Stripe doesn’t need bank

Hey, it’s Marc!

For over 15 years, Stripe processed payments. It needed banks to hold the money. It needed card networks to move it. It needed partners for everything. That just changed.

Now, Stripe owns a bank. Kind of. On February 17, 2026, the OCC conditionally approved Bridge, Stripe’s $1.1 billion stablecoin acquisition, for a national trust bank charter. [RELEASE]

👉PRO: Download the PDF at the bottom

What happened

The OCC greenlit a national trust bank charter1 for Bridge, Stripe’s stablecoin acquisition, in February 2026, but conditionally. Bridge National Trust will issue stablecoins, custody digital assets, and manage reserves under direct federal oversight. [RELEASE]

This follows December 2025 approvals for Ripple, Circle, Paxos, BitGo, and Fidelity Digital Assets. WLFI, linked to the Trump family, applied for a national trust bank charter in January 2026 to issue and custody its “USD1” stablecoin. [See full analysis]

What makes Bridge different? Bridge has Stripe’s $1+ trillion in annual payment volume behind it.

Zooming in: The charter is not yet fully effective. Bridge has said it can begin operating its stablecoin and custody services only once it receives final OCC approval, and there is no public timeline for when that will happen.

But, the important question is, what makes stablecoins so significant now? Stablecoins has crossed over $307B in market cap in 2026. And, they are quietly becoming infrastructure. From cross-border remittances to corporate treasury management, the use cases have expanded far beyond speculative trading.

By the data: Stablecoins processed $6T in cross-border payments in 2024. Right now, the current share of stablecoin in cross-border payment markets ($194.8T) is <1% with a total $16.5T base total addressable market.

And, that number tells only part of the story. The real shift is structural: stablecoins are no longer operating in a regulatory gray zone by default. With the passage of the GENIUS Act in July 2025, the first federal framework for payment stablecoins, the floodgates have opened for mainstream financial institutions to enter the space.

Stripe was one the first incumbents to enter the space.

- Fidelity Investments launched the Fidelity Digital Dollar (FIDD) in February 2026.

- SoFi became the first national bank to issue a stablecoin on a public blockchain, launching SoFiUSD in December 2025.

- JPMorgan launched its deposit token JPMD on Coinbase’s public layer-2 blockchain Base.

- Custodia Bank released the Avit deposit token on Ethereum with Vantage Bank.

And much more.

Here, this approval will support Stripe’s Open Issuance, a platform service that allows its customers, fintechs, enterprises, and platforms, to launch their own white-labeled stablecoins.

Stripe now owns the entire lifecycle of money: Stripe has moved beyond transaction facilitation. Now, it combines Bridge’s federal charter rails (Stablecoin issuance), Lemon Squeezy’s global tax compliance (tax & MoR), the movement (rails) and the new Agentic Commerce Protocol (co-built with OpenAI) to monetize AI agents as a transacting consumer class.

What you must know about the GENIUS Act: The GENIUS Act established a dual-track system:

- Subsidiaries of Insured Depository Institutions (IDIs): Traditional banks can issue stablecoins through separate, bankruptcy-remote subsidiaries.

- Federal Qualified Payment Stablecoin Issuers (FQPSI): Non-bank entities (like Bridge or Circle) can obtain a federal charter from the OCC to issue stablecoins.

Sections 5(h) and 7(f) of the GENIUS Act are the most consequential. They preempt state-level money transmitter licensing requirements for federal issuers.

- Old World: A fintech like Stripe or Coinbase needed 49 distinct state money transmitter licenses (MTLs) to operate nationally. This “patchwork” was costly, slow, and operationally fragile. It required maintaining relationships with dozens of state regulators and navigating conflicting definitions of “money transmission.”

- New World: A single federal OCC trust charter allows nationwide operation. This creates a “bespoke fintech license“ that functions as a national payments rail, independent of the legacy banking system. This federal preemption makes the national trust charter so valuable; it dramatically reduces compliance overhead and creates a unified regulatory interface.

The analysis that follows is for PRO subscribers.

You just saw the rule change. What you haven't seen is who wins, who's dead, and how to position before the rest of the market catches up. PRO ONLY:

- Why it matters (instant settlement unlock, USDT kill switch, the netting catch, banks terrified)

- Investor Alpha (Circle, Coinbase, onshore challengers, allocator advice, M&A wave)

- Watchlist + Full PDF

Why it matters

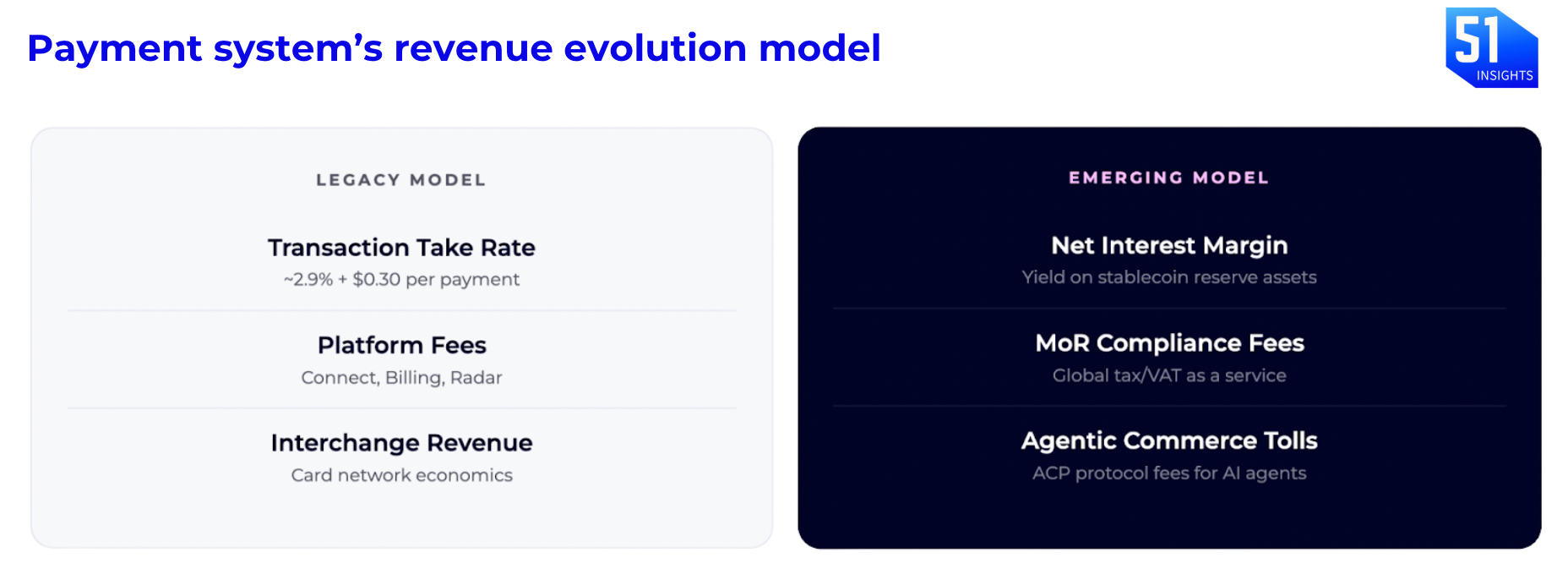

- The yield just moved in-house. The old model: fintechs rent a license from Paxos or Circle, give up the float, take a small rev-share. The new model: own the OCC charter, park reserves in Treasuries directly, capture 100% of the net interest margin. Stripe processes trillions in volume. Even a fraction of that float, at current ~5% T-bill yields, is a multi-billion-dollar income stream that never existed before. This is a business model transformation from fee capture to yield capture. At scale, it rivals Stripe’s core payments margins.

Banks have two problems now, not one. First, deposit displacement. If Stripe’s customers park working capital in Bridge-issued stablecoins earning Treasury yield, regional banks lose their cheapest funding source. When deposits leave, lending contracts, and NIMs compress. Second, the payment bypass. Stripe processed $58B in cross-border volume in 2025. Those transactions ran through card networks and correspondent banks at 2–3% FX/interchange cost. On stablecoin rails, the marginal cost is near zero. That margin doesn’t go to Visa or Deutsche Bank anymore. It stays with Stripe. The Bank Policy Institute sees this clearly; they’ve formally opposed Bridge’s charter, calling stablecoin reserve management a “core banking function” that requires FDIC insurance2. They’re not wrong that it’s banking. They’re just too late to stop it.

AI agents are the new buyers. Stripe and OpenAI’s Agentic Commerce Protocol already powers Instant Checkout in ChatGPT and Microsoft Copilot. Etsy, Urban Outfitters, Coach, and Glossier are onboard. Stablecoins are the native currency for these agents, programmable, instant, 24/7. Credit cards can’t compete with software that never sleeps.

Investor Alpha

Stripe isn’t building a crypto product. It’s assembling a full-stack financial OS: charter (Bridge), wallets (Privy), compliance (Lemon Squeezy), and AI commerce (OpenAI protocol), backed by 4M+ merchants. At $140B, it’s the most valuable private fintech on Earth, and it owns the pipes, the float, and the AI distribution channel. Don’t wait for the IPO. This is already the most consequential fintech story of 2026.

The opportunities are:

- Fintechs: The Genius Act permits them to vertically integrate OCC charter and issue stablecoins.

- Banks: They can partner with stablecoin issuers and custodians and tokenise deposits to retain FDIC insurance and pay yield, a structural advantage over stablecoins.

- Merchants: The biggest opportunity here is agentic commerce with stablecoin enabling lower payment costs and near-instant settlements.

- Asset Managers: The GENIUS Act creates a pathway for tokenised money market funds to function as stablecoin-adjacent instruments, allowing asset managers to offer yield-bearing, programmable cash equivalents. Firms like BlackRock and Franklin Templeton are already positioned here.

That said, the risks across all of these are real and should not be understated. The rules are clearer than they were, but the plumbing is still being built. Anyone moving into this space should be honest about what they don’t know yet, because the infrastructure underneath stablecoins, the technology, the reserves, the legal frameworks, is still young and untested at scale.

Watchlist:

- Mar 1–2: Crypto Expo Europe (Bucharest)

- Mar 11: US CPI (Feb) release – critical for Fed rate cut expectations

- Mar 17–18: DC Blockchain Summit (Chamber of Digital Commerce)

- Mar 18: FOMC Interest Rate Decision & Summary of Economic Projections

That’s it for now.

Missed last week? Access all our CEO notes here.

Marc & Team

Download the PDF

A national bank charter is a federal license granted by the Office of the Comptroller of the Currency (OCC) that authorizes a financial institution to operate as a bank across the United States. These institutions are governed by the National Bank Act, subject to strict federal regulations, and usually feature “National Association” or “N.A.” in their title. ↩

FDIC insurance (Federal Deposit Insurance Corporation) is a U.S. government guarantee protecting depositors’ money, up to per depositor, per ownership category, if an insured bank fails. It covers checking, savings, and CDs, but not investments like stocks or mutual funds. Since 1933, no depositor has lost insured funds ↩