the first on-chain M&A

Hey, it’s Marc,

WE keep a running list of how institutions actually use blockchain. Not what they announce. What they do. Yesterday, Franklin Templeton added something new to that list.[RELEASE]

They bought a crypto team. Normal. They launched a new division. Fine. But here’s the part that matters: they paid for part of the deal with BENJI tokens. Their own tokenized money market fund shares. On-chain. Earning yield.

A $1.74 trillion asset manager just used a blockchain token to settle a corporate acquisition.

Let’s unpack.

The Signal: Major financial companies are now using digital assets to conduct real, everyday business deals. Most importantly, they are building their own plumbing rather than renting.

👉PRO: Download the PDF below

What happened

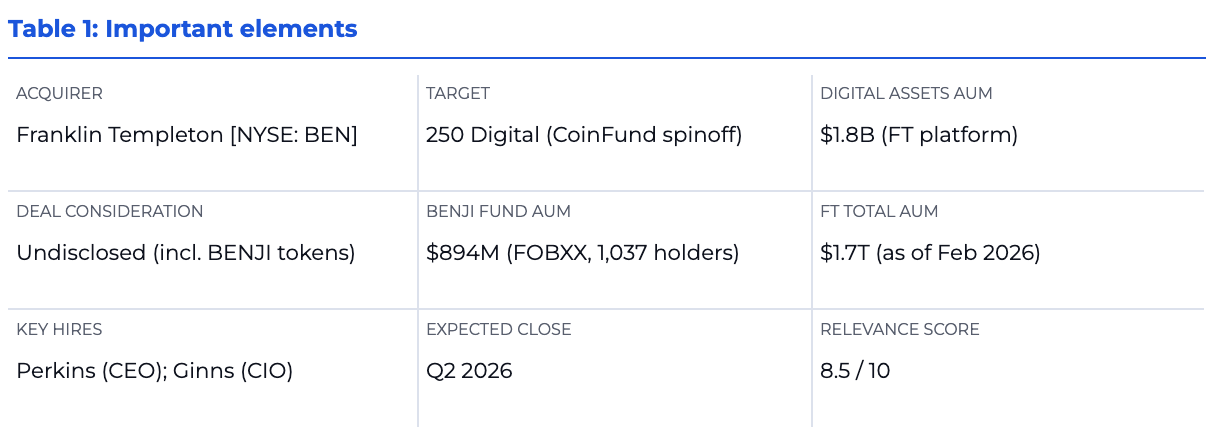

On April 1, 2026, Franklin Templeton ($1.74T AUM) announced the acquisition of 250 Digital, an active digital asset management firm spun out of CoinFund. The deal includes 250 Digital’s full investment team and all liquid crypto strategies previously managed by CoinFund. Financial terms were not disclosed. [RELEASE]

Franklin Templeton is using BENJI tokens as part of the payment consideration. BENJI tokens represent shares in Franklin’s OnChain U.S. Government Money Fund (FOBXX), which holds $864M in AUM and currently yields 3.58% (7-day effective).

Zooming in: The deal forms a new division, “Franklin Crypto,” led by Christopher Perkins (ex-Citigroup, 13 years in TradFi) and Seth Ginns as CIO (ex-Jennison Associates/PGIM, 17 years). It reports to Sandy Kaul, Franklin’s Head of Innovation. The deal is expected to close in Q2 2026.

Stepping back: Franklin has been expanding its Benji platform and its money market fund FOBXX to Canton Network, Solana, Stellar, Base and also in the European markets.

Why it matters

- The acquisition of product: This is not an AUM acquisition. CoinFund’s liquid strategies are relatively small by TradFi standards. What Franklin bought is a leadership team that cannot be assembled from scratch. Perkins spent a decade at Citi running global futures, clearing, and FX prime brokerage. He’s testified before Congress on crypto market structure. He sits on the CFTC’s Global Markets Advisory Committee. He co-invented CESR, the first crypto interest rate benchmark. Ginns was an angel investor in Coinbase in 2012, two years before Ethereum’s ICO, and ran public growth equities at Jennison Associates for 18 years. They’re the rare operators who are fluent in both languages: derivatives clearing and token economics, SEC filings and DeFi governance.

- Active management is the next institutional battleground. Most crypto investing right now is passive. You buy a Bitcoin ETF and you’re done. That works. But it’s not interesting. The interesting part is coming next: actually picking tokens, finding yield, moving across chains. That’s where the real money gets made and where almost nobody is focused yet. Franklin is building for that. Everyone else is still building the thing that already exists.

- This is the first M&A deal settled on-chain. Paying with BENJI tokens is a structural improvement over how corporate payments work today. Wire transfers are slow, opaque, and expensive. BENJI eliminates that friction entirely. Transactions settle on-chain instantly, with verifiable proof of transfer built in. There’s no escrow delay, no T+2 settlement window, and no opportunity cost from cash sitting idle. More importantly, recipients start earning yield from the moment funds arrive. That’s a fundamental shift. A tokenized asset is functioning as an active medium of corporate exchange, not just a store of value. Franklin didn’t just complete a transaction. It demonstrated a new financial primitive: money that works while it moves. This also proves the tokenization thesis.

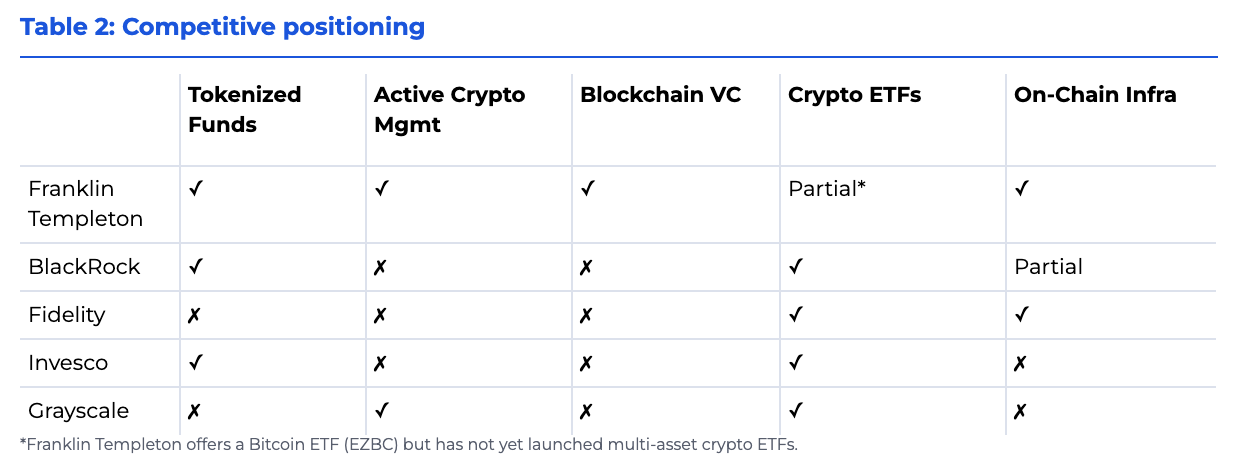

- The 2026 arm race. BlackRock’s BUIDL is at $2.2B and dominant but it is dominant on Ethereum, Solana and BNB Chain. State Street and Galaxy are racing to launch SWEEP on Solana with a $200M Ondo seed. Fidelity launched its own stablecoin (FIDD) and is building a closed-loop ecosystem. Franklin’s counter is multi-chain depth: BENJI runs on Stellar, Polygon, Arbitrum, Avalanche, Aptos, and BNB. That is a distributed infrastructure. Couple that with active management capabilities from 250 Digital and you have something none of the others have yet: a full-stack digital asset factory spanning passive indexing, venture, and active liquid strategies.

Investor Alpha

There is no more crypto story. Crypto is a part of it. The BENJI payment validated the thesis that tokenized money market shares can replace cash in corporate transactions.

- Franklin Resources (BEN): If Franklin Crypto captures institutional active crypto flows the way IBIT captured passive Bitcoin demand, this reprices. Franklin Templeton is actively building its blockchain rails and results will compound through the cycle. 👉 Trade on Robinhood

- Coinbase (COIN) and BNY Mellon (BK): Franklin Crypto’s active strategies require custodial infrastructure and exchange access, Coinbase Custody, BNY Mellon and Coinbase Prime are the default institutional stack. 👉 Trade on Robinhood

- Galaxy Digital (GLXY / BRPHF): Galaxy’s partnership with State Street puts them on the competing SWEEP fund, but Galaxy also benefits structurally from any growth in institutional active crypto AUM. 👉 Trade on Robinhood

Our Take

Every headline will say “Franklin buys crypto team.” But, the interesting read is how all the pieces connect. BENJI gives them the on-chain settlement layer. Perkins and Ginns give them the active management engine. The blockchain VC portfolio gives them deal flow and ecosystem intelligence in the blockchain space. Franklin itself has institutional distribution. This makes them powerful in the race of actively managed digital asset strategies.

But here’s the part I keep coming back to. The BENJI detail. Franklin used its own tokenized money market fund shares to pay for a corporate acquisition. We previously mentioned the usage of money market funds for collateral and now it is also being used for settlement. This expands the playbook of tokenised funds and hence competes with bank deposits and T-bills for a seat at the institutional treasury table.

Bottom line: Franklin bought a team, launched a brand, and stress-tested its own tokenization product, all in one transaction. We will call this acquisition a strategy memo.

51 Intelligence Stack: Recommended Reading

Watchlist:

- Apr 28–29: FOMC meeting. Second rate decision window

- May 5–6: Next FOMC policy meeting after April

- May 5-7: Consensus Miami and the release of Money Movement Report

- Mid-May: Kevin Warsh expected to take over as Fed Chair

- Jul 1: MiCA universal deadline

- Q1-Q2 2026: SEC final decision on Nasdaq tokenized trading rule change (SR-NASDAQ-2025-072)

- H2 2026: DTCC tokenization pilot launch

That’s it for now.

Missed last week? Access all our CEO notes here.

Marc & Team