Why the U.S. Treasury can't let Tether fail

hey, it’s Marc.

S&P Global downgraded Tether to “Weak” on Wednesday, citing a balance sheet that defies traditional risk management. The math is stark: Tether’s exposure to Bitcoin now exceeds its equity cushion.

With $180B in assets and zero deposit insurance, Tether is running the boldest liquidity experiment in finance. Here is why the U.S. Treasury might be forced to save a company it can’t even regulate.

Let’s unpack.

(💎PRO readers: PDF below)

What happened

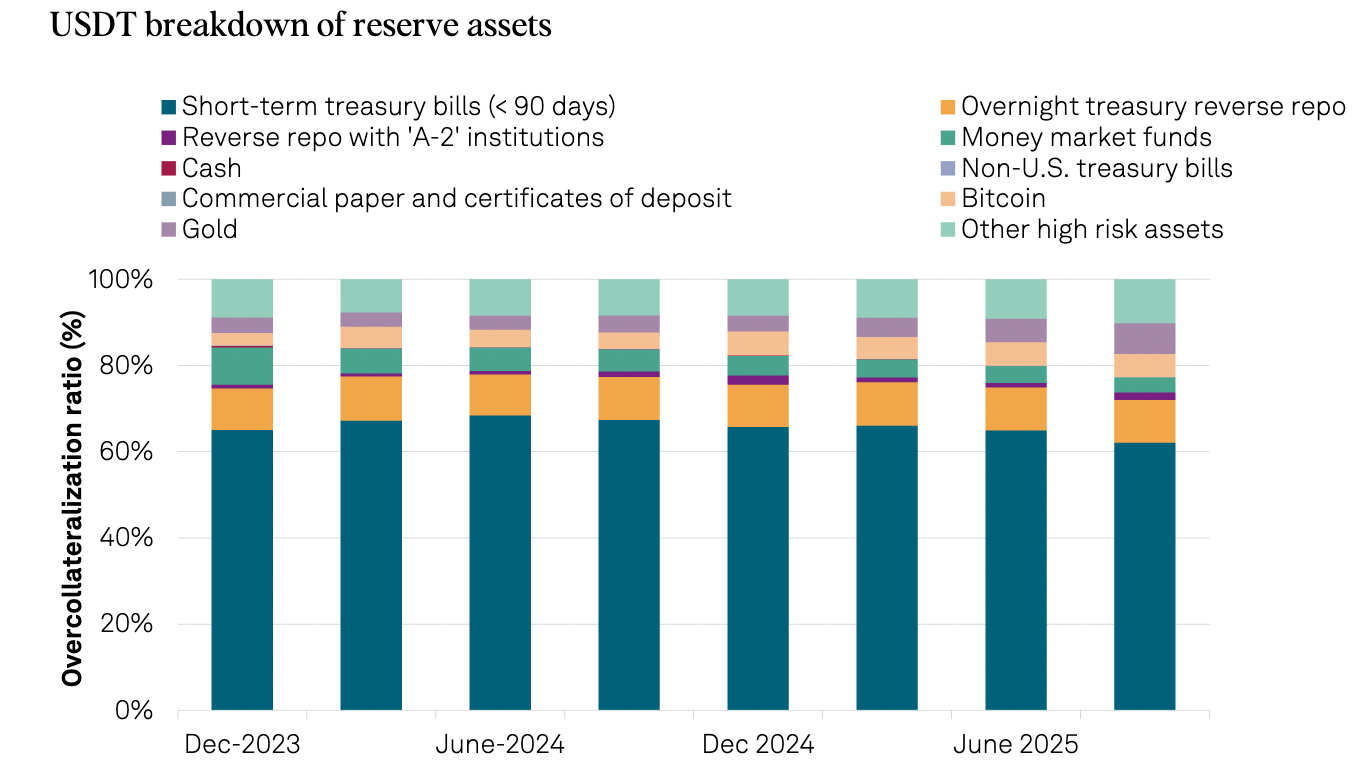

On November 26, 2025, S&P Global Ratings downgraded Tether (USDT) from “Constrained” to “Weak” (4 on a 5-point scale). The primary trigger was a shift in balance sheet composition: Tether’s holdings of Bitcoin now account for 5.6%of tokens in circulation, while its equity buffer (excess reserves) sits at just 3.9% ($6.8B). [see the report]

The math is simple: Tether’s exposure to volatile assets now exceeds its capacity to absorb a shock without dipping into customer funds.

- S&P’s view: 100% reserve coverage isn’t enough for a stablecoin issuer holding volatile assets without a lender of last resort. A 70% drop in BTC would render USDT technically undercollateralized.

- Tether’s view: CEO Paolo Ardoino dismissed the rating, citing $10B in annual profits and a massive portfolio of U.S. Treasuries ($135B) and gold. He framed the Bitcoin allocation as a strategic hedge against fiat debasement, not a liability.

The framework: S&P Global Ratings does not rate stablecoins using the traditional corporate bond scale (AAA to D). Instead, it employs a specialized “Stablecoin Stability Assessment” scale ranging from 1 (Very Strong) to 5 (Weak). This framework is designed to evaluate a single, binary outcome: the ability of the stablecoin to maintain its peg to a fiat currency or basket of assets.

Zooming in: Tether runs a fractional-reserve model where its assets exceed its liabilities, creating a small equity cushion. In Q3 2025, it reported $181.2B in assets against $174.4B in liabilities, leaving about $6.8B in “excess reserves.” That sounds large, but it’s only a 3.9% buffer, a thin margin for an instrument that underpins so much of crypto’s day-to-day liquidity.

Ardoino claims Tether is “the first overcapitalized entity in financial history”.

- Banks: Hold ~10% of deposits in liquid reserves but are protected by central-bank backstops and deposit insurance.

- Tether: Holds ~104% of liabilities in assets, but with no lender of last resort and no insurance safety net.

So even though Tether’s capital ratio looks higher than a bank’s, it has no safety net. Its 4% buffer is its only protection. S&P’s downgrade is basically saying that 104% coverage isn’t enough for a firm that can’t print money and still holds about a quarter of its assets in volatile instruments.

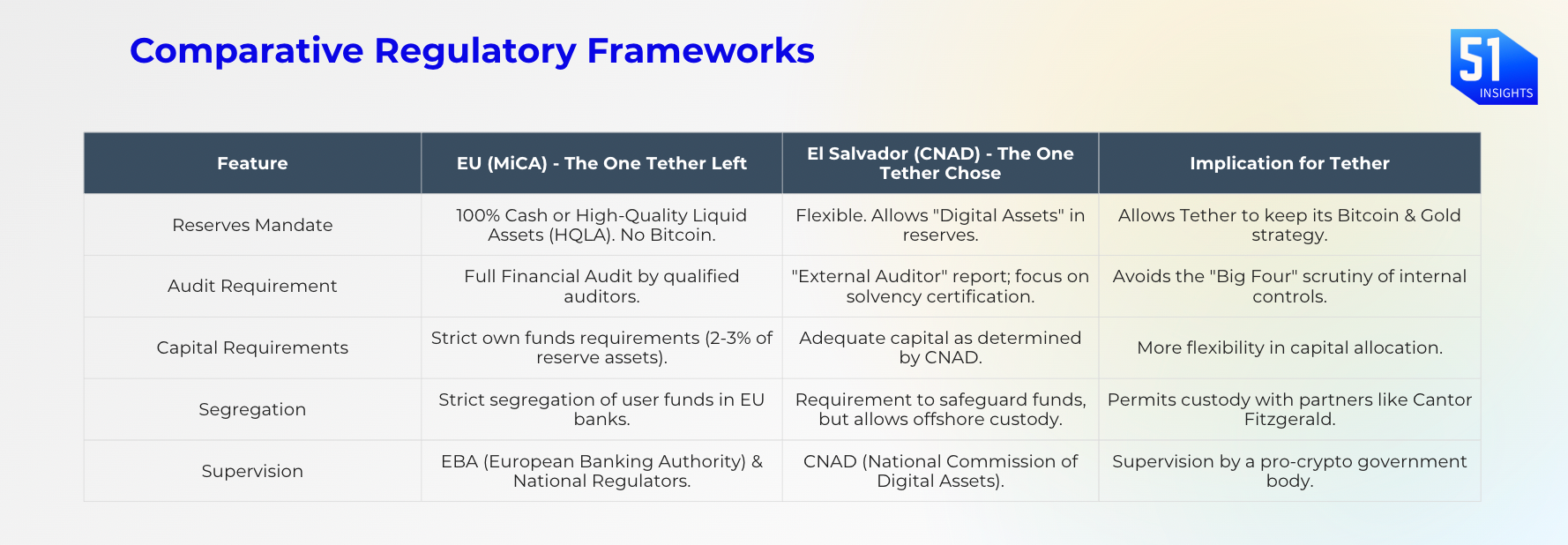

Simultaneously, Tether has finalized its regulatory migration from the Caribbean to El Salvador, effectively sidestepping the EU’s stringent MiCA regulations (which require 100% cash reserves) in favor of a jurisdiction prioritizing sovereign Bitcoin adoption.

🙌 Work with us: We arm financial institutions and digital asset leaders with bespoke research, thought leadership to shape the most important conversations, scale trust, and win business.

💎 What most people don’t see (alpha)

The Capital Structure Mismatch: Tether is operating a fractional-reserve model without the safety nets that make fractional banking viable. Banks hold ~10% capital but are backstopped by the Fed and FDIC. Tether holds ~104% capital but has no backstop. S&P’s downgrade signals that in a liquidity crisis, that 4% equity sliver is the only thing standing between a peg break and a run on the bank. Tether is betting it can grow its way out of volatility via yield generation; ratings agencies argue risk management shouldn’t rely on bull markets.

The “Too Big to Fail” Paradox: This is the most critical, under-discussed dynamic in global finance. Tether is now a top 20 holder of U.S. debt, owning more T-Bills than Germany or South Korea.

The Feedback Loop: By relentlessly recycling crypto inflows into U.S. debt, Tether subsidizes U.S. borrowing costs, saving the Treasury Department an estimated $15B in annual interest payments.

The Implicit Put: If Tether were to collapse disorderly, it would have to liquidize $135B in Treasuries. This would destablize the repo market and spike short-term rates.

The Conundrum: The U.S. Treasury effectively cannot ban Tether without risking a bond market flash crash.

The Governance Black Box: The “Attestation vs. Audit” debate remains unresolved. Tether provides quarterly attestations (snapshots in time) via BDO Italia, not full audits (deep dives into controls and flows over time) by a Big Four firm. S&P’s downgrade reflects the opacity of where those assets sit. If the widely reported custodian is Cantor Fitzgerald, the counterparty risk is concentrated. Without a full audit, institutional capital has no visibility into encumbrances or liens on those reserves. Be smart: In 2023, 90% of Tether was controlled by four people.

Our take

Tether is a solvent, highly efficient hedge fund masquerading as a payment rail. While S&P is technically correct about the capital structure risk, they miss the utility argument. In the Global South, users care about censorship resistance and dollar access, not credit ratings. Tether will likely continue to grow in emerging markets while USDC captures the regulated Western institutional flow.

Tether is currently a solvent, highly profitable, and operationally efficient shadow bank. However, S&P has correctly identified that its capital structure is misaligned with its asset risk. For the global financial system, the risk is not just that Tether breaks the buck, but that in doing so, it breaks the bond and digital asset market with it.

Actionable plays we see investors take:

- Long Regulated Infrastructure (COIN): As the gap between onshore and offshore stablecoins widens, institutions will be forced into regulated rails. Coinbase (partners with Circle/USDC) benefits from the flight to quality and the MiCA-driven exodus from USDT in Europe.

- Long Bitcoin (BTC): Tether’s aggressive accumulation of Bitcoin (now exceeding its equity buffer) creates a forced-buyer dynamic. Tether is effectively a programmatic bidder for BTC using the float from the global dollar trade.

Today’s Market Signals

- $12 trillion Charles Schwab says it will offer Bitcoin & Ethereum trading in early 2026. Link

Take care,

Marc & team

Download the PDF