The first nation to run on USDC

Hey, it’s Marc & the 51 team,

Every country has a central bank. Bermuda just chose Circle instead.

At Davos, Premier David Burt announced a partnership with Circle and Coinbase to build what he called “the world’s first fully on-chain national economy.” Tax payments. Merchant settlement. Government disbursements.

All on USDC, all on Coinbase’s Base network. It’s either the most pragmatic monetary decision of the decade — or the most reckless. Let’s unpack. [RELEASE]

Island nations live in the margin. Bermuda, with $780B in insurable risk, has no room for mediocrity. For 30 years, it survived via regulatory arbitrage, reinsurance dominance, captive insurance innovation, and then digital assets.

👉PRO: Download the PDF

What happened

On January 19, 2026, the Government of Bermuda formally partnered with Circle and Coinbase to transition to a “fully on-chain national economy.” [RELEASE]

Why Bermuda had to act: Since 2008, large global banks have steadily pulled back from smaller markets, cutting cross-border banking ties that no longer justify rising compliance costs. For offshore jurisdictions, access eroded not because of risk, but because scale no longer made the relationship economical. As offshore markets lost banking links faster than onshore ones, Bermuda’s cross-border payments became constrained. The pressure is acute because Foreign Direct Investment (FDI) in insurance and financial services makes up roughly 85% of GDP, while the island depends on constant dollar outflows to fund imports.

Island nations live in the margin. Bermuda, with $780B in insurable risk, has no room for mediocrity. For 30 years, it survived via regulatory arbitrage, reinsurance dominance, captive insurance innovation, then digital assets.

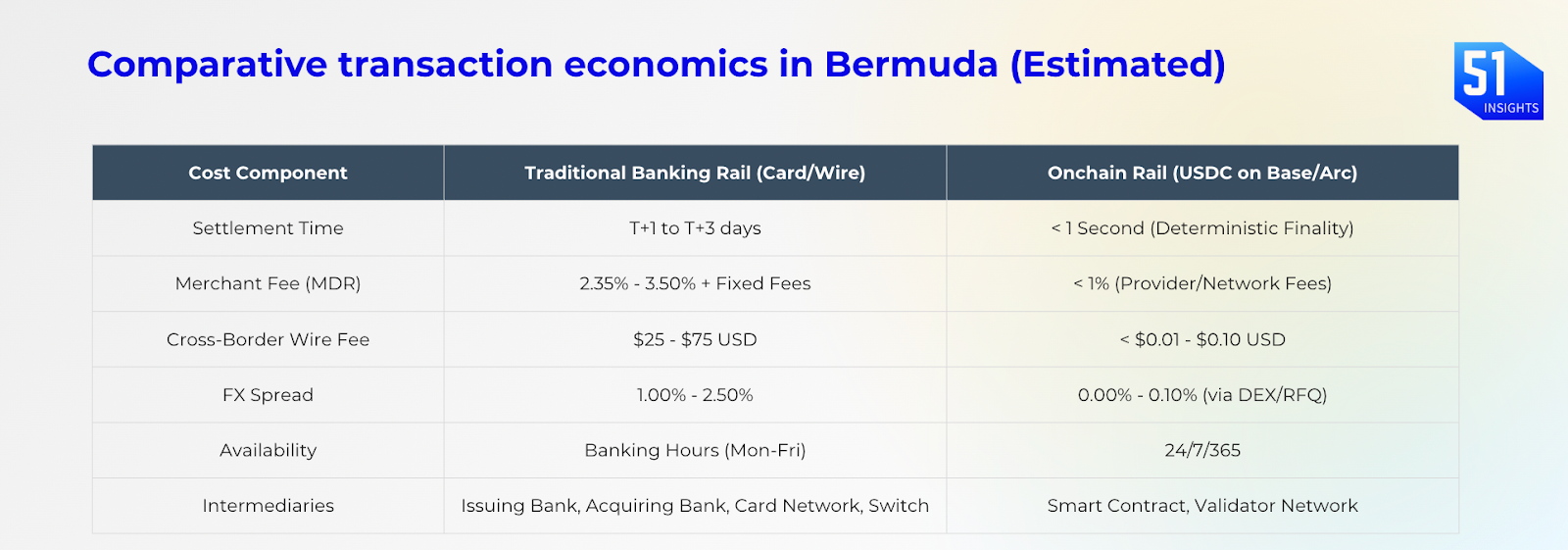

What they built and why this way: Unlike El Salvador’s Bitcoin gamble, Bermuda chose dollar parity and institutional-grade infrastructure. The partnership targets three problems: eliminate correspondent banking delays (payments currently take T+3 to T+5 days); collapse merchant fees (from 3-4.5% to <1%); and unlock $60B in illiquid reinsurance capital trapped in legacy trust structures. The goal is to eliminate the “island tax” of correspondent banking and reduce the cost of capital for its $780B insurance market.

Rails: The government selected Base (an Ethereum Layer-2) as its national settlement layer and USDC as its medium of exchange, rejecting the CBDC model.

Scope: It covers government agency payments, merchant systems, and financial institution tooling. Participation is voluntary, and the partnership is non-exclusive.

Goal: To eliminate the “island tax” of correspondent banking and reduce the cost of capital for its $780B insurance market.

Architecture: Leveraging Bermuda’s 2018 DABA regulation, the system utilizes Decentralized Identity1 (DID) for privacy-preserving compliance, effectively outsourcing the M0 money supply to a regulated private issuer (Circle).

In 2019, Bermuda launched PerseID initiative, a blockchain-based digital identity project in partnership with Shyft Network.

What they’re saying: “Bermuda’s leadership shows what’s possible when clear rules are paired with strong public-private collaboration,” said Coinbase CEO Brian Armstrong.

Bottom Line: Bermuda solved the Island Trap by centralizing with two US corporations.

Why it matters

The correspondent banking problem: Bermuda’s financial system runs on dollar flows — premium payments in, claims and dividends out. For decades, those flows ran through correspondent banks: intermediaries that connect smaller offshore institutions to the global dollar system. After 2008, those relationships became uneconomical for large banks to maintain. Compliance costs rose, transaction volumes stayed small, and one by one the links were cut. What remained was slower, more expensive, and increasingly fragile. Payments that should clear in hours take T+3 to T+5 days. Merchant fees run 3–4.5% on every transaction. For an island economy with no central bank and no domestic dollar supply, every delay and every basis point is a structural tax. USDC ($73.7B in circulation) running on Base changes the equation. Settlement moves from days to seconds. Fees collapse below 1%. And because USDC is fully dollar-backed and regulated, it carries none of the volatility risk like Bitcoin. For a $7.5B economy where 85% of GDP flows through financial services and imports, it is a survival infrastructure.

What happens when the global banking system prices out an entire class of economies: Caribbean and Atlantic island economies have a problem that doesn’t show up in any headline number. Over the past two decades, the world’s biggest banks, JPMorgan, Deutsche, HSBC, have quietly cut ties with island banks. Not because the islands were doing anything wrong. Because the math stopped working. Monitoring a small offshore bank for money laundering compliance costs roughly the same whether you’re moving $10M or $10B. At low volumes, it’s just not worth it.

The result is that Bermuda pays for it on every transaction. A wire transfer into the island costs $40–$100. The US equivalent, sent as USDC, costs $0.10.

When a Bermudian merchant buys goods from Florida, that payment sits in a New York correspondent system for three to five days before it moves. A Singapore merchant doing the same deal settles instantly. Bermuda’s retailers also pay 300–350 basis points more in card processing fees than their US counterparts, because payment processors classify the island as “high-risk international.” That label alone costs the economy an estimated $100M+ a year, just from geography.

Tokenizing $2T in illiquid risk: Bermuda hosts 75% of global Insurance-Linked Securities (ILS). These are catastrophe bonds, capital set aside to cover hurricanes, earthquakes, or cyber events. The money is locked up for one to three years by design. If a pension fund commits $5M, that capital is inaccessible until maturity. That structure broke in 2023. As interest rates rose, investors lost patience with long lockups. The reinsurance market faced a $60B capital gap almost overnight. Traditional funding simply pulled back. Tokenization turns locked, long-dated insurance capital into something flexible: smaller entry sizes, real liquidity, and faster payouts. It brings new capital back into reinsurance without changing the underlying risk.

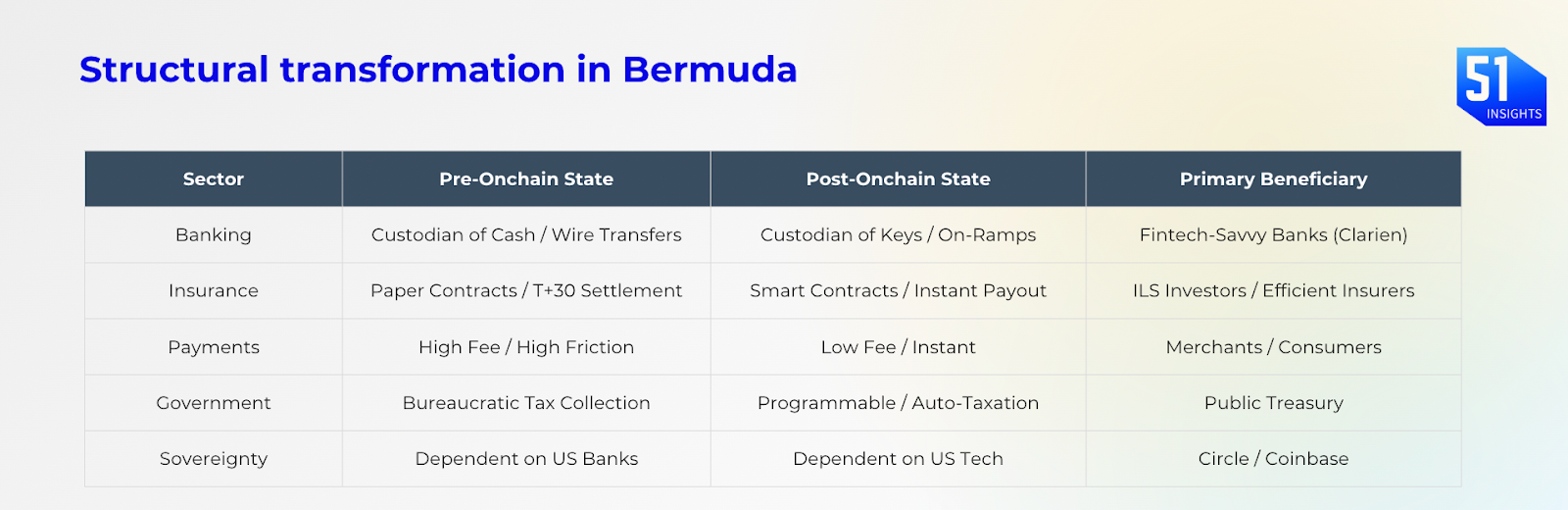

Banks become custodians: Local incumbents (Butterfield Bank, Clarien Bank) face disintermediation. When citizens hold USDC instead of bank deposits, the float migrates to Circle. To survive, these banks can become “Digital Asset Custodians“ and “Compliance Gatekeepers.” The Bermuda Monetary Authority evolves from financial supervisor to code Supervisor, real-time on-chain monitoring of systemic risk.

The risk is real. Bermuda traded monetary resilience for efficiency. USDC can be frozen at the smart contract layer. If Coinbase’s Base Sequencer goes down, the payment system halts. The country is betting that US regulatory stability and Coinbase uptime are more reliable than correspondent banking. That’s probably true — until it isn’t.

Investor Alpha

By tying digital dollars to regulated financial infrastructure, Bermuda shows that private networks can deliver the core functions of money where traditional systems fall short. This is a practical fix for small, open economies (Singapore, Abu Dhabi, Malta and Cayman).

- Long Coinbase (COIN): Coinbase is now de facto sovereign infrastructure provider. Base isn’t just an exchange scaling solution anymore, it’s a national settlement layer. As more jurisdictions adopt similar models, Base becomes enterprise-grade infrastructure with recurring Sequencer fee revenue (not just DEX revenue).

- Watch tokenized risk infrastructure: Protocols bridging DeFi capital to reinsurance markets (MembersCap, Relm, OnRe, Archax-style platforms) are capturing the convergence trade. Tokenized Cat Bonds offer 10-15% yields uncorrelated to crypto market cycles. If the ILS market migrates even 2-3% on-chain over 5 years, that’s $40-60B in new capital formation. These platforms become the infrastructure layer.

- Circle (CRCL): Circle has evolved from a simple stablecoin issuer into a high-margin financial infrastructure provider. is positioning itself as the compliant, “clean” alternative to Tether, specifically targeting institutional settlement and corporate treasuries and now nations as well. Fundamentals show strong USDC growth to $73.7B circulation (29% market share), driving a 66% revenue rise to $740M in Q3 2025, though reliant on reserve interest income. Coinbase dependency adds volatility.

Watchlist:

- Feb 17–21: ETHDenver 2026

- Feb 18: FOMC minutes for Jan 27–28 meeting

- Feb 19: Fed Gov. Bowman Speech

- Mar 1–2: Crypto Expo Europe (Bucharest)

- Mar 11: US CPI (Feb) release – critical for Fed rate cut expectations

- Mar 17–18: DC Blockchain Summit (Chamber of Digital Commerce)

- Mar 18: FOMC Interest Rate Decision & Summary of Economic Projections

- Mar 24–25: Next Block Expo (Warsaw)

- Mar 24–26: Digital Asset Summit (DAS) (New York City)

- Mar 25: Crypto Assets Conference (#CAC26 Frankfurt)

That’s it for now.

Marc & Team

Download the PDF

Decentralized Identity (DID) is a self-sovereign digital ID system where individuals control their own identities, independent of central authorities like governments or companies, using globally unique, cryptographically verifiable identifiers often stored on blockchains. DIDs allow users to manage digital credentials in secure wallets, selectively sharing verified information with trusted parties, which enhances privacy and security by reducing reliance on centralized data stores and preventing single points of failure for data breaches. ↩