Re-Engineering of US Derivatives Markets

The Federal Reserve just lost control of its most important tool: the collateral hierarchy.

For seventy years, the Fed’s power flowed from a single choke point - deciding what counts as “money good“ collateral. Treasury bonds. Agency MBS. Investment-grade corporates. But on December 8, 2025, CFTC changed that. It has approved Bitcoin, Ethereum, and USDC as collateral in the U.S. derivative market, without touching the traditional banking system at all. [ANNOUNCEMENT]

Let’s unpack.

Download the PDF below

Today’s Market Signals

Strategy buys $963m BTC, BitMine buys 138k ETH. Link

SEC ends Biden-era investigation into Ondo Finance. Link

HashKey launches Hong Kong IPO seeking up to $214.7M. Link

Tether gains Abu Dhabi’s approval to expand USDT. Link

What happened

CFTC has permitted Bitcoin, Ethereum and USDC (high-quality liquid assets) to serve as margin collateral for Futures Commission Merchants (FCMs) under a pilot program. The regulator has effectively removed the old rule that forced digital asset holders to sell their tokens for cash before they could hedge.

Bitnomial is the first exchange to receive approval for this model. [RELEASE]

This is supported by the GENIUS Act, passes earlier in 2025.

The CFTC pilot uses this new framework to remove the rule Staff Advisory 20-34, which stopped brokers from holding crypto in segregated customer accounts. That old rule meant FCMs could not directly custody crypto, which forced many traders to sell their tokens for cash whenever they needed margin. By withdrawing the rule and adding new guidance at the same time, the pilot creates a two-part change: FCMs like Citi, Goldman, and JPMorgan can now hold digital assets for clients, and they are also allowed to treat Bitcoin, Ether, and USDC as eligible margin.

It also challenges the long-standing dominance of the U.S. Treasuries as the safest and most liquid collateral, pushing major global banks to upgrade their custody and clearing systems.

Zooming in: With this CFTC pilot,

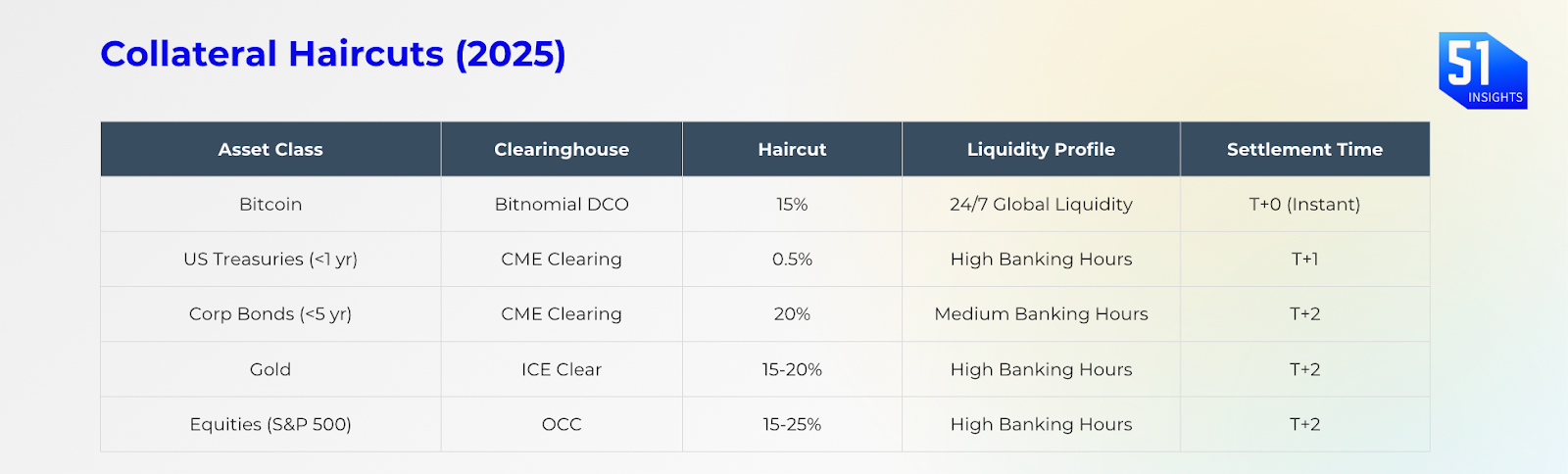

- FCMs can treat Bitcoin, ETH, and payment stablecoins (like USDC) as regulated margin collateral, with DCO-set haircuts and oversight.

- As FCMs can now take BTC/ETH as margin, they can support contracts denominated and settled in the same asset.

- Previously, FCMs had to treat crypto collateral as zero for capital purposes, forcing them to plug deficits with their own cash. The pilot allows them to count digital assets at haircut-adjusted values.

- Because payment stablecoins already have clear rules under the GENIUS Act, FCMs can now treat these approved stablecoins much more like high-quality cash in their margin and customer-fund calculations.

- Since stablecoins settle continuously across blockchains, the pilot effectively introduces the first step toward real-time collateral flows in U.S. markets.

The program limits the first 3 months to BTC, ETH, and payment stablecoins, plus mandatory weekly reporting.

Marc Baumann

Marc Baumann

A practical example of how this works in real time comes from Bitnomial.

The Bitnomial model: Bitnomial runs a fully integrated stack, exchange, clearinghouse, and settlement, instead of relying on third-party clearing.

In the old model, an FCM sits in the middle. When a margin is called, the FCM fronts the payment to the clearinghouse and then chases the client. This creates lag and credit risk. In Bitnomial’s model, the collateral (e.g., Bitcoin) already sits inside the DCO/FCM wallet, so liquidations happen programmatically and in real time.

It applies a 15% maintenance margin haircut (percentage discount applied to the asset’s value when posted as margin) on Bitcoin.

Why it matters

- 24x7 markets: The U.S. banking system runs on weekday hours, but crypto never closes. The CFTC pilot begins to bridge that gap by letting firms post stablecoins as margin, creating the first real pathway to round-the-clock collateral movement in regulated markets. Bitnomial shows what this looks like in practice: collateral sits inside the clearing system and can be liquidated instantly, which cuts credit risk and speeds up the entire process. But it also exposes a new fault line. If Bitcoin collapses on a Saturday, banks still can’t move dollars to cover losses. Unless U.S. payment rails move toward 24/7 settlement, the derivatives market may advance faster than the banking system can support.

- New challenge/ opportunity for FCMs: Instead of just holding cash and securities, they now have to safeguard private keys or rely on custodians like Coinbase Custody or BNY Mellon to store Bitcoin and Ethereum. Banks like JPMorgan and Goldman Sachs need blockchain node access or high-assurance custodial APIs to access Bitcoin. This also provides a clear path for adopting digital assets for them.

- The end of Bitcoin treasury premium: Companies like MicroStrategy used to trade at a premium because they were one of the only ways for big investors to get extra-leveraged exposure to Bitcoin. Now that Bitcoin itself can be used as regulated collateral, institutions can build the same strategy on their own through futures. As this access opens up, MicroStrategy is no longer the “only game in town,” so its premium is likely to shrink.

Marc Baumann

Investor Alpha

By allowing BTC/ETH/USDC as collateral, U.S. FCMs (Futures Commission Merchants) now offer the same capital efficiency as offshore venues. This removes the extra costs and delays that previously forced people to use risky foreign platforms, making the safer U.S. market the obvious choice for big investors again. Essentially, instead of trying to ban offshore competition [Binance ($1.7T monthly volume)], the U.S. built a better system at home that convinces investors to voluntarily reveal their identities in exchange for safety and speed.

The Trade: Long Infrastructure, Short Proxies.

The GENIUS Act doesn’t just legitimize crypto; it financializes it. We are moving from a “buy and hold” asset class to a “use as collateral” asset class. This transition favors the picks-and-shovels providers who manage the plumbing over the proxy bets that thrive on scarcity and friction. Capital efficiency is the new alpha.

Actionable plays:

- Coinbase (COIN): Coinbase Derivatives Exchange (CDE) can now offer a more diverse suite of products, including margined futures contracts for various digital assets. Plus, this will also increase the adoption of USDC (co-founded by Coinbase). Trade on Robinhood

- BlackRock (BLK): BlackRock manages the Treasuries behind USDC through Circle. Under the GENIUS Act, those reserves must stay in T-bills and repo, so any growth in USDC as derivatives collateral boosts BlackRock’s AUM. More crypto trading → more USDC demand → more Treasury buying → more revenue for BlackRock.

- Companies providing the custody for this collateral (e.g., Coinbase Custody, Bank of New York Mellon) are the immediate beneficiaries of the reporting requirements.

Challenge: Crypto trades nonstop, but the banking system shuts down on weekends. So if prices crash on a Saturday, firms can’t move dollars to meet margin calls, forcing exchanges to sell assets in thin weekend markets just to protect themselves.

The countermeasure: The SEC and CFTC are reviewing “Blueprint Tokenised Collateral” proposals that use tokenised T-bills and 24/7 stablecoins to fix the weekend gap. The logic: if assets trade 24/7, the collateral money backing them must trade 24/7 too.

Watchlist

- Dec 10: U.S. Federal Reserve: 0.25% interest rate cut (expected)

- Dec 15: SEC roundtable (crypto task force)

- Dec 15: Cboe Global Markets will launch the first U.S.-regulated perpetual-style futures contracts (PBT and PET)

- Dec: USAT launch by Tether (expected)

- Dec: Clarity Act (H.R.3633) Senate vote (expected)

- Dec 31: Europe’s MiCA full enforcement (Austria, Germany, and Spain) ends

Take care,

Marc & team

Download the PDF

🙌 Work with us: We arm financial institutions and digital asset leaders with bespoke research, thought leadership to shape the most important conversations, scale trust, and win business.