Will Strategy's flywheel break?

Hey, it’s Marc.

Everyone is watching Bitcoin’s chart, but JPMorgan is watching the index committees. The bank warns MicroStrategy faces a silent, structural threat: expulsion from global equity benchmarks. [NEWS]

This would trigger billions in forced selling, crush the Net Asset Value (NAV) premium, and effectively end the Digital Asset Treasury model. The infinite money glitch might be over.

Let’s unpack.

👉PRO readers: Download the PDF

What happened

On October 10, 2025, MSCI released a consultation paper proposing a new rule: exclude “Digital Asset Treasury” (DAT) firms from its MSCI Global Investable Market Indexes (GIMI), the benchmark against which trillions of dollars in institutional capital are measured. A DAT is defined as any entity where digital assets make up 50% or more of total assets.

The final decision drops January 15, 2026.

- The Impact: JPMorgan analyst Nikolaos Panigirtzoglou estimates exclusion would trigger $2.8B in automatic selling from MSCI-tracking funds. If S&P and FTSE follow, the forced outflow hits $8.8B.

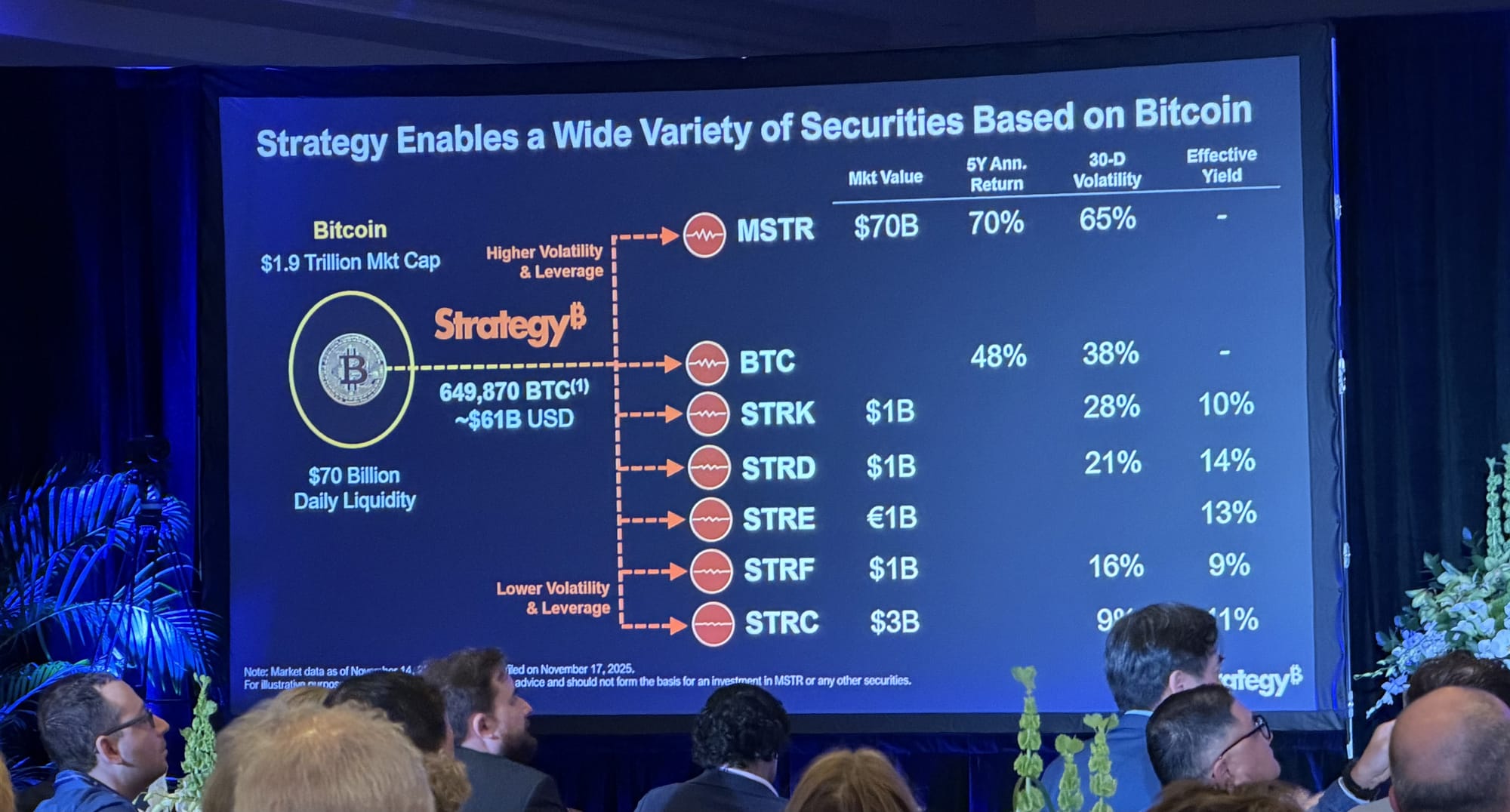

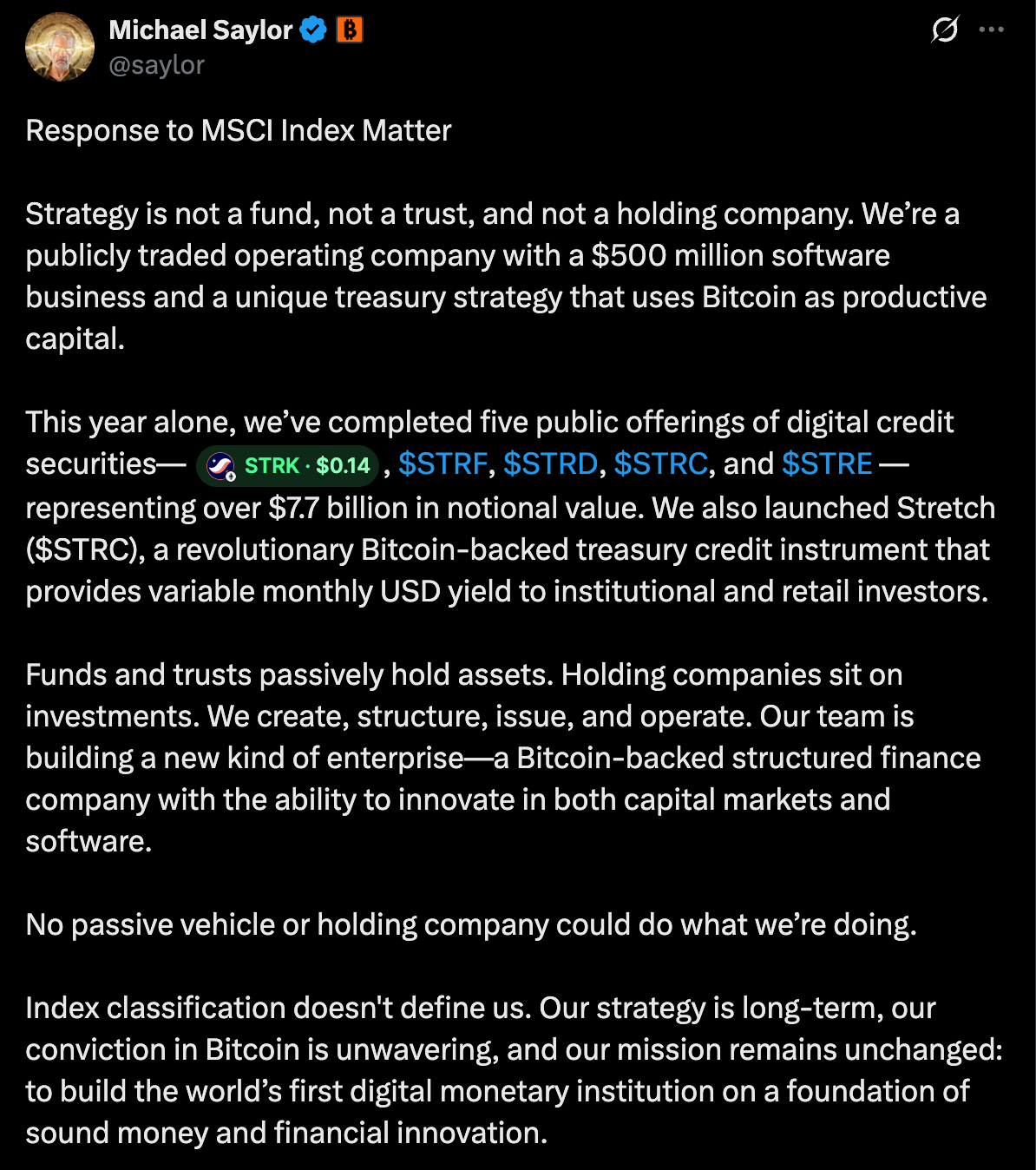

- The Defense: MicroStrategy argues it is an operating software business (generating $500M revenue), not a passive holding company or ETF wrapper.

Precedent: This mirrors Snap’s 2017 exclusion, which permanently altered its liquidity and cost of capital.1

Why it matters: The death of the premium. MicroStrategy’s valuation—and its ability to buy Bitcoin—relies entirely on its stock trading at a premium to its Net Asset Value (NAV). This premium allows Michael Saylor to issue equity and convertible debt to buy Bitcoin accretively. Index inclusion guarantees passive buying pressure, which supports that premium.

If MicroStrategy loses its index spots, its shares become harder to trade, its borrowing costs rise, and its ability to keep raising money to buy more bitcoin becomes much weaker. The whole “buy bitcoin → stock rises → raise more money → buy more bitcoin” cycle starts to break down.

- In the index: Passive buying supports the premium → MSTR issues paper → buys BTC → NAV rises.

- Out of the index: Passive selling crushes the premium → Issuance becomes dilutive → The flywheel stalls.

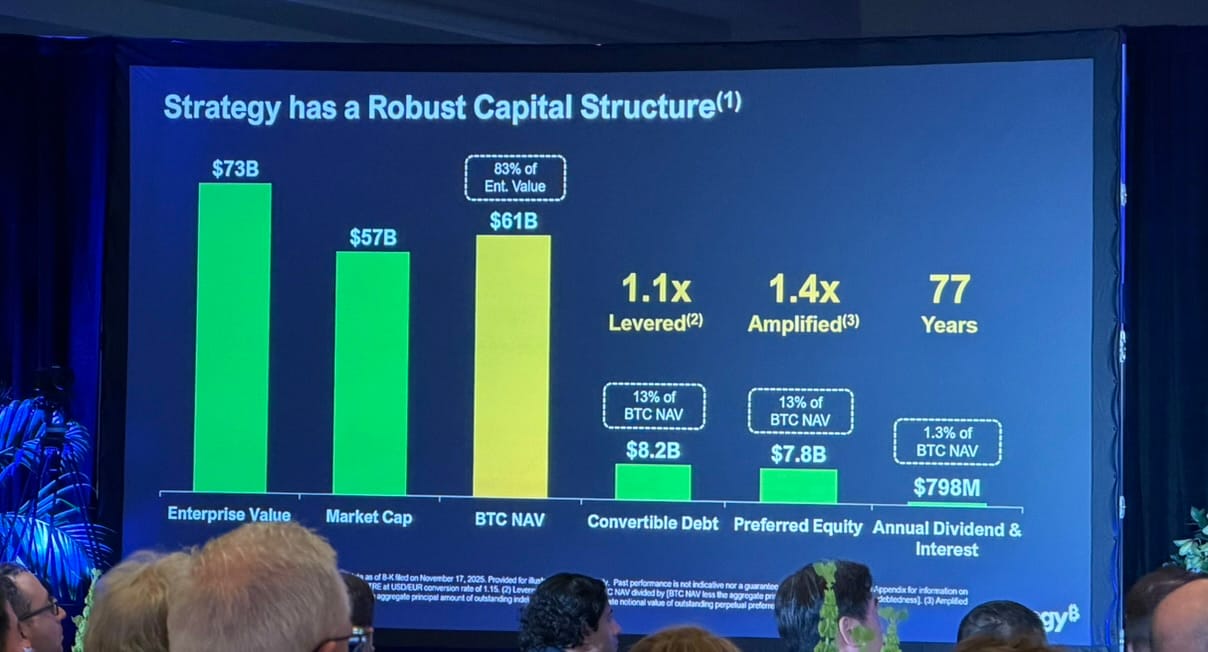

The cost of capital shock. MSTR’s convertible bonds trade at near-zero coupons because investors pay for the embedded volatility. If index exclusion kills liquidity and compresses the premium, volatility drops. Investors will stop accepting 0% yields and demand high-yield spreads (5-8%+). This effectively shuts down the cheap leverage machine.

The risk: MSTR’s convertible notes are unsecured. There is no collateral call if Bitcoin drops. Bondholders cannot force liquidation until maturity.

Zooming in: Since 2020, MicroStrategy has executed an unparalleled strategy: repeatedly raising capital (via equity, convertible debt, and, more recently, high-yield preferreds) to purchase a hoard of Bitcoin, reaching over 649,000 BTC by November 2025. This positioned MicroStrategy as the “gateway equity” for institutional and retail investors seeking regulated Bitcoin exposure. This transformed MSTR into a core component of indices like the Nasdaq 100, MSCI USA, and MSCI World.

MicroStrategy’s response: In response, MicroStrategy pushed back hard on the “fund” narrative. After the MSCI announcement, Michael Saylor emphasised that the company is an operating business, not a fund, trust, or holding company, anchored by a $500M software line and a treasury strategy that treats Bitcoin as productive capital.

UPDATE: On December 1, the company announced a massive $1.44 billion USD reserve to guarantee debt and dividend payments. Why? Because the stock is now trading at a discount to its Bitcoin holdings. With the premium gone, the “infinite money glitch”—issuing expensive equity to buy cheap Bitcoin—is over.

Investor Alpha

The “Flywheel” is fragile. The market is pricing MSTR as a tech stock, but MSCI views it as a levered holding company. Even a single MSCI exclusion is disruptive, but a cascade across S&P and NASDAQ would decapitate the “Crypto Equity” asset class. While management has stated they will never sell Bitcoin, debt covenants (though currently loose) or a collapse in the stock price could force their hand. The feedback loop works both ways: Selling Bitcoin lowers NAV -> lowers stock -> forces more selling.

- The Arbitrage Play (MSTR vs. BTC): Many hedge funds are executing a classic convertible arbitrage strategy. They buy the MSTR convertible bond (long volatility/gamma) and short sell the MSTR common stock (delta hedging). This profits from the mispricing between the bond and the stock.

- Volatility Straddle: The January 15 decision is a binary event. Buying straddles (options betting on a large move in either direction) on MSTR for late January captures the inevitable volatility of the ruling, regardless of the outcome.

Takeaway: The smart money is preparing for the premium to collapse. Many investors ensure that their exposure to Bitcoin is direct (Spot ETFs) rather than levered through a corporate structure facing an existential governance threat.

Watchlist

Take care,

Marc & team

Download the PDF

🙌 Work with us: We arm financial institutions and digital asset leaders with bespoke research, thought leadership to shape the most important conversations, scale trust, and win business.

Strategy’s situation echoes Snap’s in 2017, when the company was shut out of major indices because its no-vote share structure angered large investors who then pushed index providers to act. With no way to influence Snap directly, asset managers pressured S&P and FTSE to rewrite their rules, and Snap was effectively exiled from key benchmarks, raising its cost of capital for years. ↩