BNY Mellon rewrote how money moves

Hey, it’s Marc,

On January 9, 2026, the Bank of New York Mellon, guardian of $57.8T in assets, rewrote the rules of money.

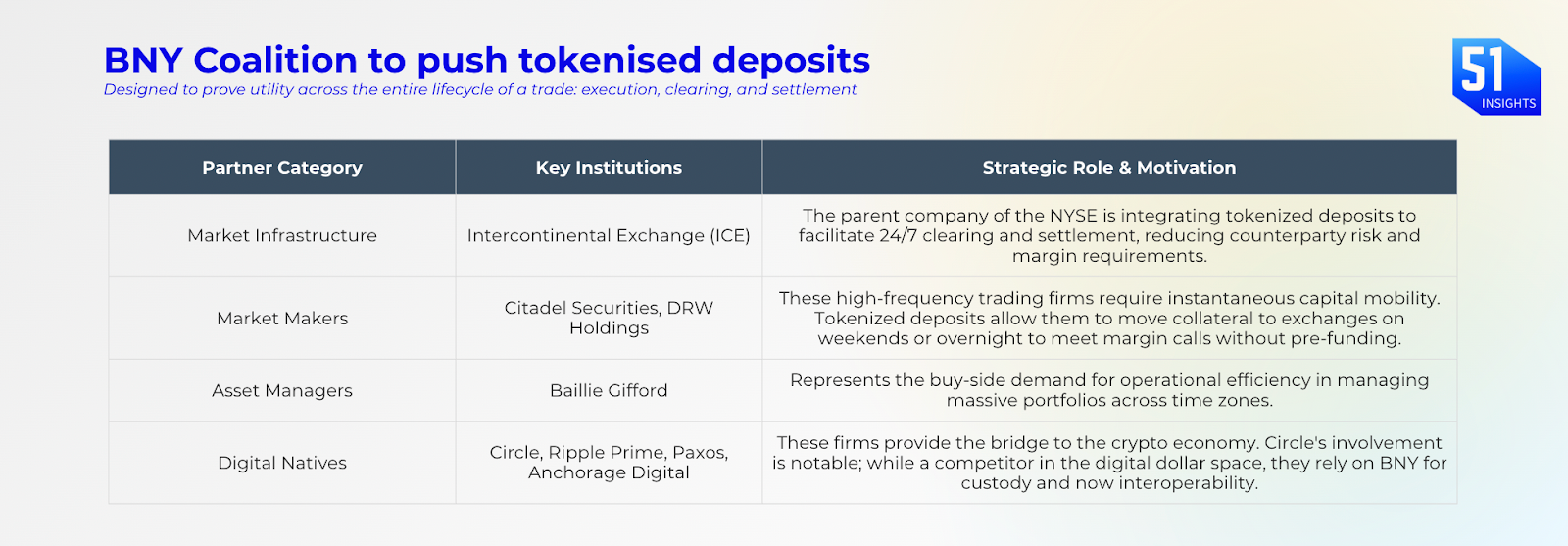

BNY went live with tokenized deposits: 24/7, programmable, atomic settlement on private blockchains with six initial clients: ICE (owns NYSE), Citadel Securities, DRW Holdings, Ripple Prime, Baillie Gifford, and Circle. Same dollar. Same FDIC insurance. Crypto speed. [RELEASE]

The move kills two narratives at once. First: “crypto will disrupt banking.” Second: “stablecoins are the future.”

What’s emerging is messier and far more powerful: a two-tier monetary system where banks keep the yield, insurance, and control, and crypto gets the plumbing.

Let’s unpack.

PS: Today, NYSE announced 24/7 tokenized securities trading today – made possible by BNYs tokenized deposits. We’ll share a CEO Note on that tomorrow.

What happened

BNY launched tokenized deposits on the Canton Network, a privacy-enabled interoperability protocol designed by Digital Asset. Clients (Citadel Securities, Intercontinental Exchange, Circle) can now move commercial bank money across blockchains 24/7 with atomic settlement and zero counterparty risk.

A $100M deposit becomes $100M in tokens. Transfers and redemptions are instant. No T+2 settlement window. No trapped capital over weekends.

The architecture matters. Unlike public chains (Ethereum, Solana), Canton keeps transaction data private between parties. Citadel’s collateral positions don’t broadcast to competitors. ICE’s margin calls settle without SWIFT delays.

For institutions, this solves the “privacy vs. decentralization” tradeoff.

Marc Baumann

Marc Baumann Marc Baumann

Marc Baumann Marc Baumann

Marc Baumann

Be smart: BNY currently provides fund services for over 80% of digital asset exchange-traded products (ETPs) in the U.S., Canada, and EMEA, and manages over 50% of tokenized fund assets globally.

Stepping back: BNY’s integrated platform provides secure custody for digital assets, financing solutions, and Data on Chain capabilities.

- 2023+: Became a key participant in major industry pilots, including Singapore’s Project Guardian for cross-border tokenized FX and the Canton Network.

- October 2025: Was appointed to provide the foundational infrastructure for WisdomTree’s digital asset initiatives.

- November 2025: Introduced the BNY Dreyfus Stablecoin Reserves Fund, a government money market fund for U.S. stablecoin issuers to hold reserves under GENIUS Act frameworks.

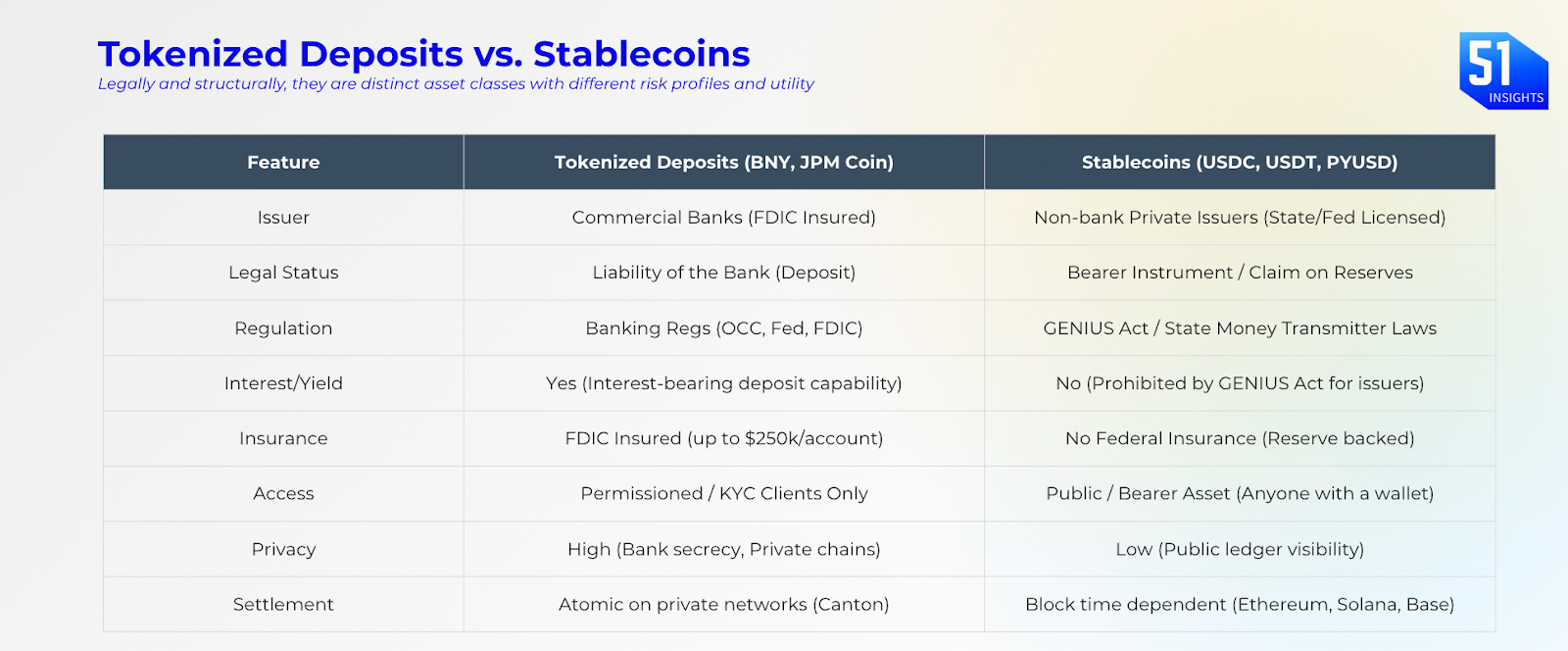

Banks and financial institutions are taking the most valuable feature of tokenisation: programmability and 24/7 settlement, and folding it inside regulated deposits.

Why it matters

- It is about displacement and time: Citi projects tokenized deposits could handle $100–140T in annual transaction flow by 2030. Stablecoins, the public alternative, are projected at $95–200T in velocity, but that’s misleading. A dollar in a stablecoin circulates faster than a dollar in a tokenized deposit because it’s used for retail payments and DeFi. But for the $2.5 quadrillion derivatives market, for margin optimization, for collateral management, where trillions of dollars sit idle every weekend, tokenized deposits win on utility. In November, JPMorgan first introduced tokenized deposits with JPMD.

- Banking’s real weakness exposed: The GENIUS Act banned stablecoin issuers from paying interest. The stated reason: prevent “shadow banking” and protect the deposit franchise. The actual effect: created a regulatory moat that only banks could exploit. BNY’s tokenized deposits yield interest. Circle’s USDC cannot. The crypto industry can offer you 4.5% via the “rewards loophole.” Banks now offer something better: 4% yield + atomic settlement + FDIC insurance + programmability. The Clarity Act is trying to close the rewards loophole. If it does, stablecoins lose their last economic advantage over tokenized deposits. If it doesn’t, banks have already positioned themselves as the premium alternative.

- Capital efficiency unlock is real: Margin calls in derivatives markets currently happen on banker’s hours. A Sunday volatility spike at ICE forces Citadel to pre-fund cash all weekend or face liquidation. $100M sits idle as insurance against a Monday morning panic. BNY’s tokenized deposits run 24/7/365. That volatility spike? Citadel pledges tokens to ICE’s smart contract in seconds. The collateral moves instantly. The capital that was trapped is now free. Multiply this across trillions in notional derivatives positions, and you’re talking about billions in released working capital. This is why ICE (the world’s largest clearinghouse) is a launch partner, to reduce risk at scale.

Our view

By 2030, a dual-tier monetary system will emerge:

- Tokenized Deposits: The dominant rail for wholesale, institutional, and B2B high-value transactions, integrated into the fractional reserve system and yielding interest.

- Stablecoins: The dominant rail for retail, P2P, and cross-border remittances, functioning as digital bearer instruments but increasingly constrained by yield prohibitions.

Investor Alpha

Crypto narratives frame this as “banks stealing crypto’s thunder.” That’s surface-level. What’s actually happening is more ruthless: traditional finance identified the best features of blockchain (atomicity, programmability, 24/7 settlement) and integrated them into the existing system without surrendering any of its advantages (regulation, insurance, yield, liquidity). They’re not losing institutional capital to crypto. They’re capturing it by becoming better crypto.

- Long BNY (BK) and JPMorgan (JPM): Both are the “Layer 0” infrastructure for institutional blockchain adoption. Every institution that wants regulated, insured, programmable settlement needs to custody with them. This is a profitability story. They’re keeping capital inside the perimeter while taking custody fees on both ends (stablecoin backing + tokenized deposits).

- Short regional banks into this news (KRE): They lack the tech budget to build tokenized deposit platforms and the scale to compete. Watch for quiet deposit migration to G-SIBs in the name of “operational efficiency.” This is the silent consolidation nobody is talking about.

- Watch Circle and Coinbase at risk (CRCL, COIN): Stablecoins’ value proposition was “better than bank money.” Now bank money IS blockchain money. Their only path forward is if the Clarity Act preserves the rewards loophole, and Coinbase has already signaled it will walk if the compromise bans passive yield. A walking Coinbase = a dead Clarity Act. A dead Clarity Act = a fractured regulatory landscape that hurts, not helps, USDC adoption. Execution risk is extreme.

Watchlist:

- Jan: USAT launch by Tether (expected)

- Jan 13: Consumer Price Index data for December 2025; heavily influence the January 27-28 meeting

- Jan 15: Clarity Act (H.R.3633) Senate markup

- Jan 27: The Federal Reserve will convene for two days, with the rate decision

- Jan: SEC Crypto Innovation Exemption

- Jan: Spot crypto ETF approvals for altcoin

- Q1’26: Kraken IPO

- Q1’26: Hong Kong Stablecoin licensing

- Q1’26: Singapore Stablecoin framework

Market signals

- New York Stock Exchange announces 24/7 tokenized securities trading. Link

That’s it for now.

Marc & Team

Appendix

The life cycle of BNY tokenised deposit:

- Minting: A client (e.g., Citadel) sends $100M via Fedwire (or internal transfer) to their BNY omnibus account.

- Tokenization: BNY’s private ledger (Canton) mints 100M “BNY-USD” tokens to Citadel’s wallet address on the network. These tokens are legally defined as a deposit claim against BNY.

- Transfer: Citadel pledges these tokens to ICE’s clearinghouse smart contract as margin.

- Atomic Settlement: The transfer is atomic. The ledger updates instantly. ICE now holds the claim on the BNY deposit. No money has left BNY; the liability has simply shifted from Citadel to ICE.

- Redemption: ICE can redeem the tokens for fiat in their BNY account, or hold them to pay other members of the network.