Mastercard’s $2B play to own digital money’s backend

Mastercard is reportedly in late-stage talks to acquire Zerohash for between $1.5B and $2B, a company that raised $104M from Interactive Brokers, Morgan Stanley, and Apollo at a $1B in September and just became one of the first firms authorised under Europe’s new MiCAR framework. [NEWS]

This is one of Mastercard’s largest investments ever in the crypto space.

The seven-year-old startup not only powers 5M+ users across 190 countries but also serves blue-chip clients like Stripe, Franklin Templeton, Morgan Stanley’s E-Trade and BlackRock’s BUIDL fund. Let’s unpack.

👉Download the PDF

What’s happening?

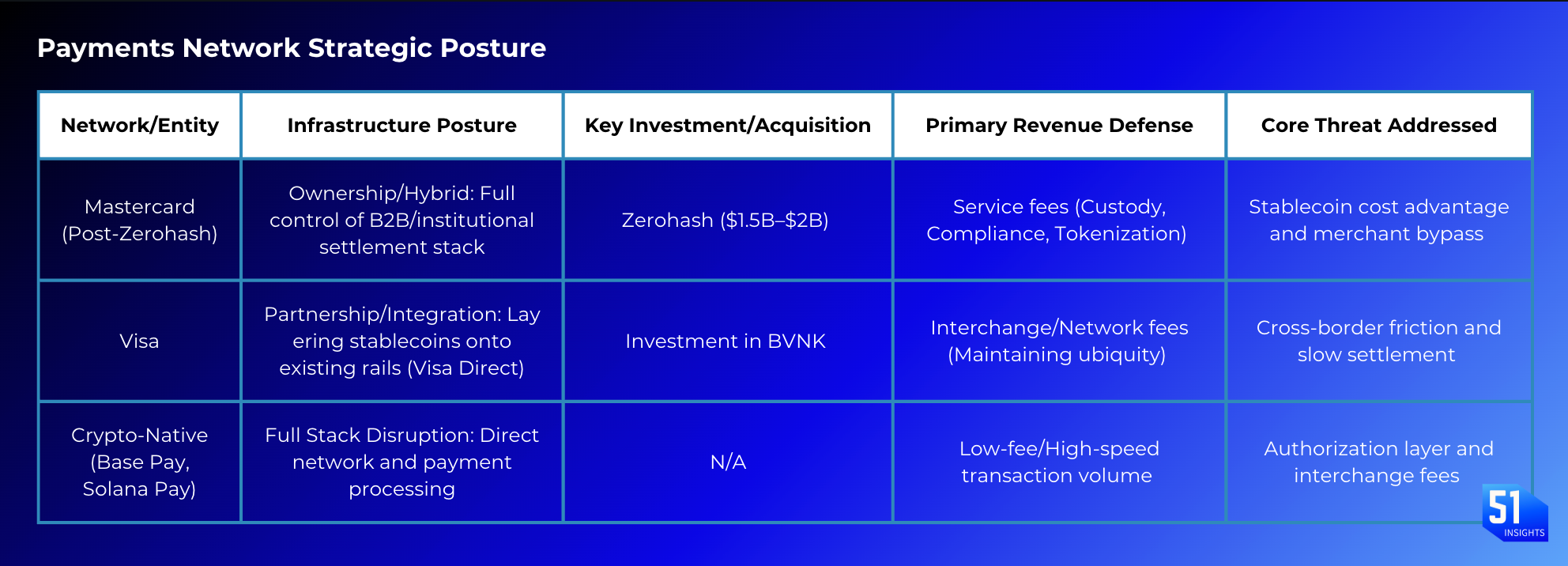

Mastercard is making its biggest move in crypto by acquiring Zerohash, a turnkey, regulated infrastructure stack that lets banks, brokers, and fintechs plug into digital assets without touching the backend.

Zooming in: Mastercard has long talked about “crypto-ready” payments, but most of its progress has been through partnerships and pilots. Owning infrastructure like Zerohash would give Mastercard direct control over the APIs that convert dollars into stablecoins, settle transactions on-chain, and manage custody. Zerohash key technological services include: custody and settlement, on/off ramps, tokenisation APIs, and compliance layer.

Zerohash isn’t a “payments” company. It’s basically a crypto’s back office. They enable

- fiat-to-crypto conversions for major banks,

- stablecoin trading infrastructure for platforms,

- API-level crypto integration for financial institutions, and tokenization infrastructure.

This means: Mastercard is not bidding for its revenue, but for a plug-and-play infrastructure that buys time and regulatory access. It will an add-on to Mastercard’s existing Multi-Token Network (MTN)™.

Zooming out: As fees from traditional card payments shrink, Mastercard is betting its future on selling the compliant “pipes” and custody services that make stablecoin and tokenized money flow safely through the global system.

🙌 Work with us: We arm financial institutions and digital asset leaders with bespoke research, thought leadership to shape the most important conversations, scale trust, and win business.

Why it matters

- Mastercard’s attempt to defend its moat: Mastercard’s entire business model rests on controlling the “authorization” and “settlement” layers of global payments. In today’s system, those steps are intentionally separate: authorization happens instantly, but settlement drags on for days, allowing Mastercard to sit in the middle and monetize the flow. Stablecoins collapse that gap. The move would let Mastercard internalize the new on-chain settlement layer, preserving its role as the trusted, compliant intermediary.

- Immediate production volume and desirable list of partners: Zerohash powers some of the biggest names, from Morgan Stanley’s E-Trade, which will soon let users trade bitcoin, ether, and solana, to Walmart-backed OnePay, which plans to offer crypto access to retail users later this year.

- The MiCA license as a strategic premium: In the United States, Zerohash holds the stringent New York BitLicense and U.S. Money Transmitter licenses. In Nov’25, it got approval to offer regulated crypto and stablecoin services across all 30 countries in the EEA by the Dutch AFM. By buying a MiCA-licensed firm, Mastercard is effectively purchasing regulatory trust in Europe, positioning itself as the go-to private partner to power future euro-backed stablecoins and even the Digital Euro.

Our take

This is about owning the infrastructure layer between traditional money and digital money. With a full MiCA license, operational APIs, and active production clients, this move accelerates Mastercard’s shift from consumer-facing rails to regulated, embedded infrastructure for banks, brokers, and fintechs.

Critically, the ECB has signaled that private intermediaries will manage Digital Euro distribution. And with this acquisition, Mastercard becomes a top contender to own that role. Its scale and existing compliance footprint make it one of the most credible bridges for institutions entering regulated digital assets in both the U.S. and Europe.

But the real transformation is economic: this moves Mastercard away from low-margin per-swipe fees toward high-margin B2B services: custody, KYC, tokenization, and on-chain settlement. To fully realize that upside, Mastercard must now deeply integrate its Multi-Token Network (MTN) with Zerohash’s live infrastructure, compressing time-to-market for stablecoin and CBDC services across its global partner base.

Marc Baumann

Marc Baumann Marc Baumann

Marc Baumann

Today’s Market Signals

- Coinbase to acquire BVNK. Link

- ECB will test Digital Euro in 2027. Link

- UBS completes the first tokenisation fund transaction. Link

- HashKey Group partners with Kraken for institutional tokenisation. Link

Take care,

Marc & team