Tether just put on a suit

Hey, it’s Marc & 51 team,

For a decade, Tether (USD₮) was the “offshore casino chip,” massive, liquid, but operating in the regulatory shadows. Wall Street ignored it; regulators hunted it.

But on January 27, 2026, Tether launched USA₮, a federally chartered stablecoin backed 1:1 by short-term Treasuries, held at Anchorage Digital Bank, and custody by Cantor Fitzgerald.

The Fed didn’t lose control. It delegated it. Now $186.2B in private-sector dollars can settle 24/7 across blockchains without touching the Federal Reserve’s ledger.

The collateral hierarchy just got disrupted by the very person who would have fought it hardest: a regulator.

Let’s unpack.

👉PRO: Download the PDF

What happened

Tether launched USA₮ on January 27, 2026, as the first federally compliant stablecoin issued through a nationally chartered bank. The token operates on Tether’s Hadron platform and is backed by 1:1 reserves in U.S. currency, demand deposits, or short-term Treasuries, exactly as mandated by the GENIUS Act (enacted July 18, 2025).

The Office of the Comptroller of the Currency (OCC) granted the “Permitted Payment Stablecoin Issuer“ (PPSI) status required for U.S. operations.

- Regulation: Compliant with the GENIUS Act of 2025.

- Oversight: Direct supervision by the OCC (Office of the Comptroller of the Currency).

- Backing: 1:1 in US currency or short-term Treasuries.

- Yield: 0%. The GENIUS Act strictly prohibits paying interest to holders (protecting bank deposits from direct yield competition).

Marc Baumann

Marc Baumann Marc Baumann

Marc Baumann

Bo Hines, former Executive Director of the White House Crypto Council, was appointed CEO of Tether USA. Anchorage Digital Bank (America’s first federally regulated digital asset bank) handles minting and redemption. Cantor Fitzgerald (a primary dealer in U.S. government securities) holds the reserves and actively manages them in the Treasury market.

That means: A “compliant face” of Tether, built for institutions that demand federal oversight.

Be smart: The token is not a new asset. It’s regulatory formalization of what $186.2B in offshore USD₮ already does, act as digital dollars. The difference: USA₮ settles 24/7/365 on blockchain without counterparty risk, monthly independent audits confirm reserves, and the OCC has direct regulatory oversight.

Zooming in: Tether runs a fractional-reserve model where its assets exceed its liabilities, creating a small equity cushion. Tether is now the 17th-largest Treasury holder globally, sitting ahead of Germany, South Korea, and Australia as a sovereign wealth fund would.

Be smart: The GENIUS Act subordinated stablecoins by forcing 1:1 reserve backing in Treasury bills, the law turned Tether into an interest-free buyer of government debt. It deputized Tether as an arm of fiscal policy. When Tether mints USA₮, it doesn’t lend it. It buys T-bills. The more USA₮ circulates, the more the Federal government can borrow without foreign central banks.

By the data: Standard Chartered estimates one-third will migrate from traditional bank deposits ($100B by Q2 2026) to Stablecoins. By 2028, as the market hits $2T, $500 B could exit developed-market bank balance sheets.

But here’s the fact: that $500B doesn’t vanish. It flows into Treasuries.

Marc Baumann

Why it matters

The banking system’s structural vulnerabilities: Regional banks are in trouble. Community institutions like Huntington Bancshares, M&T Bank, and Truist Financial rely on deposit bases to fund lending. Their Net Interest Margin (NIM), the spread between deposit costs and loan rates, is how they fund the credit that powers Main Street. When a corporation moves $1M from a bank account to USA₮, it is permanent. The bank loses the ability to lend that $1M as a mortgage or business loan. To attract deposits back, the bank must raise savings rates, which increases funding costs, which compresses lending.

Traditional bank deposits use fractional reserve lending (lend out 90%, hold 10%). Stablecoin reserves are 1:1 (lend out 0%, hold 100%). A dollar in USDC recycled into Treasury bills does zero work for the real economy. It finances the federal government instead. However, it won’t just impact the business model of banks but also lending ability of banks.

A threat to Circle: For years, Circle (USDC) traded on one value prop: “We are the compliant ones.” Tether traded on “We have the liquidity.” With USA₮, Tether now has both. It pairs the massive global distribution of a company with $13B in annual profits with the same OCC-regulated status as Circle. The “war of features” in 2026 will be vicious: cross-chain interoperability, transaction fees, ERP system integration. But the outcome is predetermined. Tether has global distribution, domestic scale, and Treasury support. Circle has a better compliance profile that nobody needs anymore.

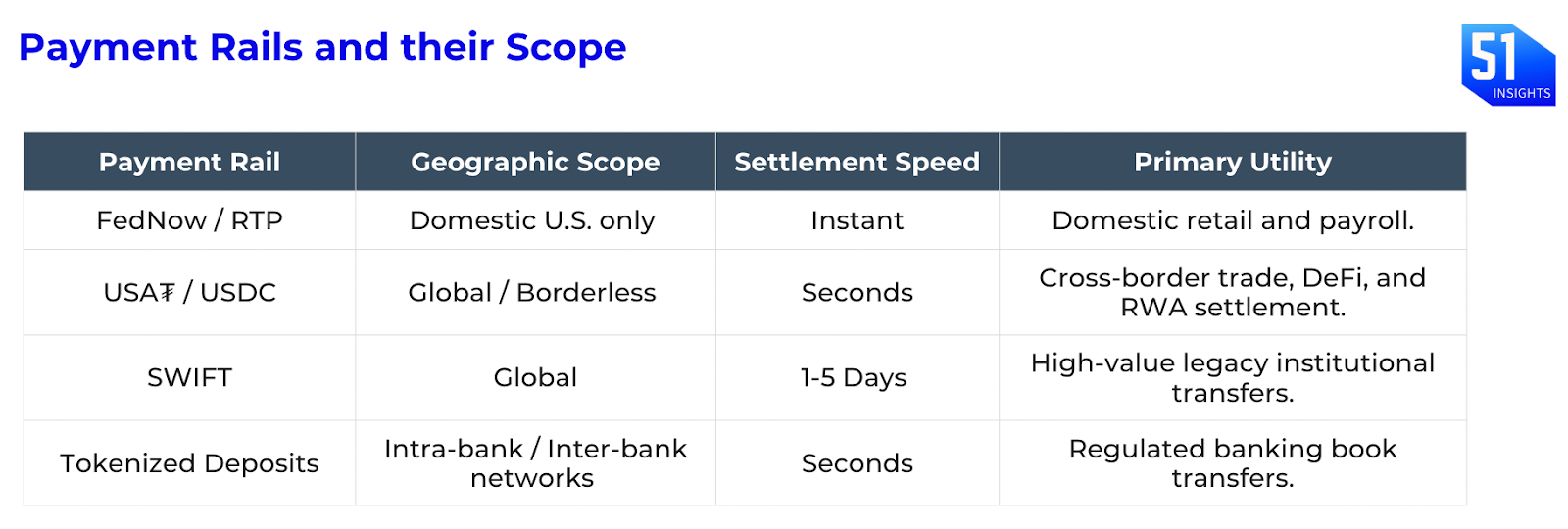

The settlement rail: USA₮ doesn’t replace the Federal Reserve. It bypasses the Federal Reserve. Traditional bank transfers (ACH/Wire) require movement of reserves between banks via the Fed’s ledger, which operates on limited hours and depends on correspondent banking relationships. USA₮ is a bearer instrument. Possession equals ownership. Atomic settlement means simultaneous exchange of USA₮ for other tokenized assets (digital gilts, tokenized equities) without a central clearinghouse. By 2026, corporate treasurers will use “multi-rail orchestration.” Domestic payroll flows through FedNow. Cross-border supplier payments flow through USA₮. Large institutional transfers flow through SWIFT. Each rail owns its niche because each solves a different problem. But USA₮ just became the global niche. It settles in seconds. It works 24/7. It requires no bank intermediary.

Investor Alpha

Winners are the picks-and-shovels providers. The custody operators. The settlement infrastructure firms. The institutions that monetize velocity instead of scarcity.

- Long Anchorage Digital Bank (Equity/Debt): The PPSI gatekeeper just became essential infrastructure. Anchorage processes every USA₮ minting and redemption. As $2T in stablecoins flows through the federal system by 2028, Anchorage’s throughput and compliance capabilities become non-negotiable. The margin profile: minimal.

- Short Regional Bank Deposit ETFs (KRE): Bank deposits face permanent structural headwinds. Huntington Bancshares, M&T, Truist, all exposed to corporate treasury migration. As USA₮ adoption accelerates, deposit bases compress. Q1 2026 earnings will show the first evidence.

- Long Payment Orchestration Platforms (ZeroHash, Volante: Private rounds only): The future is “multi-rail” settlement. Corporations will need APIs that route payments intelligently across FedNow, USA₮, SWIFT, and bank-issued tokenized deposits.

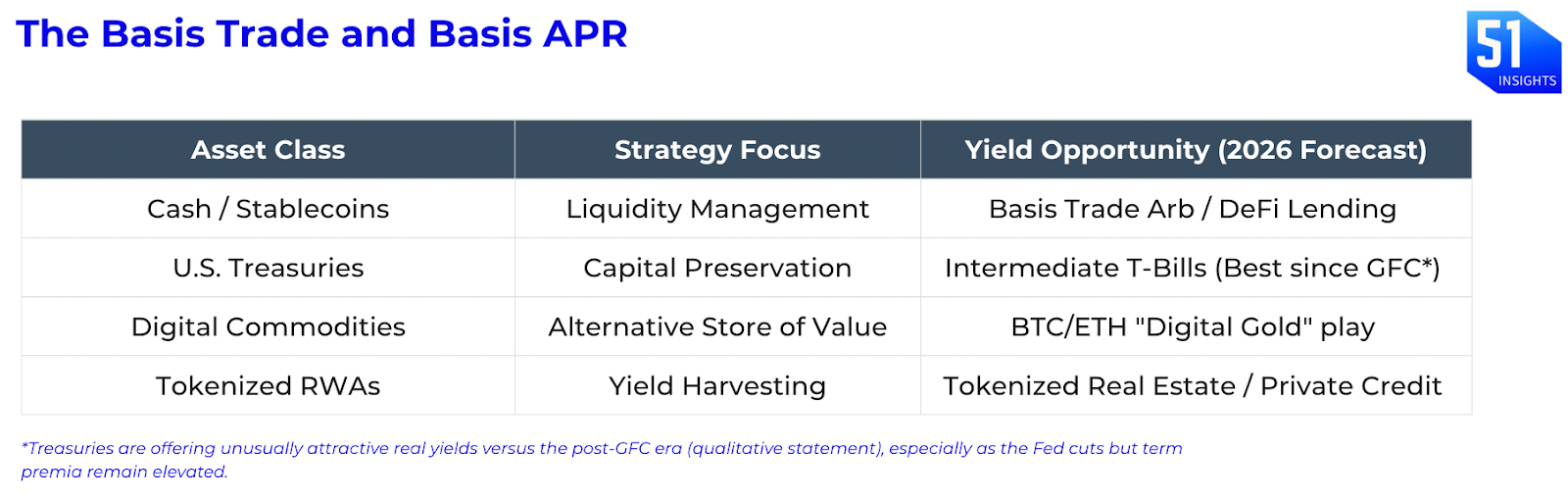

The most prominent institutional strategy in 2026 is the “basis trade,” simultaneously purchasing Treasury securities (or BTC/ETH spot) while selling corresponding futures contracts. Regulated stablecoins are the preferred collateral for these trades, as they provide the transparency required by institutional risk committees.

Watchlist:

- Feb 10–12: Consensus Hong Kong (CoinDesk)

- Feb 11: US CPI (Jan) release

- Feb 12: US PPI release

- Feb 12: FCA consultation on applying handbook rules to cryptoasset firms

- Feb 17–21: ETHDenver 2026

- Feb 18: FOMC minutes for Jan 27–28 meeting

- Feb: CLARITY‑style market‑structure bills and stablecoin implementation

- Q1’26: Kraken IPO window

- Q1’26: Hong Kong stablecoin licensing regime

- Q1’26: Singapore stablecoin framework launch

- Q1’26: Bitmine MAVAN (Made-in-America Validator Network) rollout

Market signals

- Citadel, DTCC and ICE back layer zero’s ‘ZERO’ blockchain. Link

- Goldman Sachs discloses $2.4B in crypto holdings. Link

- Chainlink to participate in the Bank of England’s Synchronisation Lab. Link

- Bithumb puts South Korea regulators on alert. Link

- Bitcoin ETFs inflows for first time in a month. Link

- Bitmine added 40,613 ether this week. Link

That’s it for now.

Marc & Team