China Pays Yield. America Bans It.

Remember when your bank paid 0.1% on checking? Then Coinbase started paying 4.5% on your USDC. Not interest: “rewards.”

That loophole might be dying this Thursday.

On January 12, Senate staff told crypto leaders they would “need prayers“ for the January 15 markup on the Clarity Act1, signalling that banks had successfully lobbied to close the stablecoin “loophole” that allows platforms like Coinbase to share Treasury returns with users. The $1.3B Coinbase revenue stream from stablecoin yield? Gone.

China started paying interest on the digital yuan on January 1st. America is banning it. What’s going on?

This vote is not just about your 4.5%. It’s about whether America gets regulatory clarity at all.

Let’s unpack.

👉PRO: Download the PDF at the bottom

What happened:

The Senate Banking Committee will vote on January 15 on the death of stablecoin yield.

While the 2025 GENIUS Act banned issuers (like Circle) from paying interest, it left a loophole for intermediaries (like Coinbase) to pass 4.5% treasury yield to users as “rewards.” Legal arbitrage. The banking lobby just closed it.

Just-in: The latest draft (page 189) says companies cannot pay interest just for holding balances. They can earn rewards, but only if they’re tied to opening an account or activity like making transactions, staking, providing liquidity, putting up collateral, or participating in network governance.

Zooming in: Your local bank lobbied (led by the American Bankers Association (ABA)2 and Banking Policy Institute (BPI)3) against your ability to earn yield. They sent Congress a letter: $6.6T in deposits are “at risk.” At risk of what? Paying you market rates.

What they’re saying:

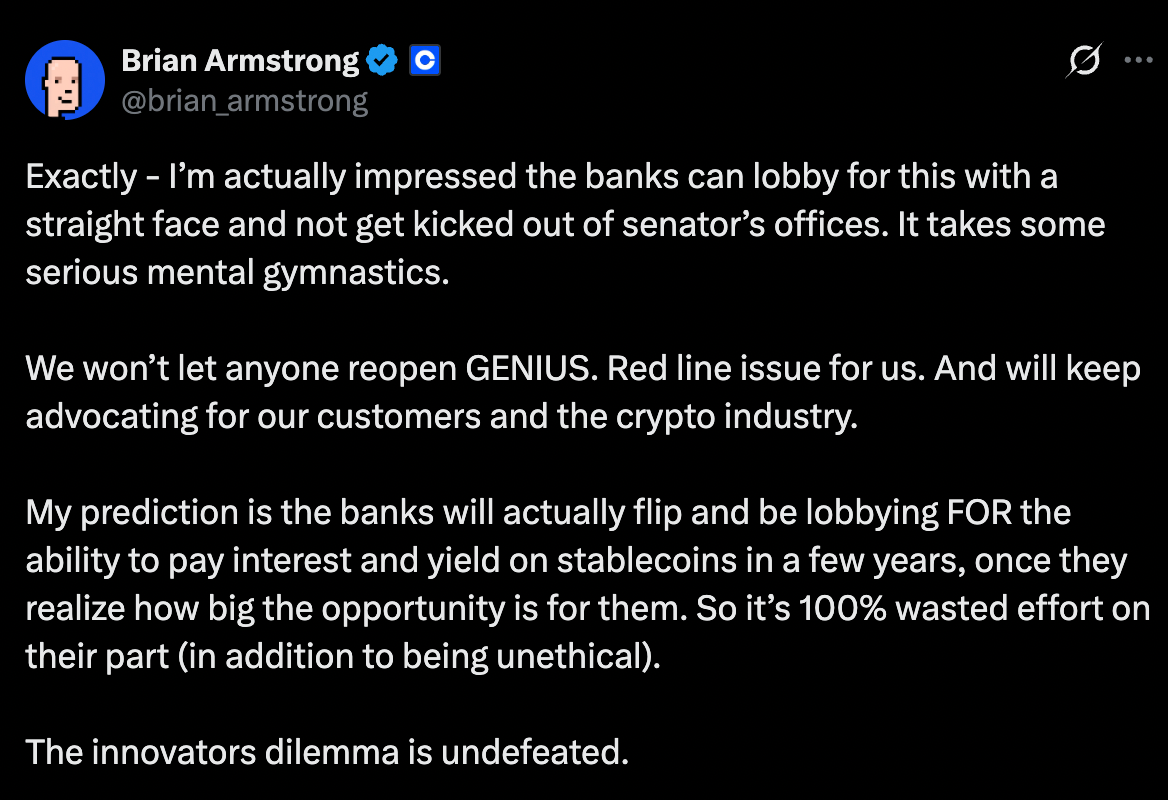

- Coinbase is telling the crypto industry to stand down on opposing the stablecoin yield language for now.

- Senator Angela Alsobrooks (D-MD) has proposed a last-minute compromise: limiting yield strictly to “transaction-based” activity while banning passive yield on deposits.

“We want to make sure that we are not doing anything that mimics a bank-like product without bank-like protections. Pay rewards on transactions made with dollar-pegged stablecoins, but bar programs that pay rewards on tokens sitting in a digital wallet.”

– Senate Angela Alsobrooks (D-MD)

The American Bankers Association’s case: Interest-bearing stablecoins pull deposits from community banks. Fewer deposits mean fewer loans to small businesses, farmers, and students. Circle and Coinbase exploit a “loophole” by paying yield through affiliates. Stablecoins lack FDIC insurance. Ban it all.

Banking Policy Institute argued stablecoins are “shadow banks” that bypass regulation while offering superior products. They want stablecoins to function strictly as payments (M0) not savings (M1/M2).

Here’s how the arbitrage worked

The GENIUS Act (passed July 2025) banned stablecoin issuers like Circle from paying interest to holders. Clean and simple.

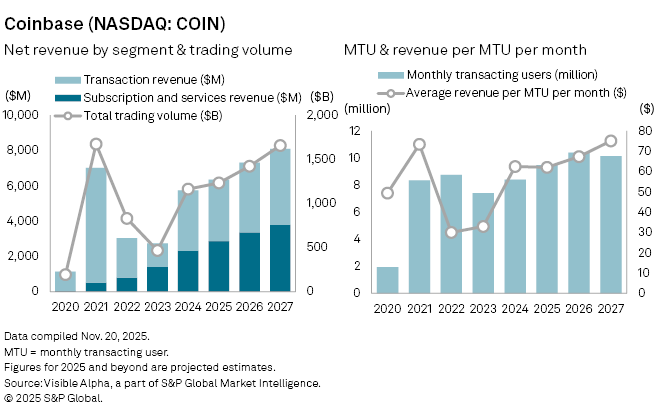

But Circle doesn’t pay interest. Circle earns it. Circle generated $711M in Q3 2025 from interest on the $60B+ in Treasuries backing USDC. That’s 96% of their revenue. They can’t share it with users—but they can share it with Coinbase.

The revenue-sharing deal: Coinbase gets 100% of interest on USDC held on Coinbase’s platform, 50% on USDC held elsewhere. Circle paid Coinbase $900M in 2024—54% of Circle’s total revenue—as “distribution costs.”

Coinbase then offers that money to users as “rewards.” Not interest. Rewards. Legal.

The banking lobby just closed it.

Coinbase generated $1.3B from this model in 2025. Mike Novogratz didn’t hold back: “Sad state that Congress cares more about banks’ margins than they do consumers! Both [Democrats] and [Republicans] need to ask who are they serving?“

In short: The proposed amendments can extend the GENIUS Act’s yield prohibition beyond stablecoin issuers to all third-party intermediaries, including Coinbase, Kraken, and other digital asset service providers. This kills how Coinbase makes money. This reverses the current operating model, where Eexchanges legally share a portion of reserve interest (currently ~4.5%) with users as “rewards” rather than “interest.”

Plot twist: Coinbase may withdraw support for the entire CLARITY Act if yield restrictions pass, per Bloomberg sources. When your biggest industry supporter threatens to walk, you’ve miscalculated.

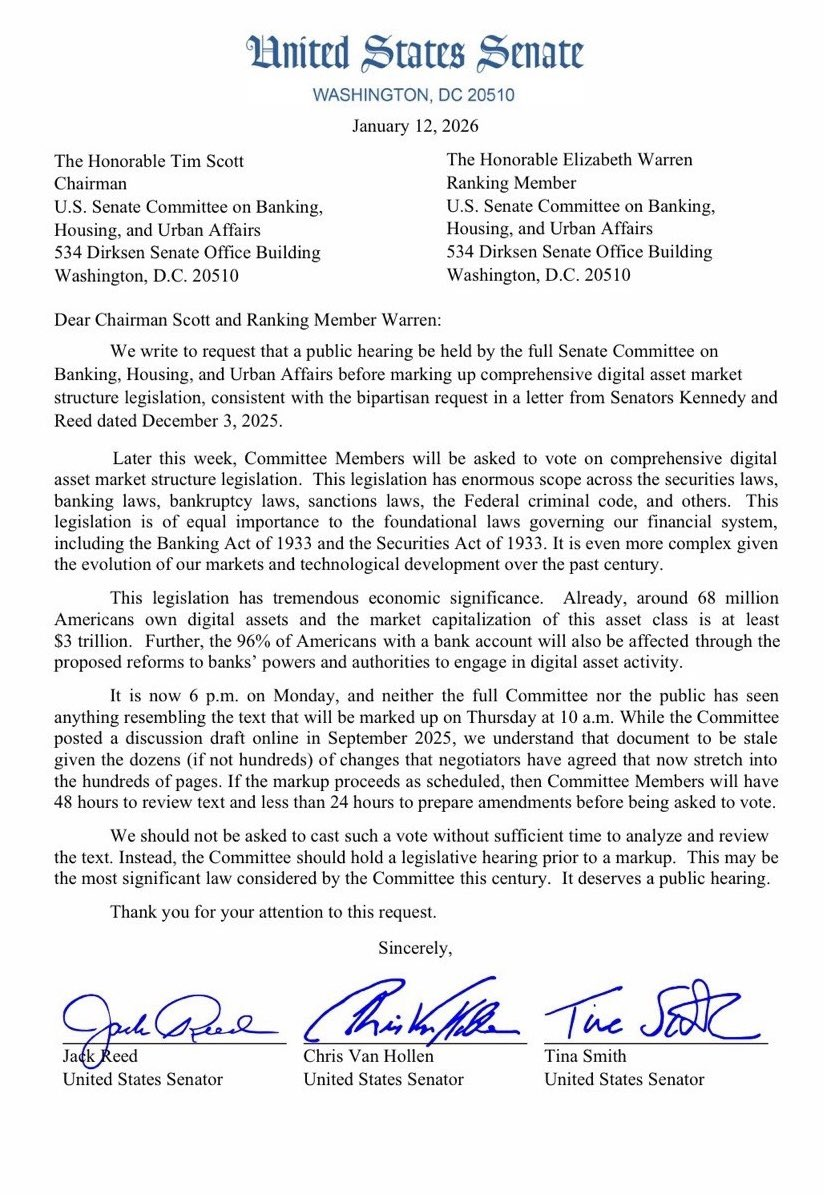

Must know: The Jan 15 markup isn’t the real decision point, it’s just one committee moving its piece forward. This is a bipartisan bill4 that only matters once both committees (Senate Agriculture Committee and House Committee on Financial Services) agree and enough Senators are lined up to actually pass it.

Banks want to ensure that payment stablecoins function strictly as a medium of exchange (like cash) rather than an investment product (like a savings account or money market fund).

Why you need to pay attention

PRO subscribers get the non-obvious alpha below:

- The China angle nobody is pricing in

- The winners / losers of Thursday’s vote

- Our watchlist

- The full board-ready PDF

Existential threat to banks: According to a U.S. Treasury Department report from April 2025, widespread stablecoin yield adoption could catalyze up to $6.6T in deposit outflows from traditional banking. Banks operate on a “maturity transformation” model: they take non-interest (or near-zero interest) deposits and lend them as 30-year mortgages or business loans. The spread, the Net Interest Margin (NIM), is how they fund lending to Main Street. If you’re rational, you already moved. 4.5% beats 0%. Instant settlement beats T+2. 24/7 access beats banker’s hours. If even a fraction of operational cash migrates from checking accounts to USDC wallets, community banks lose their cheapest funding source. To attract deposits back, they must raise savings rates, which increases their cost of funds, which forces them to raise loan rates, which contracts credit to the “real economy.”

China weaponized yield on January 1st. Geopolitical pov: China weaponized yield on January 1st. The People’s Bank of China announced commercial banks can pay interest on e-CNY wallets. This transforms the digital yuan from cash (M0) to savings (M1/M2)—a direct competitor to the dollar in international settlement.

The U.S. Senate is removing yield from the digital dollar while China adds it. Pro-crypto lawyer John Deaton nailed it: “The stakes are higher than ever because China officially began paying interest on the Digital Yuan—making it a ‘yield-bearing’ competitor to the USD.”

The “transaction” compromise creates chaos: Alsobrooks’ proposal allows yield only on transactions (velocity) not balances (savings). This protects banks by making stablecoins a payment rail rather than savings account.

But the gray area is massive:

If I swap USDC to BTC and back, is that a transaction?

Does depositing into Uniswap count as “activity”?

Who defines “transaction-based”? The proposal bifurcates the industry: payment processors like Stripe (who monetize velocity) win. Exchanges like Coinbase (who monetize assets on platform) lose.

- This isn’t policy: The banking lobby framed deposit flight as a systemic risk. But the mechanism is basic competition: stablecoins offer a superior product. Instant settlement. Market-rate yield. Global access. The only “risk” is that consumers choose better financial infrastructure.Mike Novogratz again: “What I say to banks who are whining like mad 4th graders. Toughen up and compete. This is what innovation looks like.”

Investor Alpha

Many investors treat this as a binary policy event, it is, but outcomes are not evenly distributed. A ban on third-party yield compresses exchange economics and reallocates alpha to payment processors, tokenized-deposit providers, and custody infrastructure. If the Alsobrooks compromise holds, the alpha moves to infrastructure that powers payments, not savings. The most durable winners are firms that capture transaction velocity or own the settlement rails.

- Long Regional Banks (KRE): This legislative crackdown is a direct subsidy to the regional banking business model. If the yield ban passes, the threat of deposit flight vanishes, stabilizing their funding costs.

- GSIBs (JPM): If stablecoins are neutered by regulation, bank-issued tokenized deposits become the only game in town for institutional blockchain settlement.

- Long Payment Processors (PYPL / Stripe): The “Alsobrooks Compromise” (yield on transactions only) specifically favors closed-loop payment networks.

- Short Coinbase (COIN) into the Markup: Coinbase reported $332M in stablecoin revenue in Q2 2025, largely derived from the yield sharing agreement with Circle. A ban on passive rewards strikes at the heart of their “Super App” retention strategy.

Here’s the brutal irony: China launched interest-bearing digital yuan on January 1st. We’re banning it on January 15th. While Beijing weaponizes yield to compete globally, Washington protects regional bank NIMs domestically.

This isn’t crypto regulation. It’s a $6.6T banking subsidy disguised as consumer protection. The trade? America cedes the digital dollar yield advantage to Beijing, and you go back to earning 0.1% on checking.

Watchlist:

- Jan: USAT launch by Tether (expected)

- Jan: Clarity Act (H.R.3633) Senate vote (expected)

- Jan 13: Consumer Price Index data for December 2025; heavily influence the January 27-28 meeting

- Jan 15: Senate committee vote

- Jan 27: The Federal Reserve will convene for two days, with the rate decision

- Jan: SEC Crypto Innovation Exemption

- Jan: Spot crypto ETF approvals for altcoin

- Q1’26: Kraken IPO

- Q1’26: Hong Kong Stablecoin licensing

- Q1’26: Singapore Stablecoin framework

Market signals

- Dubai moves to ban privacy coins. Link

- Wells Fargo allows BTC as collateral for loans. Link

- BNY activates tokenised deposit service. Link

- Venezuela used USDT to bypass sanctions. Link

- Ripple secures FCA authorization in UK. Link

That’s it for now.

Marc & Team

The Clarity Act beyond yield: The Senate Banking Committee’s markup on January 15 will also decide the fate of DeFi and Self-Custody.

The draft legislation attempts to define “Digital Asset Service Providers” (DASPs). The banking lobby, through the BPI, has expressed strong concerns about DeFi lending acting as a “shadow bank”. If the definition of DASP is broad enough to include software developers or governance token holders of protocols like Aave or Compound, the yield ban would extend to DeFi.

To counter this, crypto-friendly Senators have fought to include Section 501, titled “Protecting Software Developers”. This section clarifies that software developers who write non-custodial code are not financial institutions under the Bank Secrecy Act. The BPI and anti-money laundering (AML) hawks view this as a loophole for terrorists and criminals. They are pressuring the committee to strip Section 501 from the bill during the markup.

Integrated into the market structure bill is the right to self-custody. Banks argue that unhosted wallets are opaque and dangerous. The industry argues that self-custody is a fundamental human right akin to holding physical cash. If self-custody is protected, the yield ban becomes harder to enforce. Users can simply withdraw funds from Coinbase (regulated) to a self-hosted wallet and access offshore DeFi yield (unregulated). ↩

On January 5, 2026, ABA sent a letter to the Senate addressing its concerns, saying $6.6T bank deposits are at risk:

Deposit flight: Interest-bearing stablecoins could pull savings out of community banks.

Local credit impact: Fewer deposits mean fewer loans for small businesses, farmers, students, and homebuyers.

Loophole abuse: Issuers use affiliates and exchanges to pay “rewards,” bypassing the interest ban.

Consumer risk: Stablecoin products lack FDIC insurance and bank-level protections.

Policy ask: Apply the interest ban to stablecoin issuers and their partners to protect local economies.

Later on June 10, 2026, they also released a statement highlighting its core concern is that digital asset legislation must give banks clear permission to engage in crypto-related activities while holding non-bank crypto firms to comparable safety, compliance, and consumer protection standards. ↩

Deposit flight risk: Interest-bearing stablecoins could pull deposits out of banks, reducing credit to the real economy.

Backdoor yield: “Rewards” or affiliate-based yield programs undermine bans on stablecoin interest.

Systemic risk: DeFi lending mimics banks but lacks basic safeguards like insurance, capital, and liquidity rules.

Illicit finance: Weak oversight enables criminals to use wallets and DeFi to bypass U.S. financial controls. ↩

A bipartisan bill is a piece of proposed legislation in a two-party system (like the U.S.) that receives support, negotiation, and agreement from members of both major political parties, aiming to find common ground on policies ranging from critical national security issues to social programs, demonstrating cooperation rather than division. These bills often address urgent matters or controversial topics, incorporating compromises from both sides to achieve broader appeal and passage.

More reads:

What’s Happening on Crypto Market Structure? (Bank Policy Institute)

Community Bank Leaders Urge Senate to Protect Local Lending from Stablecoin Risks (ABA)

Key Democrat floating stablecoin yield compromise in crypto bill (Politico)

Modernizing Supervision and Regulation: 2025 and the Path Ahead (Fed)

What “Unsafe or Unsound” Actually Means Under the Law (Bank Policy Institute)

Potential impact on community bank lending (Secure American Opportunity by ABA) ↩