Coinbase is no longer a crypto exchange

Hey, it’s Marc.

Stop calling Coinbase a crypto exchange. As of yesterday, that label is dead.

At its System Update event, Coinbase did not launch features. It dismantled categories. Stocks, derivatives, prediction markets, stablecoins, and tokenized real-world assets were all pulled into a single on-chain environment, settled on Base, collateralized by USDC, and distributed through one wallet. [MORE]

Let’s unpack. (full PDF at the bottom)

Get your brand in front of 100k+ decision makers in digital assets.

What happened

On December 17, 2025, Coinbase introduced a series of incremental features. Their advanced five core initiatives are:

- Zero-Fee Stock & ETF Trading (24/5)

– U.S. equities and ETFs, with thousands more planned

– Designed for distribution, not margin capture - International Equity Perpetual Futures (ex-U.S.)

– Perps for stocks, launching early 2026

– Unlocks global, continuous liquidity for equities - Regulated Prediction Markets (via Kalshi)

– Elections, macro outcomes, rates, and events as tradeable contracts

– Structured as financial markets, not gambling - Coinbase Tokenize (Institutional Tokenization Stack)

– End-to-end issuance, custody, compliance, and secondary trading

– Designed for off-chain assets moving on-chain at scale - Stablecoin-as-a-Service (“Custom Stablecoins”)

– Enterprises can issue branded digital dollars

– Fully backed 1:1 by USDC, custodied and compliant at Coinbase

These launches are tightly coupled. None are standalone products.

Zooming in: The “System Update” announcements reveal a deliberate strategy to converge three historically distinct asset pillars:

- Spot Equities & ETFs: The traditional ownership of corporate cash flows, representing the bedrock of household wealth.

- Digital Assets: Sovereign-grade cryptocurrencies (BTC, ETH) and utility tokens, representing the new internet economy.

- Event Contracts (Prediction Markets): Instruments for hedging against real-world outcomes, representing the “information economy.”

The strategic value lies in the cross-collateralization of these assets. In today’s system, stocks can’t be used as instant collateral for things like election or sports contracts because markets settle slowly and don’t connect. Coinbase’s on-chain setup is designed to let assets move and be reused in real time, making that kind of cross-market use possible.

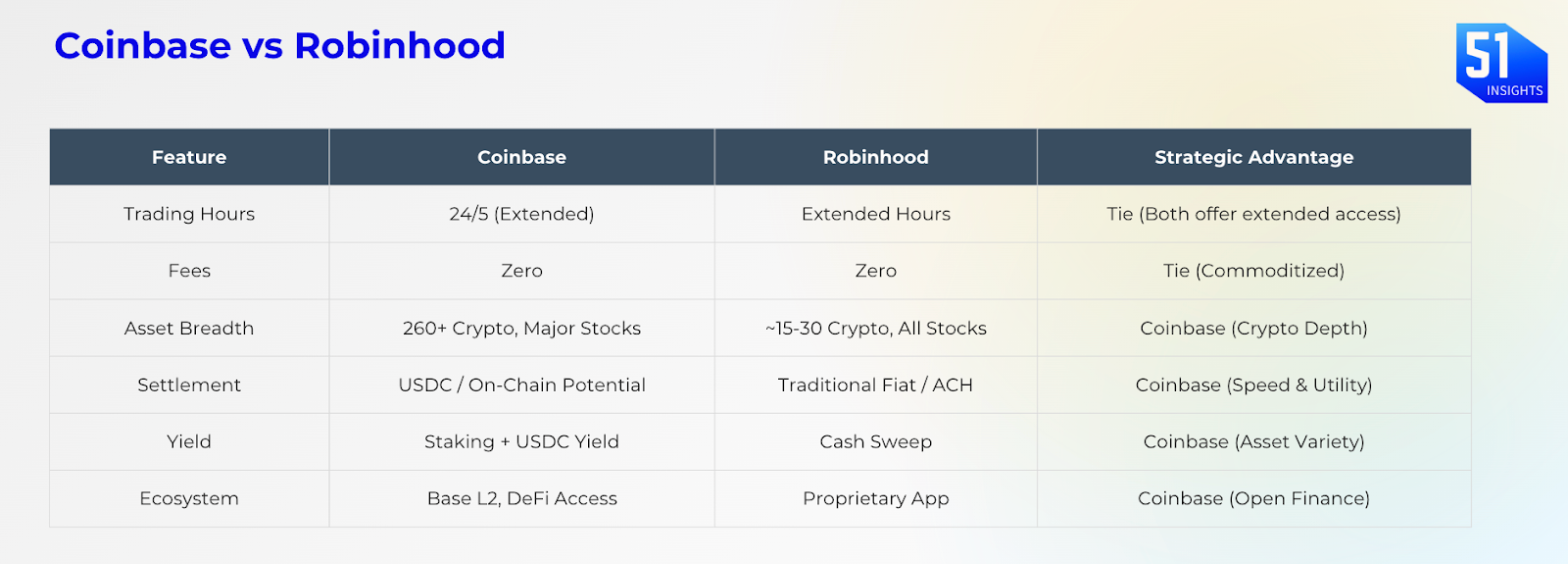

Be smart: Unlike competitors such as Robinhood, which rely on traditional clearinghouses and third-party crypto custodians, Coinbase is building its own vertical stack with Base blockchain. The blockchain serves as the settlement layer, while USDC acts as the medium of exchange.

The revenue mystery: Coinbase has explicitly stated that zero-commission stock trading is a permanent offering but has declined to detail the revenue model.

Three revenue paths stand out:

- Subscriptions: Free stock trades pull users into Coinbase One, where monthly fees cover crypto trading perks, data tools, and account protection, turning transactions into a relationship business.

- Interest on cash: Keeping more customer dollars on the platform lets Coinbase earn interest on idle balances, a proven profit engine for brokerages in higher-rate environments.

- Order flow economics: Zero-fee stocks usually rely on routing or internalizing trades; whether Coinbase uses this or avoids it to protect its brand will determine how much pressure falls on subscriptions and interest income.

The alpha: Coinbase’s move into prediction markets through its partnership with Kalshi may be its boldest step yet. By using a federally regulated venue, Coinbase can offer U.S. users a legal way to trade on real-world events, something that has driven huge demand offshore but remained off-limits at home.

The most exciting thing in our view? Stablecoin-as-a-service. Here’s why + our alpha + the full PDF

Why it matters

The "Everything Exchange": For decades, liquidity has been trapped in silos. Stocks live in one venue, commodities in another, and crypto in a third. Coinbase just broke those walls. By moving stocks, prediction markets, and treasuries onto a single ledger (Base), they allow assets to be cross-collateralized in real time. You can now theoretically use your Apple stock as collateral to hedge an election outcome on Kalshi, instantly. This velocity of capital is the new competitive moat. Unlike Robinhood, which relies on legacy clearinghouses, Coinbase owns the vertical stack—the exchange, the settlement layer (Base), and the currency (USDC).

The Branded Money Revolution: The most slept-on announcement is Stablecoin-as-a-Service. This is not just about payments; it’s about brands becoming their own central banks. Businesses can issue branded tokens (e.g., “StarbucksCoin”) backed 1:1 by USDC and other liquid assets. Historically, corporate rewards (Starbucks Stars, airline miles) were liabilities trapped in proprietary databases. By converting these into on-chain stablecoins, brands turn liabilities into liquid assets. A “DeltaDollar” can now be instant collateral in DeFi, swapped for “UberCash,” or sent globally. This unlocks billions in dormant value currently stuck in loyalty programs.

For Brands: It turns a cost center (loyalty) into a liquid asset that captures float and reduces credit card fees.

For Coinbase: It’s a massive revenue engine. They earn custody fees, transaction fees, and a spread on the float for every “DeltaDollar” or “AmazonCoin” minted. This kills the white-label stablecoin market by offering regulatory trust at scale.

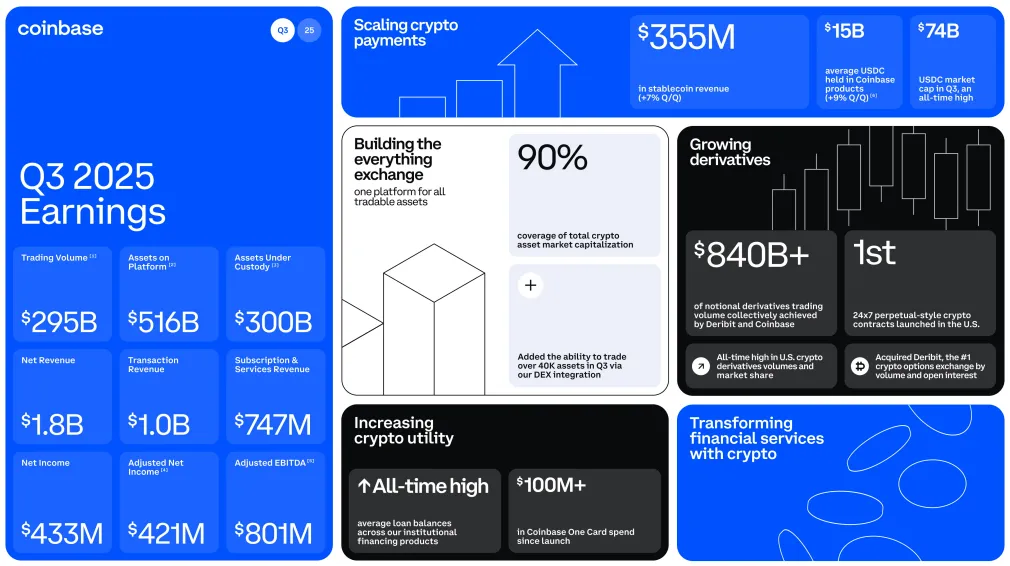

The Revenue Pivot: Coinbase is decoupling from crypto volatility. The revenue mix shifts from unpredictable transaction fees to NII, subscription, derivatives, and RWA servicing fees – and recurring subscription revenue (Coinbase One). We also expect sizable interest income on the USDC float that branded stablecoins will generate.

Alpha

The "System Update" positions COIN to compete directly with traditional brokerages and fintechs, but with a structural cost advantage: the blockchain back-end. We believe the market is underestimating the "stickiness" of the new ecosystem. Once a user holds stocks, stablecoins, and prediction contracts in one interoperable wallet, the switching costs become prohibitive. What some investors do:

Buy COIN: The “Everything Exchange” positioning will increase the TAM of Coinbase from “crypto traders” to “all investors.” However, bearish arguments persist regarding margin compression. As Coinbase competes with Robinhood (zero fees) and DeFi (low fees), its “take rate” per transaction must decline. The company is betting that volume growth (velocity) will outpace the decline in pricing power.

Watch Robinhood (HOOD): Competitive pressure will mount. If Coinbase succeeds in cross-collateralizing assets, Robinhood’s legacy infrastructure will look slow and capital inefficient.

Watchlist:

- Dec: USAT launch by Tether (expected)

- Dec: Clarity Act (H.R.3633) Senate vote (expected)

- Dec 31: Europe’s MiCA full enforcement (Austria, Germany, and Spain) ends

- Jan 1: Basel Committee crypto capital standards implementation in Hong Kong

- Jan’26: SEC Crypto Innovation Exemption

- Jan’26: Spot crypto ETF approvals for altcoin

- Q1’26: Kraken IPO

- Q1’26: Hong Kong Stablecoin licensing

- Q1’26: Singapore Stablecoin framework

Market signals

- SoFi just became the first nationally chartered U.S. bank to issue a stablecoin on a public blockchain. Link

- NYSE Owner Is Said in Talks to Invest in Crypto Firm MoonPay. Link

That’s it for now.

Marc & Team

Download the PDF