Ripple's $40B valuation, better than Circle?

Ripple raised $𝟱𝟬𝟬𝗠 𝗮𝘁 𝗮 $𝟰𝟬𝗕 𝘃𝗮𝗹𝘂𝗮𝘁𝗶𝗼𝗻, backed by Citadel and Fortress. [NEWS]

Other backers? Brevan Howard, Marshall Wace, Pantera Capital, and Galaxy. Ripple might have leapfrogged Circle and Tether.io as the vertically integrated and globally compliant financial infrastructure provider.

Unlike them, Ripple doesn’t just issue money. It owns the pipes.

Let’s unpack.

(PRO readers: PDF below)

What happened

In just over two years, Ripple has developed a comprehensive five-pillar institutional stack, transitioning from its initial use case of cross-border payments:

Custody: Acquired firm Metaco ($250M in 2023); 75 regulatory licenses globally

Payments & Stablecoins: Leveraging Rail and RLUSD (in Dec 2024)

$95B processed through Ripple Payments in 2025; RLUSD hit $1B market cap

Treasury management: Integrating GTreasury (acquired in Oct 2025 for $1B) to provide a direct gateway into corporate liquidity flows

Prime Brokerage: Operating Ripple Prime (aka Hidden Road; acquired in Apr 2025 for $1.25B); handles $3T annually, moves $10B/day, 50M daily transactions

XRP-ledger: A decentralised, open-source blockchain

The thesis: own the full stack that moves institutional money, not just the money itself.

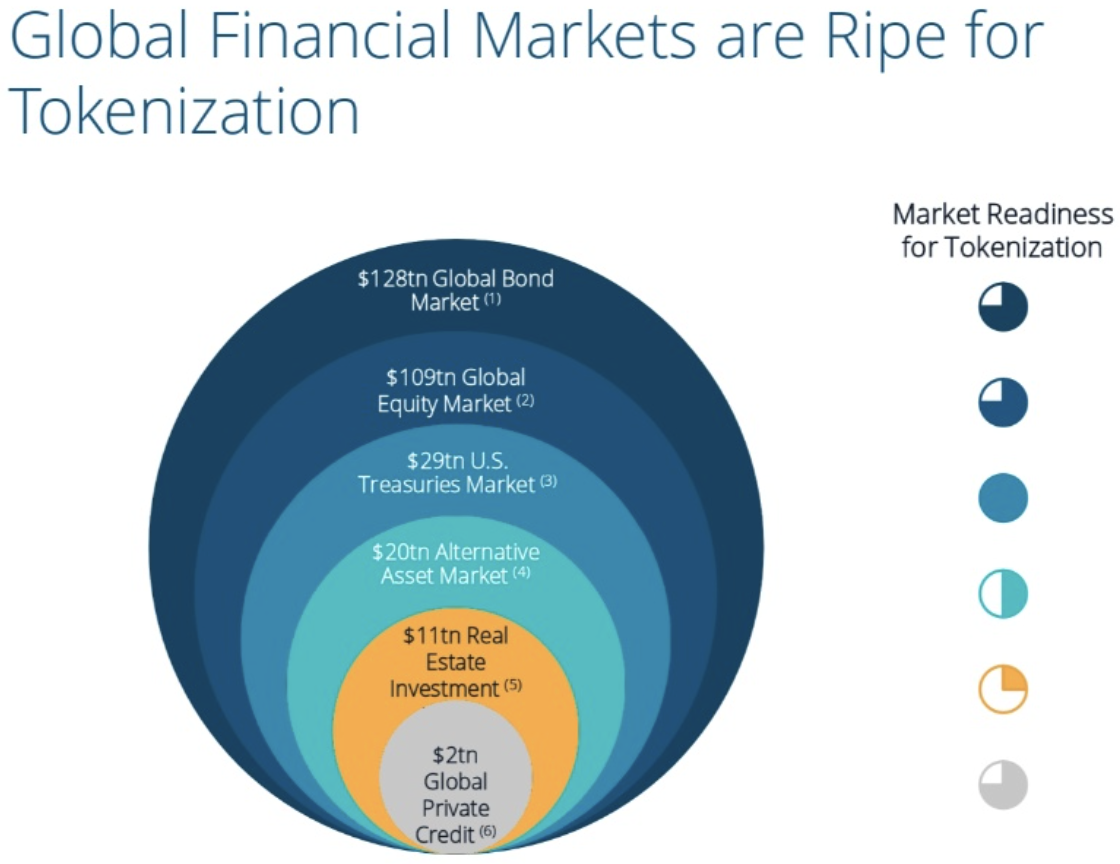

The catalyst: Tokenisation. Ripple is positioning its consolidated infrastructure as the critical liquidity and workflow bridge for $19T RWA tokenisation market.

The infrastructure play: Ripple Prime clears $3T annually across digital assets, FX, and fixed income for 300+ institutional clients. It’s the core utility layer that makes RLUSD and RWA collateral actually usable for hedge funds and asset managers.

The mechanism: XRP acts as a bridge currency for On-Demand Liquidity (ODL) outside the U.S., enabling cross-border settlements without pre-funded accounts. ODL volumes are up 41% quarter-over-quarter, topping $2.7B monthly. In the U.S., Ripple long relied on USDT due to regulatory uncertainty. That’s changing.

The institutional validation: BlackRock, Fidelity, and VanEck launched XRP ETFs holding $1.9B in assets within one month. XRP corporate treasuries hit $2B in announced commitments, led by Evernorth. Ripple is piloting stablecoin settlements with Mastercard, WebBank, and Gemini using RLUSD on XRP Ledger.

🙌 Work with us: We arm financial institutions and digital asset leaders with bespoke research, thought leadership to shape the most important conversations, scale trust, and win business.

Why it matters

- Capital migration has barely started. Stablecoins hit $300B+ in market cap but remain a rounding error versus global assets (equity: $127T; fixed income: $145T). They mainly serve crypto trading and niche cross-border payments. Real-world asset tokenization is early-stage, but as adoption widens, it opens trillion-dollar opportunities for infrastructure players to tokenize mainstream deposits and cash.

- This is an infrastructure thesis, not a token bet. Citadel Securities and Fortress Investment Group, pillars of global market structure, not venture capital, led the round, underscoring the focus on liquidity, compliance, and institutional-grade rails. The irony: Ripple still holds 34.76B XRP, worth over $80B, nearly double its $40B valuation. By discounting those holdings and valuing only the regulated payments and brokerage business, investors are clearly betting on stable, recurring institutional revenues rather than speculative token wealth.

The valuation makes no sense, until it does. Circle’s USDC is 75x larger than RLUSD ($73B vs $1B), yet Ripple is valued at 1.7x Circle’s valuation ($23.72B). Investors aren’t buying token metrics. They’re buying the only vertically integrated stack that connects corporate treasuries (GTreasury), institutional prime brokerage ($3T clearing), and stablecoin settlement in one workflow.

Our take

Ripple’s $40B valuation hinges on a single question: Do institutions adopt crypto through vertically integrated, compliance-first infrastructure or through open, liquidity-maximizing protocols?

Citadel and Fortress are betting on the former. They’re paying a 70% premium to Circle not for stablecoin dominance but for ownership of the full stack—treasury software, prime brokerage, custody, settlement rails—that could funnel trillions from corporate balance sheets into tokenized assets.

The challenge: Ripple owns the gateways but not yet the flow. RLUSD’s $1B market cap and $382M in tokenised assets on XRPL are small compared to USDC’s $70B and EVM’s $35B RWA base. Ripple needs to 10x RLUSD adoption (to $10B+) and grow XRPL’s tokenized assets from $382M to at least $3-5B to justify this valuation.

The bull case: Compliance and vertical integration eventually matter more than liquidity depth, and Ripple captures the majority of institutional flows.

The bear case: Liquidity begets liquidity and Ripple becomes expensive plumbing for a parallel financial system that never scales.

Citadel and Fortress just placed a $500M bet on the bull case. The market will render its verdict by mid-2026.

Today’s Market Signals

- CFTC chair confirms push to launch leveraged spot crypto trading. Link

- BoE proposes £20,000 on retail stablecoin holdings. Link

Take care,

Marc & team

Download the PD

F