The first crypto firm on Fedwire

Hey, it’s Marc,

For 110 years, direct access to Fedwire was the exclusive privilege of chartered commercial banks.

Today, a crypto exchange broke that streak. Kraken Financial just became the first digital asset bank in U.S. history to receive a Federal Reserve master account.

The implications run far deeper than faster deposits. [RELEASE]

Let’s unpack.

👉PRO: Download the PDF below

What happened

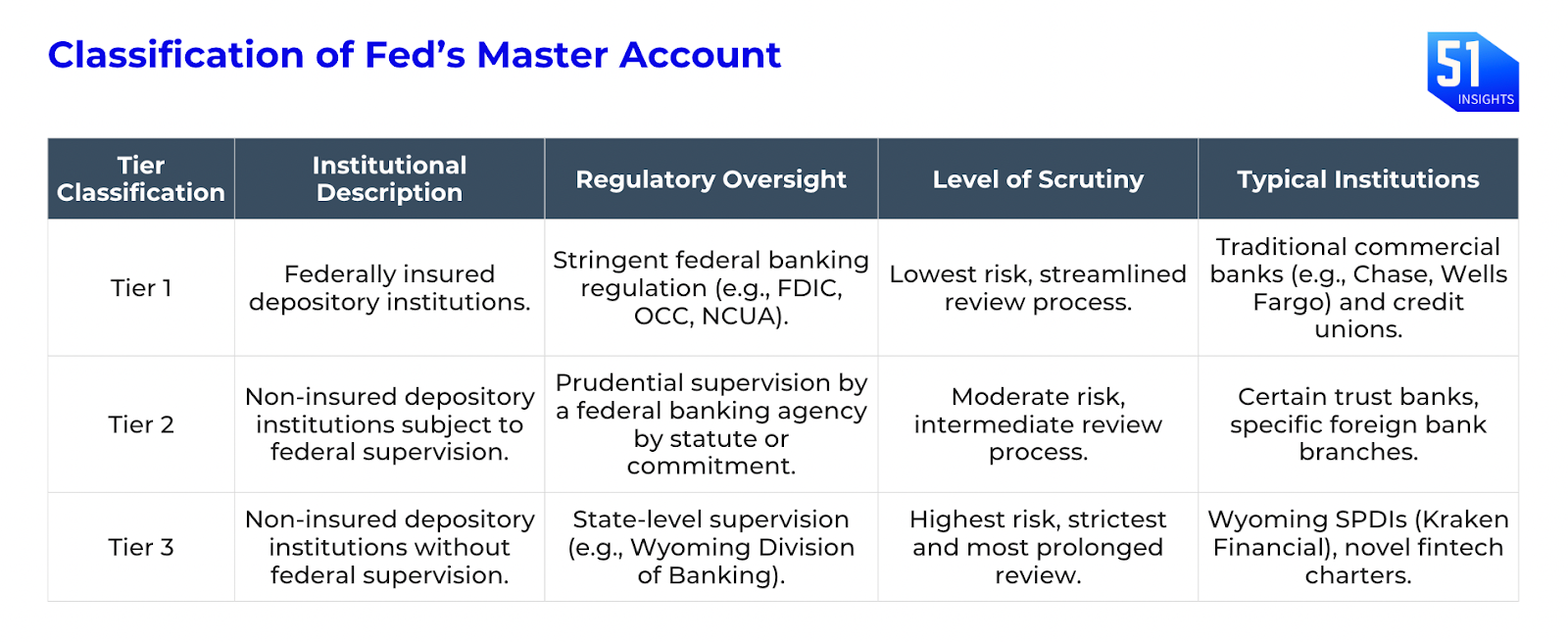

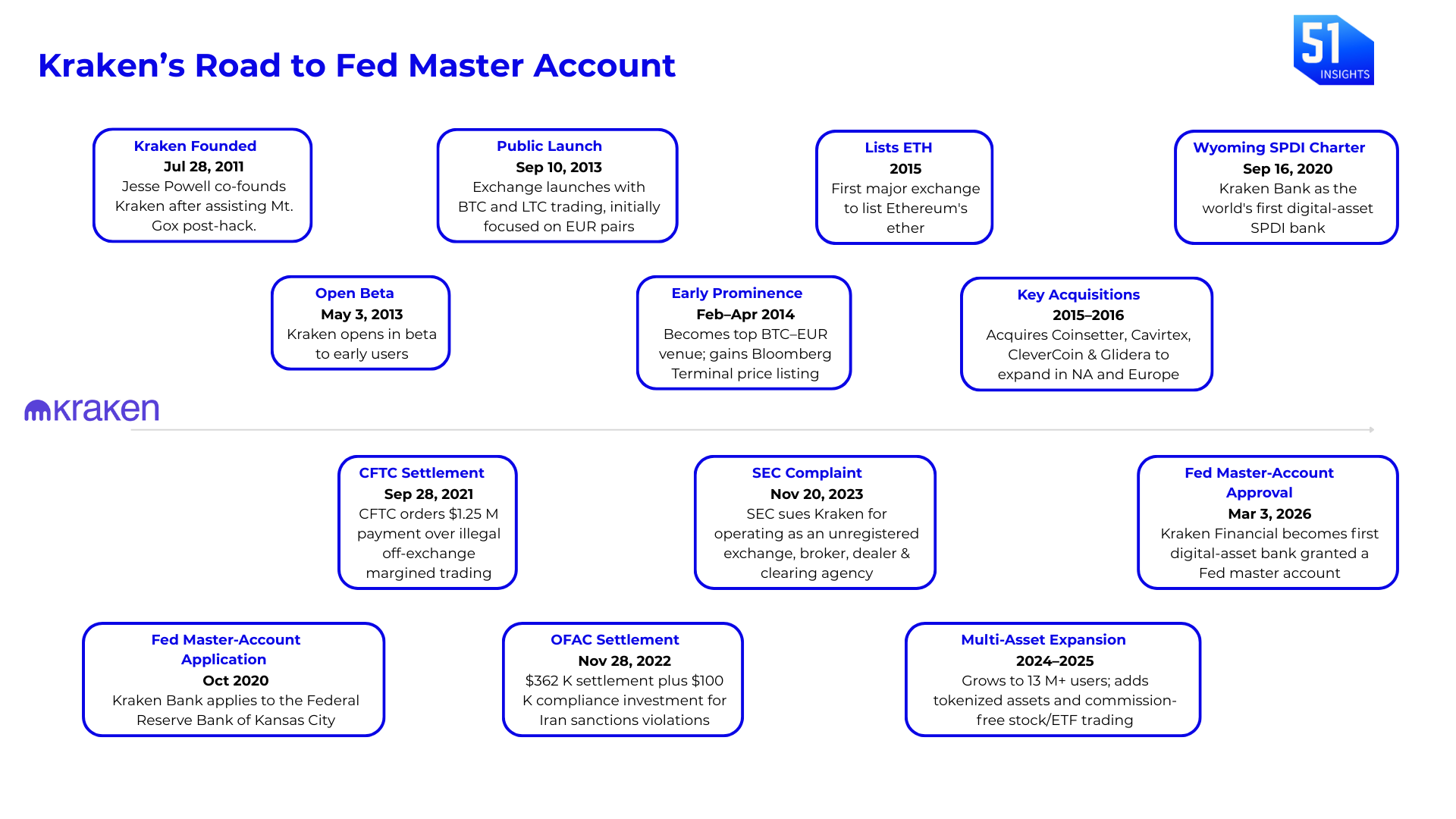

The Federal Reserve Bank of Kansas City granted Kraken Financial a Tier 3 skinny master account, giving it direct access to Fedwire, the interbank payment system that moves ~$4 trillion daily. Kraken applied in 2020. It took 5.5 years, two administrations, and what the company calls “sustained regulatory engagement” to get here. (RELEASE)

After a 5.5-year battle, Kraken Financial, operating under Wyoming’s Special Purpose Depository Institution (SPDI) framework, now has direct access to Fedwire.

In plain terms: Kraken can now settle U.S. dollars directly on the central bank’s balance sheet, with zero commercial bank intermediaries. When money moves through this account, settlement is final and guaranteed by the U.S. government.

The account comes with guardrails

- 100% reserve mandate: For every dollar a customer deposits, Kraken must keep exactly one dollar in reserve. Traditional banks only keep a fraction of deposits on hand and lend the rest out. Kraken can’t do that.

- No interest on reserves (IORB): Normally, banks earn interest just by parking money at the Fed overnight. Kraken gets none of that. It’s essentially a free safe, useful, but not profitable on its own.

- No discount window access: If a regular bank runs short on cash, it can borrow from the Fed as a lender of last resort. Kraken has no such safety net. If it runs into trouble, the Fed won’t bail it out.

Zooming in: Unlike a standard “full” master account, Kraken was granted a “limited-purpose” account for an initial one-year term.

- Phased rollout: Services will be introduced in stages, starting with support for institutional client activity.

- Restrictions: Kraken will not earn interest on reserves or have access to the Fed’s emergency lending “discount window”.

What they’re saying:

“This is what it looks like when crypto infrastructure matures into core financial infrastructure,”

– Arjun Sethi, co-CEO of Payward (Kraken’s parent)

Senator Cynthia Lummis called it “a watershed moment,” adding that the Fed has acknowledged a digital asset company can balance innovation with strong risk management. (CoinDesk)

By the numbers: Incepted in 2011, Kraken has a 13-year track record with over $2T in 2025 platform volume. It raised $800M with Citadel and Jane Street at the cap table in November 2025.

Zooming out: If it works, this could kick off a surge of Fed master account applications from other crypto firms. Anchorage and Ripple’s U.S. banking partner have also applied for master accounts.

This approval impacts custodians like BNY Mellon and State Street in a medium term with margin compression as platforms like Kraken offer the exact same sovereign-backed settlement but with native, frictionless crypto integration. However, for now, institutional inertia and existing regulatory mandates require SIFI custodians only.

Be smart: This comes right before Kraken’s IPO. A Fed master account is one of the most powerful things you can put in an S-1.

Why it matters

- No fragmentation tax: Today, institutional clients moving $50M into a crypto exchange route through three hops: their bank → Fedwire → Kraken’s correspondent bank → Kraken’s ledger. ACH deposits on Kraken currently carry a 7-day withdrawal hold. It creates a liability for exchanges. With Fedwire access, Kraken settles directly on the Fed’s balance sheet in real time. There is no hold with low counterparty risk and capital drag.

- The paradox: This approval contrasts sharply with the 10th Circuit Court’s affirmation of the Fed’s right to deny Custodia Bank. While the court ruled that the Fed is not legally required to grant accounts to every eligible institution (Custodia’s case), the Fed used that same discretionary power to voluntarily approve Kraken. However, it is not deregulation. While Custodia pursued a legal battle to force access, Kraken’s approval followed extensive coordination with both Wyoming and Federal regulators. It’s the Fed deciding exactly how crypto connects to the financial system, on its own terms, with a company it can keep a very close eye on.

- BNY Mellon and State Street got a competitor: BNY Mellon ($57.8T) and State Street ($51.7T) built their pitch to big institutional clients on one key advantage: direct access to the Fed’s settlement rails. That exclusivity just ended. Kraken now sits on the exact same foundation, but also offers round-the-clock crypto trading, lower fees, and the guarantee that every dollar on its platform is fully backed. The legacy giants have the brand and the relationships, but the one thing that made them irreplaceable for this specific use case is no longer theirs alone.

Investor Alpha

- Kraken (pre-IPO): Kraken raised $800M in November 2025, including a $200M strategic stake from Citadel Securities, at a $20B valuation. A Fed master account right before an IPO is one of the most powerful things you can put in an S-1. Watch for a pricing premium to Coinbase.

- Long COIN selectively: Coinbase still custodies the majority of spot Bitcoin ETF assets. But its fiat rails remain intermediated. If Coinbase doesn’t accelerate a competing charter application, the institutional infrastructure gap widens. 👉 Trade on Robinhood

- Long BLK: BlackRock’s BUIDL tokenized Treasury fund needs frictionless fiat on-ramps to scale. Kraken’s Fedwire access makes it a natural distribution partner. More tokenized Treasury adoption means more BUIDL AUM and fee revenue. 👉 Trade on Robinhood

Watch next: Anchorage and Ripple’s U.S. banking partner have also applied for master accounts. If Kraken’s pilot succeeds, expect a wave of applications from Circle, Paxos, and others with OCC charters.

Watchlist:

- Mar 1–2: Crypto Expo Europe (Bucharest)

- Mar 11: US CPI (Feb) release – critical for Fed rate cut expectations

- Mar 17–18: DC Blockchain Summit (Chamber of Digital Commerce)

- Mar 18: FOMC Interest Rate Decision & Summary of Economic Projections

- Apr 28–29: FOMC meeting. Second rate decision window

- Jul 1: MiCA universal deadline

- Q1-Q2 2026: SEC final decision on Nasdaq tokenized trading rule change (SR-NASDAQ-2025-072)

- H2 2026: DTCC tokenization pilot launch

That’s it for now.

Missed last week? Access all our CEO notes here.

Marc & Team