Circle is about to lose 10% of its yearly revenue

Hey, it’s Marc.

We're witnessing one of the biggest showdowns in crypto right now.

Hyperliquid’s move to launch its own stablecoin isn’t just about cutting Circle out of $200M in annual yield is the opening salvo in a much bigger war: keeping crypto out of the hands of corporate chains and their profit machines.

Step 1: The setup

Hyperliquid, a DEX with $700M TVL and more daily protocol revenue than Ethereum and Solana, has $5.5B in stablecoins sitting on it today.

Most of that is Circle’s USDC.

Which means Circle quietly collects the interest, at current rates that’s ~$200M a year (almost 10% of their revenue)

Zero flows back to Hyperliquid.

Step 2: The twist

This is why Hyperliquid just proposed its own native stablecoin: USDH.

But this isn’t “just another stablecoin.”

Whoever issues USDH must share the yield back to the ecosystem:

share the yield with the ecosystem, paying validators, funding the assistance pool, and buying back HYPE.

That revenue could grow to $1B+ a year as stablecoin balances scale.

where it gets interesting:

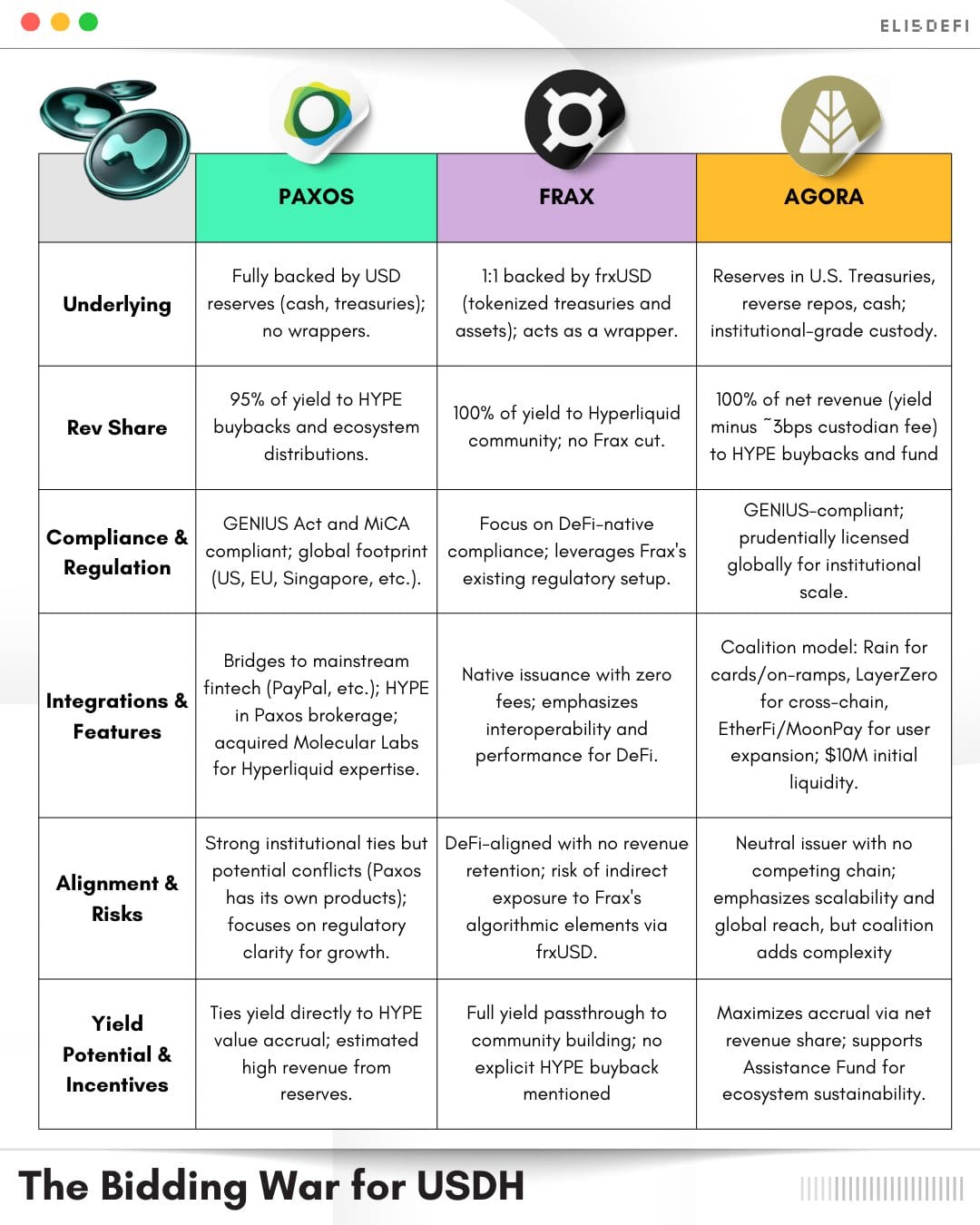

Multiple teams are now battling to become the issuer of this stablecoin:

(and give 95-100% of their stablecoin profits back HYPE holders!!)

- Paxos (Binance’s old partner, regulated under MiCA + GENIUS)

- Agora (MoonPay, EtherFi, LayerZero Labs , Rain coalition) are the frontrunners.

- Sky (former MakerDAO)

- Frax

Ethena Labs & others are circling too as more bids are coming.

And now the crazy part

Stripe, with its new layer 1, Tempo may bid too (not confirmed).

Tempo is led by Matt Huang & @Paradigm, who investors in Stripe, Tempo, MoonPay, and Agora.

Meanwhile, Jeremy Allaire, CEO of Circle, says: "don't believe the hype"

Circle continues to compete with its own USDC on hyperliquid.

All this is HUGE for 2 reasons:

1) Circle IPO’d 4 months ago at a $19B valuation.

Investors were sold on the idea of predictable, compounding revenue from USDC reserves.

Now that cash machine is under fire.

Margins are already thinning, which is why Circle launched its own L1, Arc.

2) The bigger story: We’re in an all-out war for who owns the payment rails of the future.

Stripe's launch of Tempo has sparked one of the biggest debates in crypto I've seen on decentralization, credible neutrality, and whether crypto's ethos is about to get swallowed by corporate greed.

The battlefield now:

- Stripe (Tempo)

- Circle (Arc)

- Google (GSUL)

- Tether.io (Plasma)

- Stable

vs. Ethereum (has 60% of all stablecoin volume)

Meanwhile, banks, Visa and Mastercard's foundation is under attack.

The opportunity is enormous. Probably multiple trillions in value 10y down the road.

And if Stripe bids for Hyperliquid’s USDH, this isn’t just a fight over one protocol’s revenue.

It’s corporate blockchains vs. decentralized rails, head-to-head.

So YES: Circle could lose 10% of its yearly revenue.

But the bigger picture?

This could be the inflection point for crypto’s future.

That’s all for now, folks.

Take care,

Marc

🚀 Work with us: We create pioneering thought leadership that helps digital asset and technology companies lead the conversation, earn trust and win business.