SWIFT’s vampire attack on crypto

Hey, it’s Marc,

The “DeFi vs. TradFi” narrative was binary: the banks were the dinosaurs, and the asteroid was coming. Were we wrong? In the last months, the dinosaur didn’t just survive, it learned to fly. And the “SWIFT Killer” thesis might be dead now.

In a quiet trial orchestrated with BNP Paribas, Société Générale, and Intesa Sanpaolo, SWIFT proved it could settle tokenised bonds across fragmented blockchains using existing banking infrastructure. [RELEASE]

The message: SWIFT’s rails are not outdated; they are being upgraded.

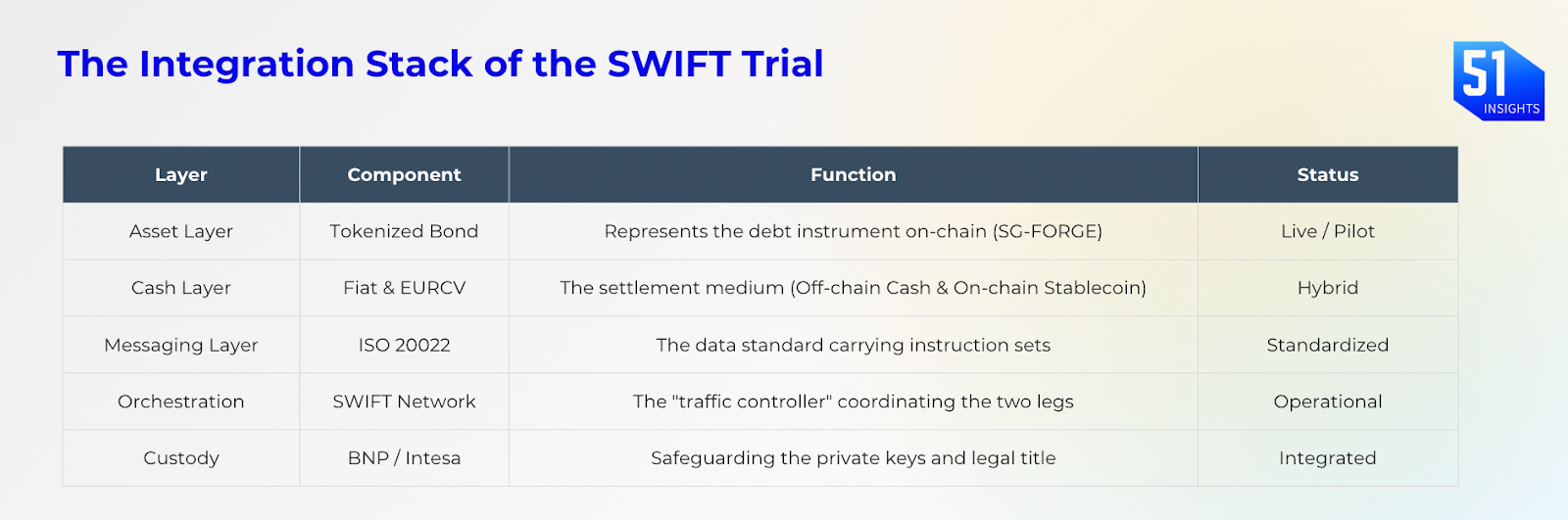

What happened

Swift, in collaboration with partners including BNP Paribas (custodian and paying agent), Société Générale – FORGE (DLT1 provider and issuer), and Intesa Sanpaolo (secondary custodian), has completed a series of trials for orchestrating tokenised bond transactions and cross-border payments.

The initiative demonstrated seamless delivery-versus-payment (DvP)2 settlement and lifecycle management across multiple blockchains and traditional systems, utilising ISO 20022 standards. Swift is now integrating a blockchain-based shared ledger into its infrastructure to enable real-time, 24/7 global transaction execution.

Be smart: SWIFT processes 68M messages daily. Now, it is building a blockchain-based shared ledger with Consensys and 30+ global institutions from 16 countries, targeting deployment across 200 countries.

Zooming in: The trial settled transactions using both fiat and EURCV (a regulated stablecoin by SG-Forge), solving the “atomic swap3” problem between legacy systems and digital assets. SWIFT’s shared ledger has two tiers.

- Tier 1 banks (JPMorgan, Citi, BNP) run validator nodes and have governance power.

- Tier 2 banks access via APIs as clients.

This proves the “Commercial Bank Money Token“ (CBMT) thesis. Banks prefer settling in digital fiat they control rather than volatile crypto assets or waiting for CBDCs.

The build up: Swift demonstrated secure tokenized assets transfers across public and private blockchains in 2023 experiments. September 2025: announced the Shared Ledger with Consensys. Same month: UBS proved banks could move on-chain assets using existing SWIFT messages via Chainlink. November 2025: ISO 20022 messaging went live.

Why this kills reconciliation: SWIFT historically just passed messages, banks updated their own records separately, creating mismatch risk. A shared ledger updates both sides simultaneously, creating a single source of truth and freeing trapped liquidity (here’s Swift’s take on that).

Why it matters

SWIFT as a state machine: Crypto startups bet on replacing SWIFT’s network. SWIFT just proved it can layer blockchain settlement under the existing network. Every bank already trusts SWIFT. Nobody needs to migrate. The 200B+ daily messages keep flowing through SWIFT - just with better back-end plumbing. They are absorbing the efficiency of the tech while rejecting the ideology. Hence, it is moving from a messaging utility to being a single source of truth for 11,000 institutions.

A threat to Layer 1s: The “SWIFT is slow” thesis was the primary value proposition for insurgent blockchains like Ripple or Stellar. That thesis is dead. By integrating Chainlink’s Cross-Chain Interoperability Protocol (CCIP, a universal standard for sending tokens and arbitrary messages on blockchains), SWIFT creates an abstraction layer that allows a bank to buy an Ethereum bond using a Corda cash account without leaving their legacy terminal. If SWIFT offers T+0 settlement with the identity verification banks legally require, the “moat” becomes insurmountable for permissionless chains.

Geopolitical defense: This upgrade makes the dollar stronger. The mBridge4 project (China, UAE, Thailand) already offers T+0 CBDC settlement, bypassing US sanctions. SWIFT’s move to a Shared Ledger is a direct defensive measure to neutralise mBridge’s technological advantage, as ~50% of its international payments volume is in USD. They are fighting the “US Dollar Lag” to prevent the Global South from defecting to faster, non-Western rails.

The rise of collateral demand: In T+2 settlement, banks hold massive liquidity buffers to bridge the gap between outflows and inflows. Mid-tier banks spend $100M+ annually on this trapped capital. But moving to real-time gross settlement creates a new problem: you can’t “net” trades at the end of the day. You need cash now. This creates massive demand for Intraday Repo (Repurchase Agreement), borrowing cash for minutes to settle a trade. This turns tokenised treasuries (like BlackRock’s BUIDL) into the new “oil” of the banking system. Banks will pledge BUIDL tokens to borrow stablecoins for settlement, turning dead collateral into working capital.

Our view

If this works, crypto companies betting on replacing payment rails might have miscalculated. You can’t out-distribute 11,000 banks with $150T in daily flow. The rails are upgrading faster than startups can scale.

So, while the settlement layer becomes more competitive, the asset origination layer is wide open. The opportunity for crypto players will be to build “Better Trains” (applications) that run on the rails; to focus on tokenising specific assets (Carbon Credits, Private Equity) rather than trying to replace the settlement layer.

Coming bills will regulate activities (who can issue stablecoins, who custodies assets), not the underlying technology. The winners will be crypto-native companies that partner with banks, not replace them.

Investor Alpha

The “Replacement Narrative” might be dead, both of payment rails and banks. The release also collapses the timeline of tokenisation.

Long Chainlink (LINK): Chainlink became TCP/IP for finance. The trial confirmed CCIP as the standard abstraction layer. If even a fraction of SWIFT’s $150T daily volume moves on-chain, it moves through CCIP. The “Chainlink Runtime Environment“ (CRE) is now critical infrastructure for performing settlement logic.

Long RWA infrastructure (Ondo Finance ONDO/ Ethena ENA): Tokenized treasuries (BUIDL, ONDO stablecoins) become the base collateral for intraday repo5 markets. BUIDL’s adoption as collateral on derivatives exchanges (Deribit, FalconX) is step one. ONDO’s integration with DeFi and regulated custody (Middle East focus) positions it for the institutional RWA flows. Here’s why: Real-time gross settlement creates intraday liquidity crunch. Banks can’t net trades at end-of-day anymore, they need cash now. ONDO’s tokenized treasuries become the repo collateral for these minute-long borrowing needs. Watch Payment L1s (XRP / XLM/ POL): The “cross-border payment token” thesis faces an existential crisis. If banks can settle instantly via a SWIFT Shared Ledger using regulated stablecoins, the utility of holding a volatile bridge currency like XRP for institutional transfer evaporates.

Watchlist:

- Jan 27: Federal Reserve two-day meeting, rate decision

- Jan: SEC Crypto Innovation Exemption window

- Jan: Spot crypto ETF decisions for altcoins

- Feb 2: Bank of Japan (BoJ) Summary of Opinions (Jan meeting)

- Feb 4–5: ECB Governing Council monetary policy meeting

- Feb 5–6: Digital Assets Forum 2026, London

- Feb 9: Liquidity Summit 2026, Hong Kong

- Feb 10–12: Consensus Hong Kong (CoinDesk)

- Feb 11: US CPI (Jan) release

- Feb 12: US PPI release

- Feb 17–21: ETHDenver 2026

- Feb 18: FOMC minutes for Jan 27–28 meeting

- Q1’26: Kraken IPO window

- Q1’26: Hong Kong stablecoin licensing regime

- Q1’26: Singapore stablecoin framework launch

Market signals

- WEF on stablecoins. Link

- HK to issue stablecoin licenses in Q1. Link

- Strategy buys $2.1b BTC, largest buy in 1+ year. Link

- Central Bank of Iran has acquired US dollar stablecoins worth $0.5B. Link

That’s it for now.

Marc & Team

Appendix

- The need for rich data in a shared ledger paradigm (SWIFT)

- How stablecoins can expand financial access to the most underserved and unbanked (WEF)

- European Banks Need to Act Now on Instant Payments and Intraday Liquidity (BCG)

DLT primarily refers to Distributed Ledger Technology, which is a decentralized, digital infrastructure that enables the simultaneous access, validation, and updating of records across a network spread across multiple entities or locations. Unlike traditional centralized databases that rely on a single authority (like a bank), DLT removes the need for a central, trusted third party, offering a “single source of truth” that is shared and synchronized in real-time. ↩

Delivery-versus-payment (DvP) is a crucial settlement system in financial markets ensuring securities are only transferred to a buyer when payment is simultaneously received from the buyer, and vice versa for the seller, preventing risk where one party delivers but the other fails to pay or deliver. It links securities and funds transfer systems, guaranteeing an “all or nothing” exchange, protecting both parties from default and ensuring market stability by mitigating risks like principal risk (losing money/securities) and liquidity issues. ↩

An atomic swap is a trustless, peer-to-peer method for directly exchanging cryptocurrencies between different blockchains, using smart contracts (specifically Hash Time-Locked Contracts or HTLCs) to ensure the trade happens entirely or not at all, eliminating intermediaries like centralized exchanges. This “all-or-nothing” nature, inspired by the concept of “atomicity,” secures the transaction by locking funds in a cryptographic escrow until both parties fulfill their parts, preventing loss and counterparty risk. ↩

The mBridge Project (Multiple CBDC Bridge) is a major initiative by central banks (China, Hong Kong, UAE, Thailand, Saudi Arabia) led by the BIS Innovation Hub to create a blockchain-based platform for faster, cheaper, and more efficient cross-border payments using Central Bank Digital Currencies (CBDCs). It aims to reduce reliance on traditional correspondent banking, offering direct peer-to-peer transactions, increased transparency, and lower costs, potentially reshaping global finance by providing an alternative to dollar-centric systems, with China’s digital yuan being dominant in current volumes. ↩

An Intraday Repo (Repurchase Agreement) is a short-term funding tool where financial institutions borrow cash for a few minutes to hours within the same trading day, selling securities as collateral and repurchasing them later the same day, rather than overnight, to manage liquidity spikes, avoid daylight overdrafts, and generate income on idle cash at lower costs than traditional repos. It provides crucial intraday liquidity, enhances cash flow management, and is increasingly facilitated by new DLT (Distributed Ledger Technology) platforms for real-time processing and settlement. ↩