Hong Kong built the rails. Will the trains arrive?

Hey, it’s Marc & 51 team,

Hong Kong’s crypto market doesn’t look like a casino anymore. It looks like a bank.

Over the past two years, the SAR methodically dismantled the unregulated exchange model, pushed out crypto-native giants like OKX and Bybit, and rebuilt itself as an institutional settlement hub. By Q1 2026, it has completed the infrastructure: VATP licenses, stablecoin regulations, Project Ensemble.

But here’s the problem: it built a $20M per-license fortress for a market that still feels empty.

The real question is whether mainland China will actually send capital through the door.

Let’s unpack.

👉PRO: Download the PDF

What happened

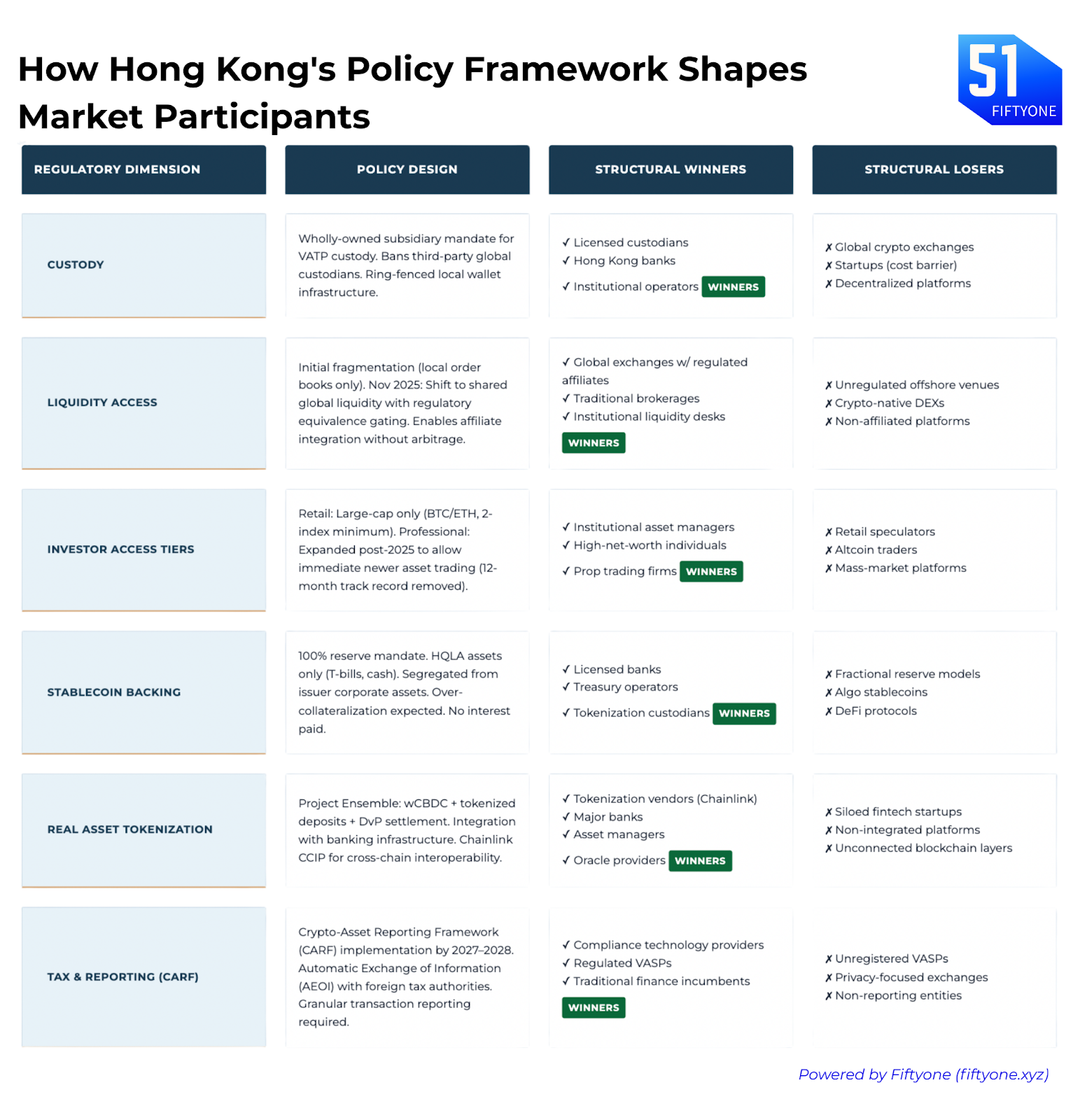

Hong Kong’s regulatory architecture bifurcated into two pillars between 2023 and early 2026.

- The Virtual Asset Trading Platform (VATP) regime, live since June 2023, imposes “bank-grade” custody and segregation requirements on all exchanges.

- The Stablecoin Ordinance (effective August 2025) treats stablecoin issuers as narrow banks, 100% reserve backing, zero interest payments, mandatory incorporation in Hong Kong.

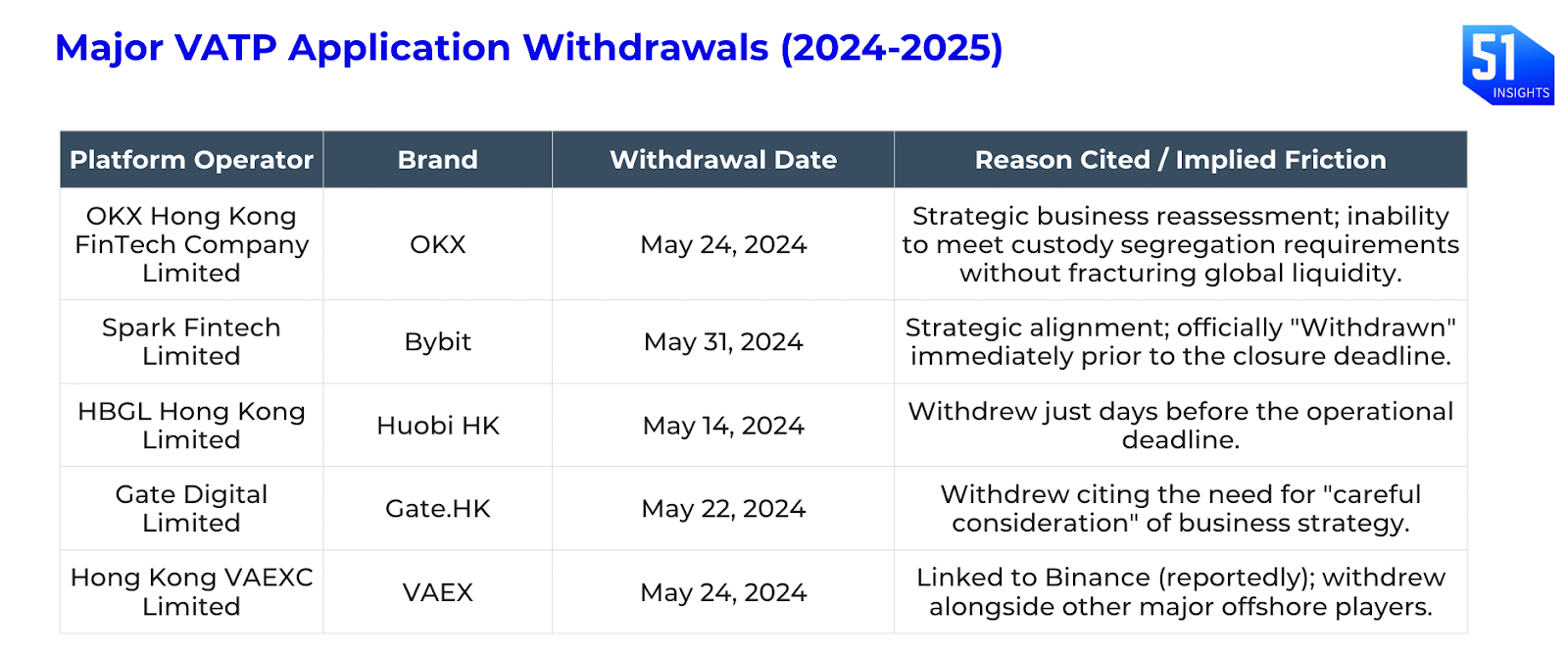

The real exodus came in 2024-2025. OKX, Bybit, Huobi, and Gate all withdrew their applications, citing compliance costs exceeding $20M USD and custody rules that shattered their global liquidity model. They couldn’t run a local Hong Kong entity that tapped global order books; the SFC demanded ring-fenced, wholly-owned custodial subsidiaries. Thin local order books meant worse pricing than offshore venues. So they left.

But regulators didn’t retreat. In November 2025, the SFC issued a critical circular: licensed platforms could now integrate with “globally regulated affiliates” to access shared liquidity pools.

By January 2026:

- Project Ensemble (the HKMA’s wholesale central bank digital currency sandbox) moved into its “EnsembleTX” pilot phase, enabling atomic settlement of tokenized bonds and deposits across a consortium of seven major banks: HSBC, Standard Chartered, Bank of China (Hong Kong), and others. Early use cases are live: HSBC settled digital bonds in minutes instead of days; Standard Chartered is tokenizing shipping bills of lading. [RELEASE]

- Under Hong Kong law, the HKMA is enforcing Basel crypto rules through its Supervisory Policy Manual and Exposure Limits Code from 1 January 2026, forcing banks to hold more capital and cap crypto exposure.

What is coming: Hong Kong will regulate virtual-asset dealers and custodians like traditional securities firms, with full AML, capital, and asset-safeguarding rules, and legislation expected in 2026.

Why it matters

- The institutional capture is complete. Hong Kong’s crypto market is no longer a retail playground. It’s a plumbing layer for the banking system. Harvest Global Investments, Bosera Asset Management, and China Asset Management (Hong Kong), all state-linked Mainland entities, now dominate the spot Bitcoin and Ethereum ETF market. Their participation signals tacit Beijing approval. It’s the infrastructure play for the Southbound Connect expansion: when mainland citizens eventually gain access to Hong Kong crypto ETFs through the Connect program (still blocked today), the pipes will already be in place.

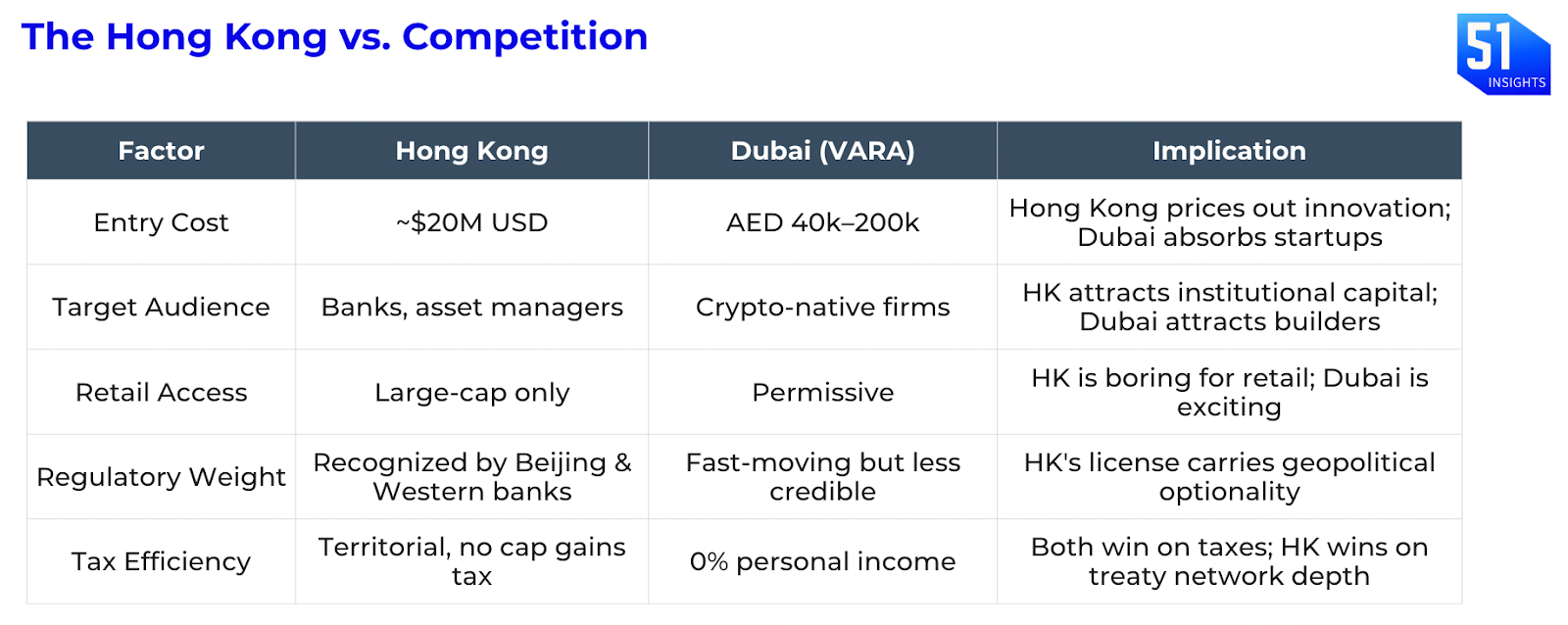

- The cost barrier is a feature, not a bug. Excluding crypto-native startups and forcing only institutional players to stay was deliberate. The SFC wanted “Old Money,” sovereign wealth funds, pension allocators, banks, not “New Money” speculators. This positions Hong Kong as the institutional counterweight to Dubai’s crypto-native permissiveness. Dubai wins on startup velocity; Hong Kong wins on regulatory credibility with mainland China and Western banking partners. That’s a real tradeoff, but only if capital actually shows up.

- Tokenization is the endgame. Project Ensemble is about settlement infrastructure. If Hong Kong can capture 1% of global mutual fund and ETF AUM by 2030 (currently $60T globally), that’s $600B in tokenized assets needing settlement rails. With on-chain deposits and on-chain bonds integrated on the same HKMA-supervised network, the city becomes the clearing hub for institutional tokenization across Asia. But this only works if Western banks and Mainland institutions actually issue and trade tokenized treasuries, corporate bonds, and structured products through Hong Kong rails. The rails are built. The traffic is not.

- Liquidity fragmentation is the real vulnerability. Despite the November 2025 fix, trading volumes in Hong Kong crypto spot markets remain microscopic compared to offshore venues or US ETFs. US Bitcoin ETFs hit $52B in AUM in weeks; Hong Kong ETFs saw $11M on day one. The city is now over-regulated relative to its actual trading volume. You can have perfect rules on an empty dance floor. The question is whether the Southbound Connect expansion (pending, but politically complex) will actually unlock the $200B+ in daily Southbound buying power that flows into Hong Kong stocks. If it does, Hong Kong’s market infrastructure becomes the natural on-ramp for Mainland capital into digital assets. If it doesn’t, Hong Kong remains a well-built fortress with no siege to defend.

Investor Alpha

Hong Kong’s regulatory framework is not competing for volume, it’s competing for institutional legitimacy. The city is betting that when mainland China opens the capital account to digital assets (via expanded Southbound Connect or a parallel mechanism), Hong Kong’s expensive, credible infrastructure will be the only trusted on-ramp.

Monitor:

- HSBC (HSBC / 0005.HK): Institutional deposit tokenization and bond settlement through Project Ensemble will increase their role as the settlement backbone for Hong Kong’s digital finance infrastructure. More tokenized assets → more settlement flow → more custody and clearing revenue. HSBC is positioned as the “house bank” of Hong Kong’s Web3 buildout.

- Harvest Global Investments / Bosera Asset Management (Holdings via parent companies): As state-linked managers dominating Hong Kong’s spot crypto ETF market, these firms are the canary in the coal mine for Mainland participation. If AUM in their Hong Kong-listed ETFs accelerates beyond current levels, it signals tacit capital flow permission from Beijing. This is the trigger for the Southbound Connect thesis.

- Circle (via USDC reserve growth in Hong Kong): If Hong Kong stablecoin licenses (pending Q1 2026) go to major players like Circle or local banks issuing HKD stablecoins, USDC-HKD conversion becomes a natural on-ramp for tokenized asset trading. More HKD stablecoin issuance → more USDC demand → more reserve growth for Circle’s Treasury backing. 👉 Trade on Robinhood

Watchlist:

- Feb 2: Bank of Japan (BoJ) Summary of Opinions (Jan meeting)

- Feb 4–5: ECB Governing Council monetary policy meeting

- Feb 5–6: Digital Assets Forum 2026, London

- Feb 9: Liquidity Summit 2026, Hong Kong

- Feb 10–12: Consensus Hong Kong (CoinDesk)

- Feb 11: US CPI (Jan) release

- Feb 12: US PPI release

- Feb 12: FCA consultation on applying handbook rules to cryptoasset firms

- Feb 17–21: ETHDenver 2026

- Feb 18: FOMC minutes for Jan 27–28 meeting

- Feb: CLARITY‑style market‑structure bills and stablecoin implementation

- Q1’26: Kraken IPO window

- Q1’26: Hong Kong stablecoin licensing regime

- Q1’26: Singapore stablecoin framework launch

- Q1’26: Bitmine MAVAN (Made-in-America Validator Network) rollout

Market signals

- xAI wants AI to trade crypto. Link

- CoinDesk’s new report. Link

- Deutsche Börse’s 360T plugs Bitpanda into FX network. Link

That’s it for now.

Marc & Team