- Dec 15: SEC roundtable (crypto task force)

- Dec 15: Cboe Global Markets will launch the first U.S.-regulated perpetual-style futures contracts (PBT and PET)

- Dec: USAT launch by Tether (expected)

- Dec: Clarity Act (H.R.3633) Senate vote (expected)

- Dec 31: Europe’s MiCA full enforcement (Austria, Germany, and Spain) ends

Take care,

Marc & team

Download the PDF

🙌 Work with us: We arm financial institutions and digital asset leaders with bespoke research, thought leadership to shape the most important conversations, scale trust, and win business.

On November 27, 2025, the SEC proposed a framework that leverages tokenisation and stablecoins primarily to resolve the systemic risk created by the misalignment between continuous 24/7 global derivatives trading activity and the limited operating hours of traditional banking settlement rails. [PROPOSAL]

Closing the weekend gap: The proposal uses tokenised Treasury bills and approved stablecoins to allow instant, round-the-clock margin payments, helping the system stay stable during periods of market stress.

Faster margin collection: Tokenised collateral lets firms send margin almost instantly, even on weekends. This cuts the time they are exposed to risk.

Lower counterparty risk: Collateral and payment move at the same time (<1m), sharply reducing the chance that one party fails to deliver.

Only regulated stablecoins: Only GENIUS Act-Compliant Payment Stablecoins are eligible as derivatives margin. These stablecoins are required to maintain 100% reserves in high-quality liquid assets (such as cash, insured deposits, or Treasury bills) and are subject to federal banking or OCC oversight.

There are also other guardrails and checks for custody, valuation and haircuts. ↩