Stripe’s 1.5% tax on the old world

For 150 years, the architecture of cross-border commerce was a walled garden guarded by correspondent banks and toll-collecting card networks.

With the launch of Tempo, Stripe isn’t just offering a new payment button; it’s effectively turning global incumbents into back-end utilities for a superior settlement layer. 1.5% is the tax they’re charging the old world to transition to the new one.

Let’s unpack.

Download the PDF

Today’s Market signals

🚨 Get your brand in front of 100k+ decision makers in digital assets.

What happened

Stripe has launched Tempo, its payment blockchain on public testnet. Unlike SWIFT, which moves messages, Tempo moves value, and it’s doing so with a partner consortium that includes Deutsche Bank, UBS1, Visa, OpenAI, Shopify, and others. [NEWS]

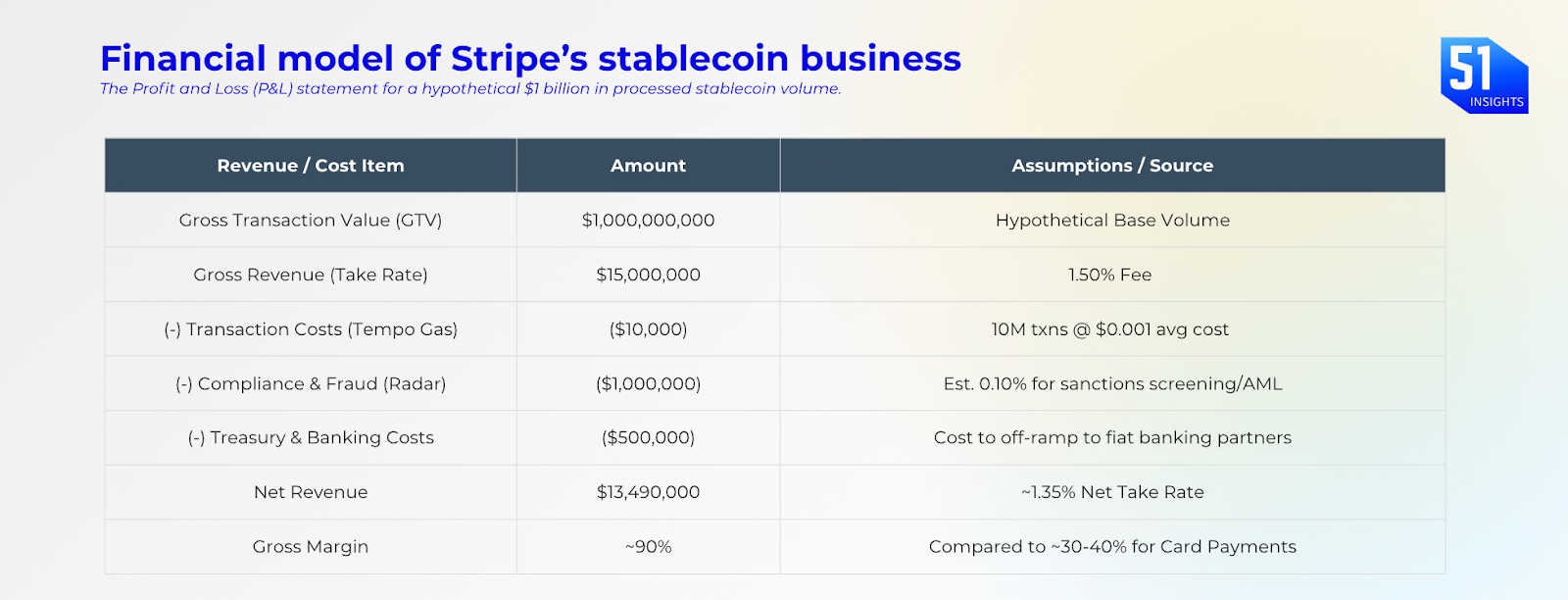

The most debated detail? Stripe is charging a 1.5% fee. While that looks pricier than pure-play crypto processors, it’s a masterclass in vertical integration. Stripe’s $1.1 billion acquisition of Bridge earlier this year allowed them to cut out the middlemen entirely. By owning the rails, that 1.5% fee, which is still a massive discount compared to the 3-5% charged by legacy international systems, becomes nearly 100% pure profit for Stripe.

Why Tempo: Public blockchains are unpredictable for payments, so Stripe needs a chain where fees and speed don’t spike when something unrelated gets busy. Tempo creates dedicated capacity specifically for payments, allowing businesses to pay fees in the same stablecoin they use, thereby removing operational friction. It’s fast, cheap, and compatible with existing Ethereum tools (yes, it’s EVM compatible). Initially, it’s tightly governed to meet bank-grade compliance, with openness introduced later.

Deconstructing the 1.5%: The merchant was previously paying $40.00 (4% of the total amount transferred) and waiting 3 days. Stripe offers the service for $15.00 (1.5%) with T+1 or instant availability. Stripe bundles currency conversion, bank payouts, and cash management into one step. It also covers recurring billing, taxes, and compliance, which would otherwise require multiple tools and extra costs.

Stripe looks pricier than BitPay or Coinbase Commerce on paper, but those also charge 1% plus hidden spreads and limited tooling. For businesses already on Stripe, the extra cost buys one dashboard, no extra engineering, and still undercuts PayPal’s 3–5% fees.

What matters is whether merchants save money overall, and Stripe’s model only works as long as it stays cheaper than the alternatives.

Why it matters

Collapsing the Settlement Stack: Traditional card networks solved for authorization speed (the “swipe”), but they never solved for settlement speed (the “cash”). Merchants typically wait 3-5 days for international funds. Tempo collapses this timeline to near-instant settlement, eliminating the need for corporate treasuries to hold idle “buffer cash” across global subsidiaries.

The Math of Idle Cash: In the legacy system, $100B in annual volume with a two-day settlement delay means roughly $550M is trapped in transit at any given time. In TradFi, this cash sits in correspondent banking networks earning interest for banks while merchants wait. By moving this volume onto Tempo, Stripe collapses the settlement window to near-instant.

But Stripe isn’t just speeding up the money; they are capturing the yield. Through Open Issuance2, Stripe and its partners (like BlackRock and Fidelity) manage the reserves backing these stablecoins.

The Revenue Engine: For every $1B in stablecoins issued on Tempo, there is $1B in “reserves” sitting in U.S. Treasuries.

The Yield Capture: At current rates (~4.5%), that $1B generates $45M in annual interest. Because Stripe owns the infrastructure (Bridge + Tempo), they—not a third-party bank—capture this “risk-free” profit. This is the Tether Playbook scaled for the enterprise: earning massive margins on the money that would otherwise be “idle” in the legacy pipes.

Infrastructure for the “Agentic” Economy: The real “alpha” isn’t in human-to-human payments; it’s in AI-to-AI transactions. Traditional credit cards cannot handle the micro-transactions (e.g., $0.005 for an API call) that AI agents require. Stripe’s integration with OpenAI suggests they are building the financial “OS” for machines that need to transact at the speed of light, not the speed of a banker’s hoursTime value of money: Beyond fees, Stripe makes money on the cash it briefly holds before paying merchants. At $100B in annual volume and a two-day delay, that’s about $550M sitting idle, earning roughly $22M a year at safe interest rates. Bridge expands this upside: if Stripe helps issue its own stablecoin, it can earn interest on the entire reserve backing it, following Tether’s playbook.

Our take

Stripe is no longer just a “checkout” company; It’s trying to become the system that money, software, and AI use to pay each other. As stablecoins move from a niche crypto tool to a $300B+ systemic infrastructure layer that will likely grow to trillions in the next 3-4 years, the “toll collectors” of the old world face a “Kodak moment”.

BUT: The L1 Graveyard Building a proprietary Layer 1 is notoriously difficult. Historically, corporate-led blockchains often fail to gain the necessary liquidity and developer adoption to move beyond “expensive plumbing”. Stripe’s challenge will be convincing the broader market that a chain tightly governed by a single corporate giant can offer the same censorship-resistance and resilience as open protocols. If Tempo remains a siloed “Stripe-only” environment, it risks becoming a high-tech cul-de-sac rather than a global highway.

Watchlist:

- Dec: USAT launch by Tether (expected)

- Dec: Clarity Act (H.R.3633) Senate vote (expected)

- Dec 31: Europe’s MiCA full enforcement (Austria, Germany, and Spain) ends

- Jan 1: Basel Committee crypto capital standards implementation in Hong Kong

- Jan’26: SEC Crypto Innovation Exemption

- Jan’26: Spot crypto ETF approvals for altcoin

- Q1’26: Kraken IPO

- Q1’26: Hong Kong Stablecoin licensing

- Q1’26: Singapore Stablecoin framework

That’s it for now.

Marc & Team

Download the PDF

UBS piloted UBS Digital Cash in 2024, a blockchain-based multi-currency payment solution designed to facilitate cross-border transactions for corporate clients. The core problem UBS is solving is Intraday Liquidity Management. In the current system, corporate treasury departments often have fragmented liquidity trapped in various subsidiaries and currencies across different time zones. Moving funds from a subsidiary in Hong Kong to a parent in Zurich via SWIFT can take days (T+2), forcing the company to hold idle “buffer” cash in both locations. UBS Digital Cash allows for 24/7, near-instant settlement. By tokenising these deposits, UBS turns “slow money” into “fast money”. ↩

What is Open Issuance? Think of Open Issuance as “Software for Minting Money.” Through Stripe’s API, a company—say, Shopify—can instantly “mint” (create) digital dollars (stablecoins) to pay a supplier in Argentina. ↩