Fidelity goes on-chain

Fidelity doesn't do crypto. It manages $6.8 trillion. So when the 79-year-old asset manager launched its own stablecoin on January 28, the game fundamentally changed.

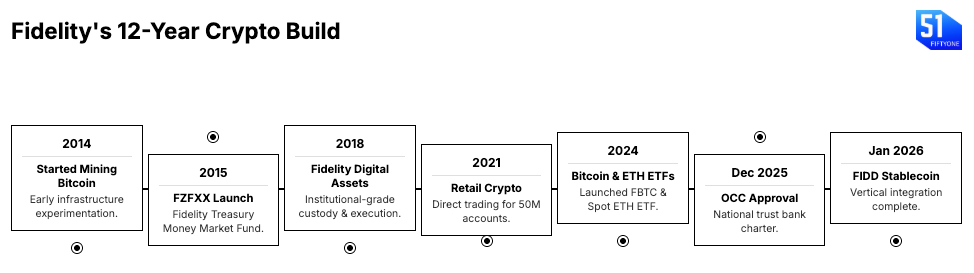

On January 28, 2026, the second-largest asset manager in America launched FIDD, a dollar-pegged stablecoin that Fidelity issues, distributes, and custodies in-house. [PRESS RELEASE].

For the first time, a titan with a national trust bank charter, the highest tier of federal oversight, is offering 24/7 dollar settlement on Ethereum. Let’s unpack.

👉PRO: Download the PDF below

What happened

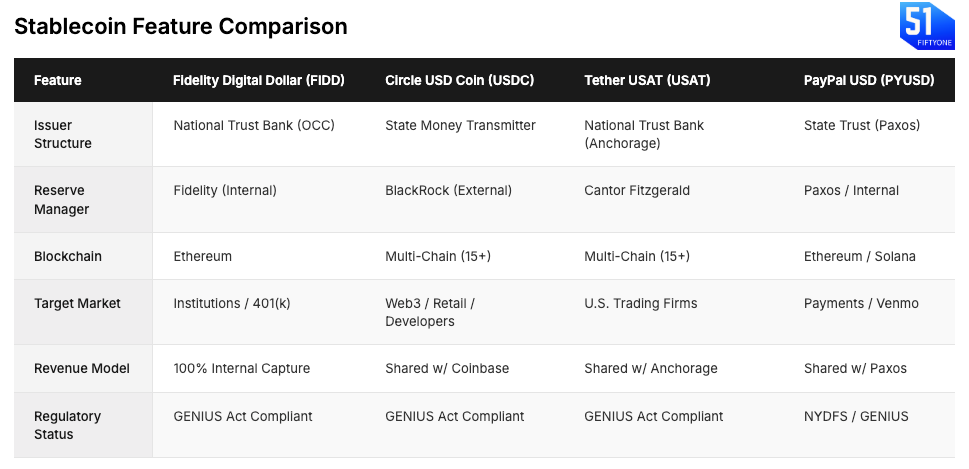

Fidelity Digital Assets, National Association (a federally chartered national trust bank and a G-SIFI) launched FIDD: a 1:1 USD-backed stablecoin, live on Ethereum mainnet. Eligible customers can buy or redeem directly through Fidelity platforms, with daily disclosures of reserves, a transparency standard that exceeds rivals like Circle (USDC) and Tether (USDT).

Be smart: By using a national trust bank structure, Fidelity bypassed state-by-state money transmitter licensing, opting instead for direct OCC oversight. The token reserves sit in cash, short-term Treasuries, and qualifying repos. Listing on major exchanges is expected.

By the data: As of January 2026, stablecoins hit $316 billion in market cap with $45 trillion in annual transaction volumes, dwarfing Visa’s $14 trillion in fiscal 2025.

Zooming in: Fidelity has completed full vertical integration. The Fidelity Digital Assets bank issues the token. At the same time, Fidelity Management & Research (FMR) manages the reserves in-house. Unlike competitors like Circle and Paxos, Fidelity combines FIDD with its tokenized money market fund, the Fidelity Treasury Digital Fund (FYHXX). This pairing creates an internal liquidity engine, acting like a shadow central bank.

When clients need cash, Fidelity automates the redemption of yield-bearing FYHXX shares. It instantly mints FIDD against Treasury collateral. This setup allows for flexible, 24/7 liquidity. It effectively turns US sovereign debt into private digital currency. This all happens within a closed system, avoiding the T+1 settlement delay of traditional banking.

Stepping back: Fidelity has been building crypto infrastructure for over a decade, and each step created what they needed to run a FIDD stablecoin business from top to bottom: secure storage, trading systems, regulatory approvals, and distribution channels.

Zoom out: The $316B stablecoin market is a duopoly shaped by regulatory differences. Tether (offshore/high-risk) holds $187B. Circle (onshore/compliant) has $72B. Fidelity’s entry brings together Tether’s integration and Circle’s compliance and distribution. The nationally chartered trust bank lets stablecoins be issued across the country. It doesn’t require state licenses. Federal oversight covers reserves, and there are clearer rules for digital assets.

The GENIUS Act stops Circle and Tether from competing with bank deposit rates. It also prevents large outflows from the banking system. This setup boosts Fidelity’s ecosystem advantage. Clients can hold FIDD for instant settlement and then move to Fidelity’s tokenized money market funds when they want yield.

Why it matters

Fidelity becomes a shadow central bank: FIDD stablecoin acts less like a consumer payment token and more like a fast collateral and settlement tool for institutions. As derivatives markets use stablecoins for margin, Fidelity’s federally chartered role in “settlement as a service” and “collateral agency services” lets it manage daily collateral flow. This flow involves hedge funds, corporates, and pension funds, areas usually led by JPMorgan and BNY Mellon.

The variation margin opportunity is real: The most tangible institutional use case is derivative margin. Traditionally, posting margin means keeping large cash buffers and pre-funding accounts at CCPs and FCMs. With FIDD as collateral, these buffers can be optimized. Margin can move on-chain within minutes. This allows firms to meet intraday and end-of-day margin calls almost in real-time. This change cuts liquidity drag. It tightens funding and risk management. Also, it lets active derivatives traders recycle collateral anytime.

The economics of vertical integration: Circle’s business model has a fatal leak: distribution costs. To access Coinbase’s users, Circle pays out roughly 50% of its interest income on platform assets. Fidelity pays zero. They own the issuer (FDA), the manager (FMR), and the distribution (50M retail accounts). In a commodity business like cash, the lowest cost producer wins. If Fidelity captures just $10B in float at a 4.5% yield, they retain the full $450M in annual revenue. The circle would have to split that. Wall Street knows they can't compete on price against a player with zero marginal cost.

The distribution moat: Fidelity leveraged the most underestimated advantage in financing existing customer relationships by skipping the distribution model that forces Circle, Tether to work with exchanges, giving Fidelity 100% margin retention, while maintaining the regulatory legitimacy Tether lacks through its OCC-supervised national trust bank charter and direct access to 50M retail accounts plus $17.5 trillion in institutional assets.

Investor Alpha

By vertically integrating issuance, custody, and distribution, Fidelity has driven the marginal cost of stablecoin revenue to zero. Capital is likely to rotate away from entities dependent on net interest margin (NIM) arbitrage and toward the underlying settlement infrastructure that benefits regardless of who issues the dollar.

- BlackRock (BLK): BlackRock manages Treasuries for USDC (through Circle). Growth in FIDD and the broader stablecoin market → more Treasury demand → more AUM under management. Additionally, if tokenized repo gains traction, BLK’s iShares Treasury holdings become settlement layer collateral. 👉 Trade on Robinhood

- BNY Mellon (BK): BK is the infrastructure layer in this cycle. FIDD, USDC, USAT all require institutional-grade custody and settlement services. BK provides that plumbing to every major issuer. As on-chain settlement scales from $316B to $1T+, custody fees compound. BK wins through volume. 👉 Trade on Robinhood

- Fidelity (FDX): Fidelity captures both the issuer margin (spread on FIDD issuance/redemption) and the ecosystem lock-in (FIDD + FYHXX creates switching costs). Additionally, Fidelity’s $6.8T AUM gives it distribution advantages over competitors. 👉 Trade on Robinhood

- Long Ethereum (ETH): Fidelity didn’t build a private blockchain; they chose the Ethereum mainnet. This is the ultimate validation of ETH as the global settlement layer. Every FIDD transaction burns gas (ETH), converting Fidelity’s institutional volume into deflationary pressure for the network, regardless of which stablecoin wins the issuance war. 👉 Trade on Robinhood

Watchlist:

- Mar 11: US CPI (Feb) release – critical for Fed rate cut expectations

- Mar 17–18: DC Blockchain Summit (Chamber of Digital Commerce)

- Mar 18: FOMC Interest Rate Decision & Summary of Economic Projections

- Mar 24–25: Next Block Expo (Warsaw)

- Mar 24–26: Digital Asset Summit (DAS) (New York City)

- Mar 25: Crypto Assets Conference (#CAC26 Frankfurt)

Appendix:

- FIDD - Fidelity Digital Dollar: A stablecoin launched by Fidelity Investments in January 2026, pegged 1:1 to the US dollar and backed by cash and short-term US Treasuries.

- G-SIFI - Global Systemically Important Financial Institution: A designation by international regulators for financial institutions whose failure could trigger a global financial crisis, requiring them to maintain higher capital buffers and face stricter oversight.

- OCC - Office of the Comptroller of the Currency: A US federal agency that charters, regulates, and supervises national banks and federal savings associations.

- FMR - Fidelity Management & Research (Company): The parent company of Fidelity Investments, one of the world’s largest asset management firms.

- FDA - Fidelity Digital Assets: Fidelity’s division that provides cryptocurrency custody, trading, and related services to institutional investors.

- NIM - Net Interest Margin: A profitability metric that measures the difference between interest income generated by banks and the interest paid to depositors, expressed as a percentage of interest-earning assets.

- CFTC - Commodity Futures Trading Commission: An independent US federal agency that regulates the derivatives markets, including futures, options, and swaps.

That’s it for now.

Missed last week? Access all our CEO notes here.

Marc & Team