BNY Mellon’s $55T Bet on Tokenized Banking

The world’s largest custodian with $55.8T in AUM, BNY Mellon, is actively exploring the use of tokenised deposits for enabling institutional client payments over distributed ledger technology (DLT) rails. [NEWS]

The message is clear: Existing payment rails are expensive, and institutions will switch to blockchain infrastructure if it saves cost and time for them.

Why it matters: BNY Mellon’s Treasury Services unit processes roughly $2.5T in payments each day, making the shift to instant, 24/7 settlement capabilities a systemic necessity. The move signals accelerating institutional blockchain adoption with major cost-efficiency gains up to 30%.

Let’s dig in.

What’s happening

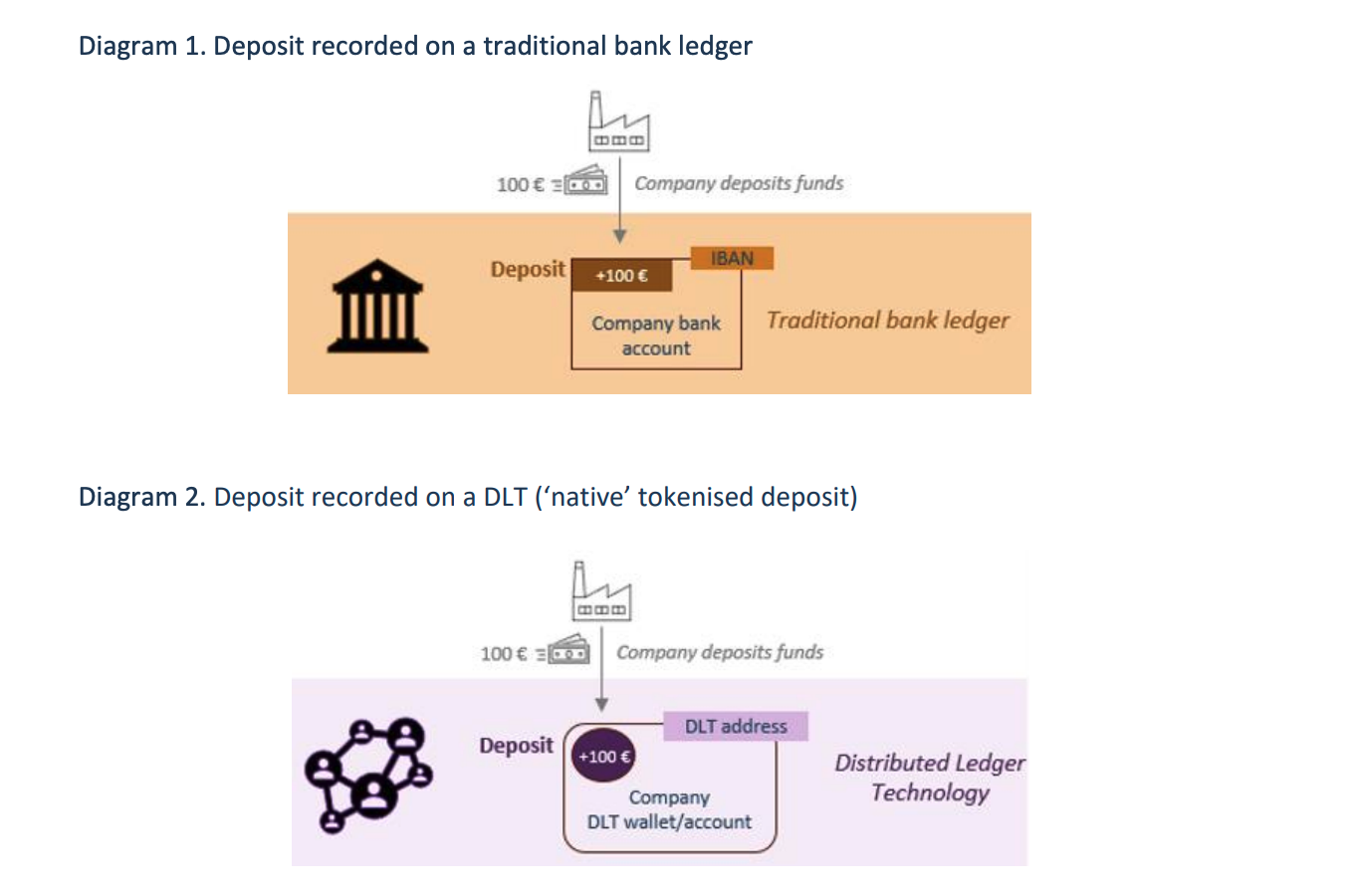

Tokenised deposits, which are bank-issued digital coins representing direct claims on commercial bank balances, have emerged as the structurally preferred form of institutional digital cash.

Be smart: The core advantage is instant, 24/7 settlement that cuts failed trades and liquidity costs. This capability eliminates the reliance on batched, time-constrained systems like CHIPS and dramatically reduces failed-trade risk and intraday borrowing costs through continuous cash sweeps and instant collateral movement. But with J.P. Morgan’s Kinexys leading with $1.5T in transactions, BNY Mellon’s strategy is necessarily centred on pursuing maximum interoperability through key partnerships (e.g., GS DAP, Fnality) and collaborative models like the Regulated Settlement Network (RSN).

By fitting within existing prudential and insurance frameworks, tokenised deposits bypass regulatory uncertainty and provide institutional-grade trust, unlike stablecoins, which the BIS deems structurally inadequate. With atomic Delivery-versus-Payment (DvP) on DLT (Distributed Ledger Technology), they eliminate principal risk in real time, shifting systemic risk management from reactive controls to instant, technology-enforced finality.

The challenge: Moving from pilots to deployment while ensuring interoperability and avoiding fragmentation.

Zooming in: This pilot builds on BNY Mellon’s DLT push, from tokenising MMF shares with Goldman’s GS DAP to broadcasting fund data like BlackRock’s BUIDL on Ethereum, creating a utility layer that connects off-chain records with on-chain automation.

Other initiatives: In June 2025, BNY and Goldman Sachs pilot tokenised MMFs, unlocking real-time liquidity and efficiency. [RELEASE]

Why now

Swift is building its tokenised ledger. NASDAQ is planning to offer tokenised equities. JP Morgan and HSBC launched tokenised deposits, while Citi is exploring them. The future of the financial system is on the tokenised ledger, and BNY has to act to get first-mover advantages.

Regulatory clarity: The U.S. and global regulators (OCC, FDIC, BIS) have affirmed that tokenised bank liabilities are deposits, reducing legal uncertainty and encouraging institutional adoption. DLT-based instruments gain credibility by aligning with existing banking frameworks, unlike non-bank crypto-assets.

Initiatives like Project Cedar and RLN show banks exploring wholesale DLT settlement, while SWIFT is also acting quickly to retain its dominance over cross-border payments through the correspondent banking model.

Poised for growth: Tokenised assets are poised for explosive growth ($10–18.9T by 2030), with cash and deposits driving early adoption. Tokenised deposits act as the foundational liquidity layer, enabling instant, programmable settlement for all other tokenised assets.

Key implications

1. The race is on and JP Morgan’s winning. Kinexys has moved $1.5T in tokenised transactions. BNY’s response? Bet on interoperability over proprietary rails. They’re partnering with Goldman’s DAP, Fnality, and the Regulated Settlement Network instead of building alone. Smart hedge if standards converge. Risky if winner-takes-most dynamics emerge.

2. $2.5T in daily volume is the prize. BNY processes that much every day through legacy rails. Moving even 10% to DLT saves hundreds of millions annually. This isn’t about innovation, it’s about margin protection.

3. Pilots ≠ production. DLT doesn’t integrate with 40-year-old core banking systems easily. BNY needs new custody infrastructure, 24/7 operations, unified data standards, all while keeping legacy systems running. Expect 3-5 years before meaningful volume. But the direction is irreversible: SWIFT’s working with 30+ banks on tokenised ledgers. The question isn’t if financial infrastructure moves on-chain, but who controls the rails.

Our Take

BNY Mellon’s pilot and participation in SWIFT’s blockchain-based shared ledger initiative represent a critical component of global payment infrastructure modernisation. By exploring tokenised deposits, SWIFT and participating banks aim to create a seamless, interoperable financial system with minimal fragmentation and enhanced liquidity.

Leveraging its client base, which spans over 90% of Fortune 100 companies and nearly all top 100 global banks, BNY Mellon positions the firm to drive broad adoption of tokenised deposit solutions. Combined with its pilot programs and strategic partnership with Goldman Sachs, it is positioning itself at the forefront of enterprise-grade, blockchain-enabled settlement infrastructure.

Market Signals of Today

- Brevan Howard Master Fund joins BlackRock in new on-chain tokenisation. Link

- Citi invests in BVNK, deepening US banks’ stablecoin adoption. Link

- Luxembourg’s sovereign wealth fund allocated 1% of its portfolio ($9M) to the BTC ETF. Link

- CruTrade tokenises fine wine on Avalanche, unlocking $9B market. Link

- DMCC and VARA partner to tokenise gold and diamonds securely. Link

- ARK Invest enters tokenised assets with $10M Securitize stake. Link

- Ondo Finance acquires Oasis Pro to expand regulated US tokenised markets. Link

That’s all for today’s CEO Briefing.

Best,

Marc & Team

🙌 Work with us: We create pioneering thought leadership that helps digital asset and technology companies lead the conversation, earn trust and win business.