Spoiler: Wall Street loves Bitcoin (fees)

Jamie Dimon once called Bitcoin a “pet rock” and a “fraud.” Now, his trading desk is wrapping it in a bow and selling it to the ultra-wealthy.

By launching an ”Auto Callable Accelerated Barrier Note“ linked to BlackRock’s iShares Bitcoin Trust (IBIT), they are structurally transforming it into a yield-bearing, volatility-dampened instrument for the country club set. [RELEASE]

Let’s unpack.

Download the PDF

Today’s Market Signals

NYT publishes puff piece on stablecoins. Link

CFTC announces pilot program for Bitcoin to be used as collateral in derivatives markets. Link

Berstein: “We are moving our 2026E Bitcoin price target to $150,000, with the cycle potentially peaking in 2027E at $200,000.” Link

BlackRock Files for Ethereum Staking ETF. Link

What happened

JPMorgan Chase issued structured notes linked to the performance of BlackRock’s iShares Bitcoin Trust (IBIT). This is explicitly engineered around the 2024–2028 Bitcoin halving cycle, combining an early‑call coupon profile in 2026 with leveraged upside and limited downside protection into 2028.

Deconstructing the JPMorgan IBIT Note:

JPMorgan has asked the SEC to approve a bond whose payout depends on the performance of IBIT.

This is a sophisticated structured product engineered around the 2024–2028 halving cycle.

- The Structure: Investors get 1.5x leveraged upside (uncapped) at maturity in December 2028, provided the price holds.

- The Safety Net: A 30% downside buffer. If IBIT falls less than 30%, principal is safe. If it falls 30.01%, losses are 1:1.

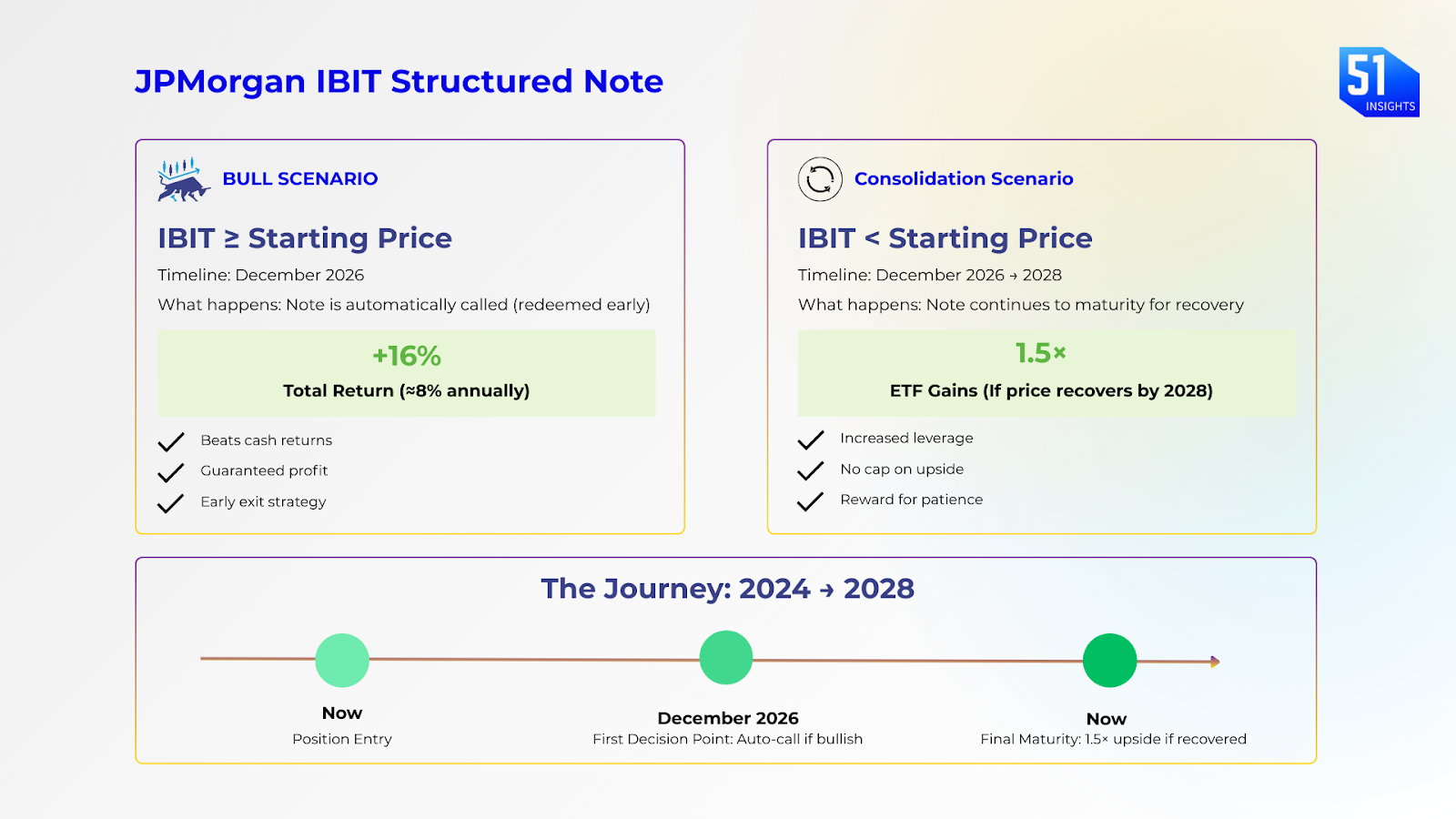

- The “Gotcha”: An auto-call feature in December 2026. If Bitcoin rallies early, JPM calls the note, paying a capped ~16% return (8% annualized) and keeping the rest of the upside for themselves.

Here’s how it works:

If IBIT is at or above the starting price in December 2026:

The note is automatically called. The investor gets their money back plus at least 16% total return. That’s about 8% a year. It beats cash, but it won’t match a strong Bitcoin rally. JPMorgan uses this feature to cap its exposure if Bitcoin runs early.

If IBIT is below the starting price in 2026:

The note continues to 2028. This matches the idea of a mid-cycle dip in 2026–2027.

At the 2028 maturity, if the price has recovered and is above the starting level, the investor gets 1.5× the gains of the ETF, with no cap. This is the reward for staying in through the down years.

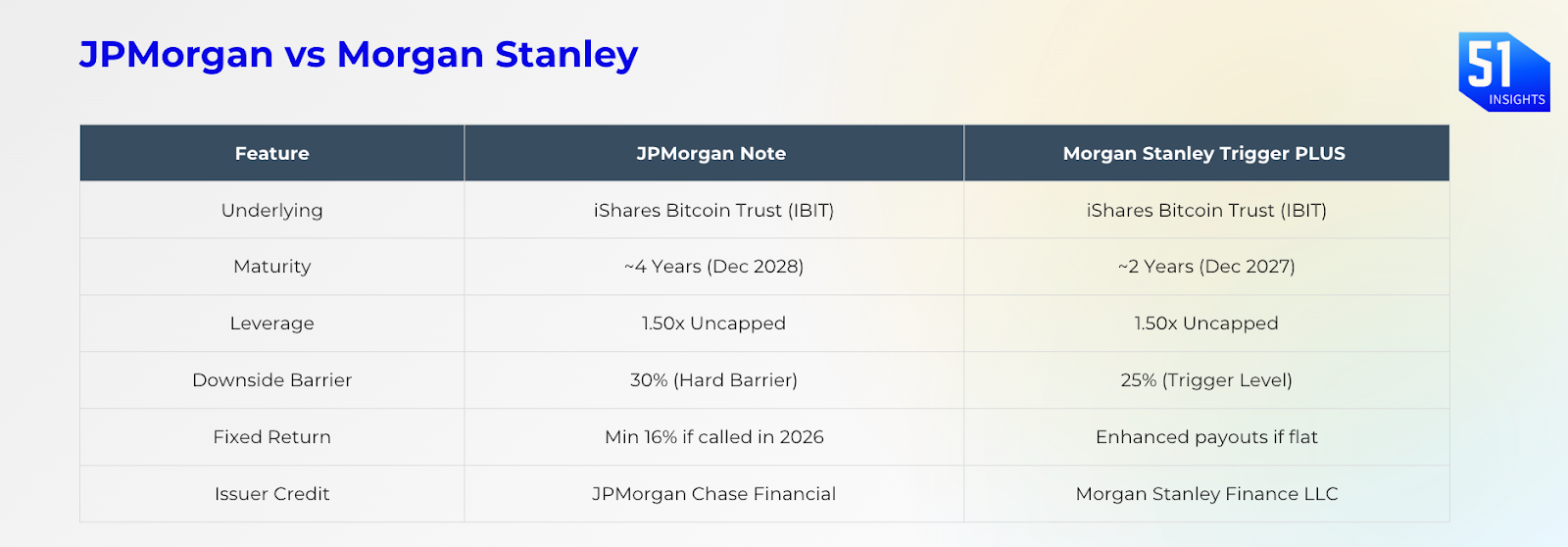

Morgan Stanley’s “Trigger PLUS”

In July 2025, Morgan Stanley has rolled out its own competing note, called the “Dual Directional Auto-Callable Trigger PLUS,” also tied to IBIT.

The core design is the same. Both products offer 1.5× uncapped upside, and both pay for that upside by making the investor take on deep downside risk.

Morgan Stanley sold $104M of these notes in a single month.

Why it matters

Securitising the Securitisation Wall Street is doing what it does best: layering fees on top of fees. First, BlackRock securitised Bitcoin into an ETF (IBIT). Now, JPMorgan is securitising the ETF into a structured note. IBIT alone holds on the order of 700k+ BTC, more than 3.5% of eventual BTC supply; JPM is now wrapping that liquidity into yield-bearing products for the massive wealth management complex. By putting Bitcoin exposure on the same “shelf” as S&P 500 autocallables, JPM effectively transforms a volatile commodity into a programmable financial instrument for private banking clients

Taming the God Candle: As these banks issue billions in structured notes, they must hedge their exposure.

What this means: Dealers are short volatility. They must sell when Bitcoin rises (to cap their payouts) and buy when it falls (to defend the buffer levels).

The result: These mechanical flows act as a dampener, pinning Bitcoin’s price in narrower ranges. We are moving from a market driven by “HODLer” ideology to one driven by dealer gamma hedging. Bitcoin is becoming institutional collateral. Expect the “God Candles” to get shorter, and the crashes to get shallower.

Third, and most importantly:

3. A strike against MicroStrategy: For the last cycle, MicroStrategy (MSTR) had a monopoly on institutional leverage. If you wanted juice, you paid Saylor a premium. JPMorgan just looked at that trade and said, “I can do that cheaper.” These notes are a direct competitive attack on the “MSTR Premium.” JPM is unbundling MSTR’s value proposition, leverage plus downside protection, and selling it directly to the end consumer for a fraction of the cost. Why pay 2.5x NAV for MicroStrategy when you can get 1.5x leverage on IBIT with a 30% downside buffer from your private banker? This is a part of a broader fight for control of institutional Bitcoin exposure.

Marc Baumann

Marc Baumann

Investor Alpha

JPMorgan isn’t just offering a product; they are orchestrating a regime change. By issuing IBIT-linked notes while simultaneously warning about MicroStrategy’s exclusion from the MSCI index, they are effectively “talking their book.” JPM analysts estimate $2.8B in forced selling if MSTR is booted from the index in January 2026—convenient timing for their own note issuance. This looks like a coordinated pincer movement: delegitimize the corporate proxy (MSTR) to clear the lane for the bank product (IBIT notes).

If MSCI excludes MicroStrategy on Jan 15, the premium collapse will accelerate. JPM’s and Morgan Stanley’s notes provide the “safe” leverage alternative that institutional allocators could rotate into. Watch the MSCI announcement like a hawk.

Take care,

Marc & team

Download the PDF

🙌 Work with us: We arm financial institutions and digital asset leaders with bespoke research, thought leadership to shape the most important conversations, scale trust, and win business.