JP Morgan x DBS: The $1.5 Trillion On-Chain Bridge

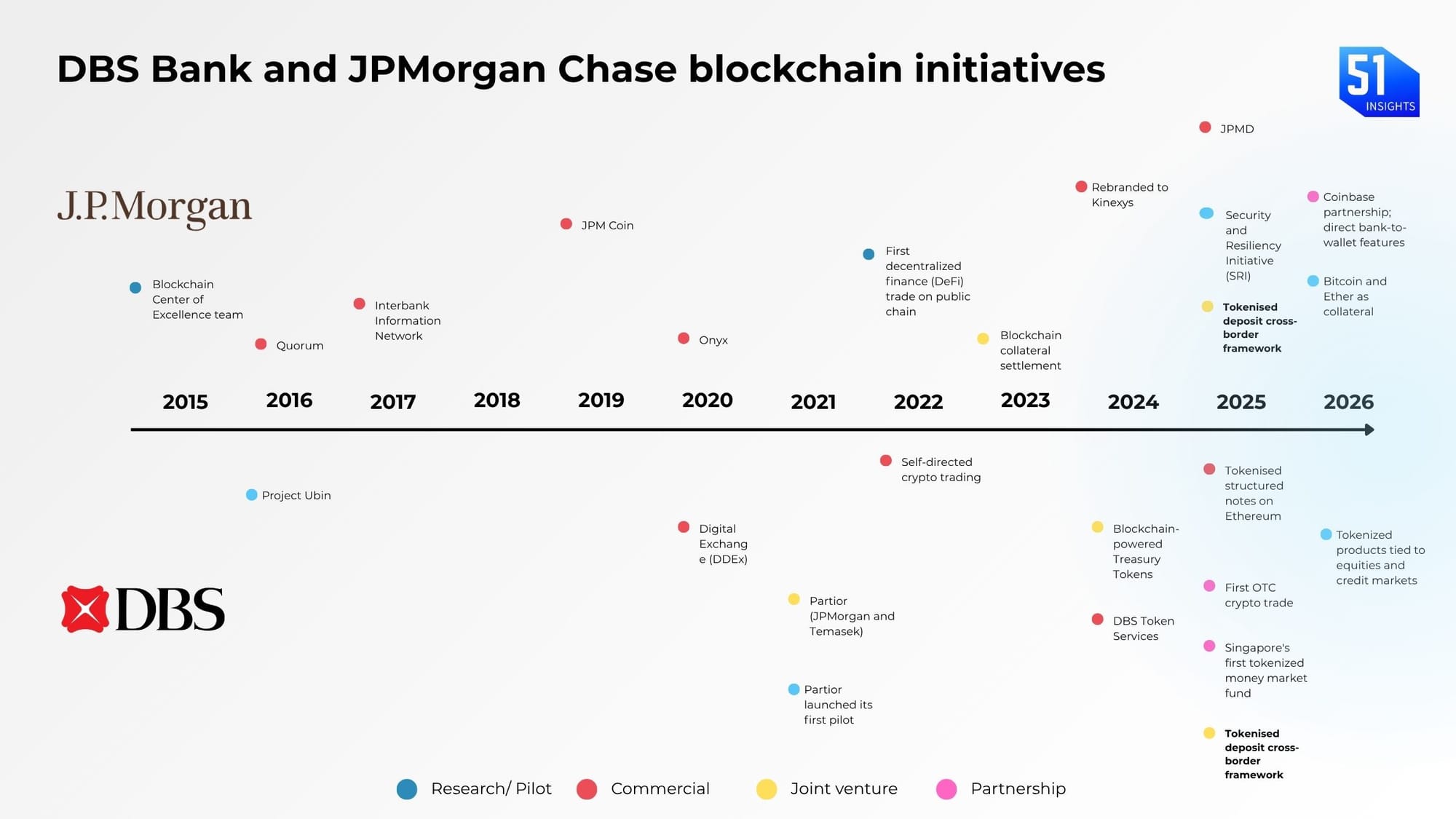

DBS and J.P. Morgan’s Kinexys are building a cross-bank framework to let tokenised deposits move seamlessly between their blockchain systems: DBS Token Services and Kinexys Digital Payments. [RELEASE]

Kinexys processes over $2B in daily payments and $1.5T cumulatively, while DBS Token Services has surpassed $1B in tokenized trading volume in 2025. This transitions tokenised commercial bank money from isolated, proprietary “walled gardens” into a unified, cross-issuer, cross-chain infrastructure.

And they’re doing it across public and permissioned chains at the same time.

Yes, public chains. That’s a huge deal. Let’s unpack.

👉Download the PDF

What happened

By linking DBS’s Token Services with Deposit Tokens (JPMD) on Base, Southeast Asia’s and the U.S.’s largest banks are establishing the blueprint for the future of global transaction banking.

Both banks have operated as closed systems, limiting transactions to their own clients. The new DBS–Kinexys framework changes that, building a regulated bridge that allows tokenised deposits to move securely between banks – and between open blockchains.

This can unlock:

- 24/7 cross-border payments between bank clients

- Real-time, FX-free B2B settlement

- Interoperability between JPMorgan’s JPMD (on Base) and DBS Token Services

- No need for USDC, USDT, or CBDCs

This means: A J.P. Morgan client in New York could pay a DBS client in Singapore in seconds, using JPM Deposit Tokens (JPMD) on Base, while the recipient redeems it as fiat or tokenised deposits on DBS’s side.

Zooming in: While J.P. Morgan has led the space, DBS is moving swiftly to capture the Asia-Pacific B2B payments corridor, projected to reach $1.4T by 2033.

By the data: Nearly one-third of central banks now have commercial institutions piloting tokenised deposits. An advanced tokenised payment infrastructure will reduce the cost of corporate cross-border transactions by a minimum of 12.5%.

The infrastructure play: DBS Token Services operates on a permissioned blockchain built for institutional control, while J.P. Morgan’s Deposit Token (JPMD) is being tested on Base, a public Layer 2. Running on Base gives JPMD access to 24/7 liquidity and network transparency while maintaining Ethereum’s security and settlement finality. Together, they’re addressing institutional settlement through a dual model: private ledgers for compliance, connected to public networks for reach and liquidity.

To connect these environments, the banks will likely use a secure, oracle-based messaging protocol like Chainlink’s CCIP, which J.P. Morgan has already tested for settling tokenised U.S. Treasuries against USD deposits.

At its core, the framework enables instant, atomic settlement; both sides of a transaction move together or not at all, removing counterparty and settlement risk and enabling advanced transaction types such as DvP and PvP.

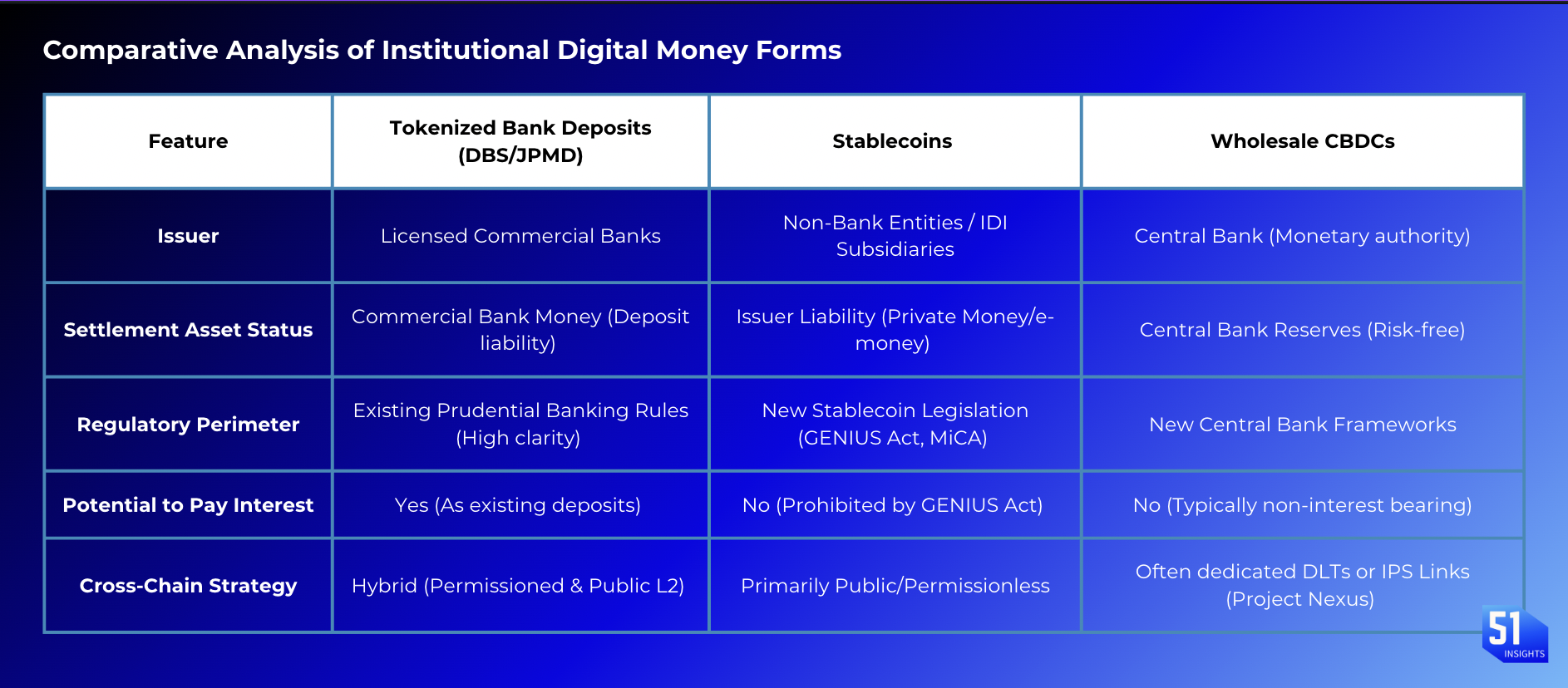

Zooming out: Digital money is consolidating around three models: tokenised deposits, stablecoins, and Central Bank Digital Currencies (CBDCs). Tokenised bank deposits are emerging as the de facto settlement asset for institutions: trusted, regulated, and yield-bearing, unlike most stablecoins.

Singapore’s MAS has led the way through initiatives like Project Guardian, creating a supportive environment for DBS to pilot the interbank standard.

In the U.S., focus remains on the GENIUS Act for stablecoins, while the Conference of State Bank Supervisors has called on federal regulators to provide similar clarity for tokenised deposits. Together, these efforts reflect rising pressure to enable bank-led innovation within clear guardrails.

Marc Baumann

Marc Baumann

🙌 Work with us: We arm financial institutions and digital asset leaders with bespoke research, thought leadership to shape the most important conversations, scale trust, and win business.

Why it matters

- Singleness of money: The framework preserves the value of one dollar on one bank’s chain to another, while achieving instant, 24/7/365 settlement across borders, directly challenging the latency and capital inefficiency of the traditional correspondent banking model. It positions tokenised deposits as the inevitable foundational layer for institutional liquidity management and the settlement of tokenised Real-World Assets (RWAs).

- Challenges, both SWIFT and stablecoins: Tokenised deposit not only replaces SWIFT and T+2 B2B rails, but also emerges as the frontrunner of regulated finance. Issued by licensed banks and backed by existing deposit laws, they carry the same legal and regulatory protections as traditional bank money. Unlike stablecoins, tokenised deposits can earn interest and integrate directly with core banking systems, making them a more practical form of on-chain cash for corporates and institutional treasuries.

- RWA’s catalyst: The growth of real-world asset (RWA) tokenisation depends on having regulated, instant, and reliable on-chain cash for settlement. Tokenised deposits fill this role, enabling atomic settlement for securities and other assets. This cross-border atomic settlement capability will power new institutional products, such as Singapore funds instantly buying U.S. Treasuries, creating a flywheel where better settlement drives RWA growth, and RWA growth amplifies demand for interoperable tokenised cash.

Our take

These banks have already piloted cross-chain settlement, but their stability will depend more on the governance, accuracy, and resilience of the FX oracle than on the DLT layer. The real challenge lies in cross-currency atomicity, linking USD-denominated JPMD with SGD within DBS Token Services in real-time. Achieving this requires live FX pricing from a trusted liquidity provider through a secure oracle, a model explored under MAS Project Guardian.

The framework will also make more sense if it prevents a two-bank duopoly. The technical and governance standards, smart contracts, messaging rules, and interoperability protocols must be open and neutral. BIS and other regulators are more likely to enforce common standards for such global tokenised money movement. Whereas, financial institutions will accelerate investment into infrastructure that supports hybrid DLT environments.

Today’s Market Signals

- Bank of England announces proposal on stablecoin regulation. Link

- Standard Chartered issues Singapore’s first stablecoin credit card. Link

- Franklin Templeton and DBS launch Singapore’s first tokenised MMF. Link

Take care,

Marc & team