Bank of America embraces Bitcoin

Bank of America just capitulated.

After years of avoiding crypto, the second-largest U.S. bank is now greenlighting Bitcoin recommendations for its 15,000 advisors with a 1-4% allocation. [NEWS]

With Washington’s anti-crypto pressure fading, the bank is racing to stop clients from leaving for digital-first competitors. The wall between traditional banking and Bitcoin has officially fallen and the capital floodgates are about to open.

Let’s unpack.

If you have feedback, please reply to this email. – Marc

What happened

Bank of America has authorised its 15,000+ advisors to actively recommend a 1% to 4% portfolio allocation to crypto assets (specifically spot Bitcoin ETFs) for wealth management clients. The formal coverage begins January 5, 2026.

The Vehicles: The bank is limiting recommendations to four specific regulated ETFs:

- BlackRock (IBIT)

- Fidelity (FBTC)

- Bitwise (BITB)

- Grayscale (GBTC)

The biggest asset managers and banks are now officially recommending:

- BlackRock: Already pushing 1-2%

- Fidelity: Suggesting 2-5%

- Morgan Stanley : Recommending 2-4%

- Bank of America: Now targeting 1-4%

The message is clear: Zero exposure is no longer a “conservative” stance.

The thesis: Nancy Fahmy (leads BofA’s investment solutions group) said the shift was driven by “growing client demand.” That’s true, but it’s only part of the story. The deeper motive is defensive. In 2024 and 2025, wirehouses kept losing assets to digital-first platforms and fast-moving RIAs (Registered Investment Advisors) that were willing to offer real crypto advice.

By the data: By 2027, RIAs are expected to surpass Wirehouses (traditional firms like Merrill Lynch, UBS, Morgan Stanley and Wells Fargo) in market share of Advisor Assets (31% vs 28%).

BofA’s move is an attempt to stem that outflow and regain wallet share from the next generation of wealth clients.

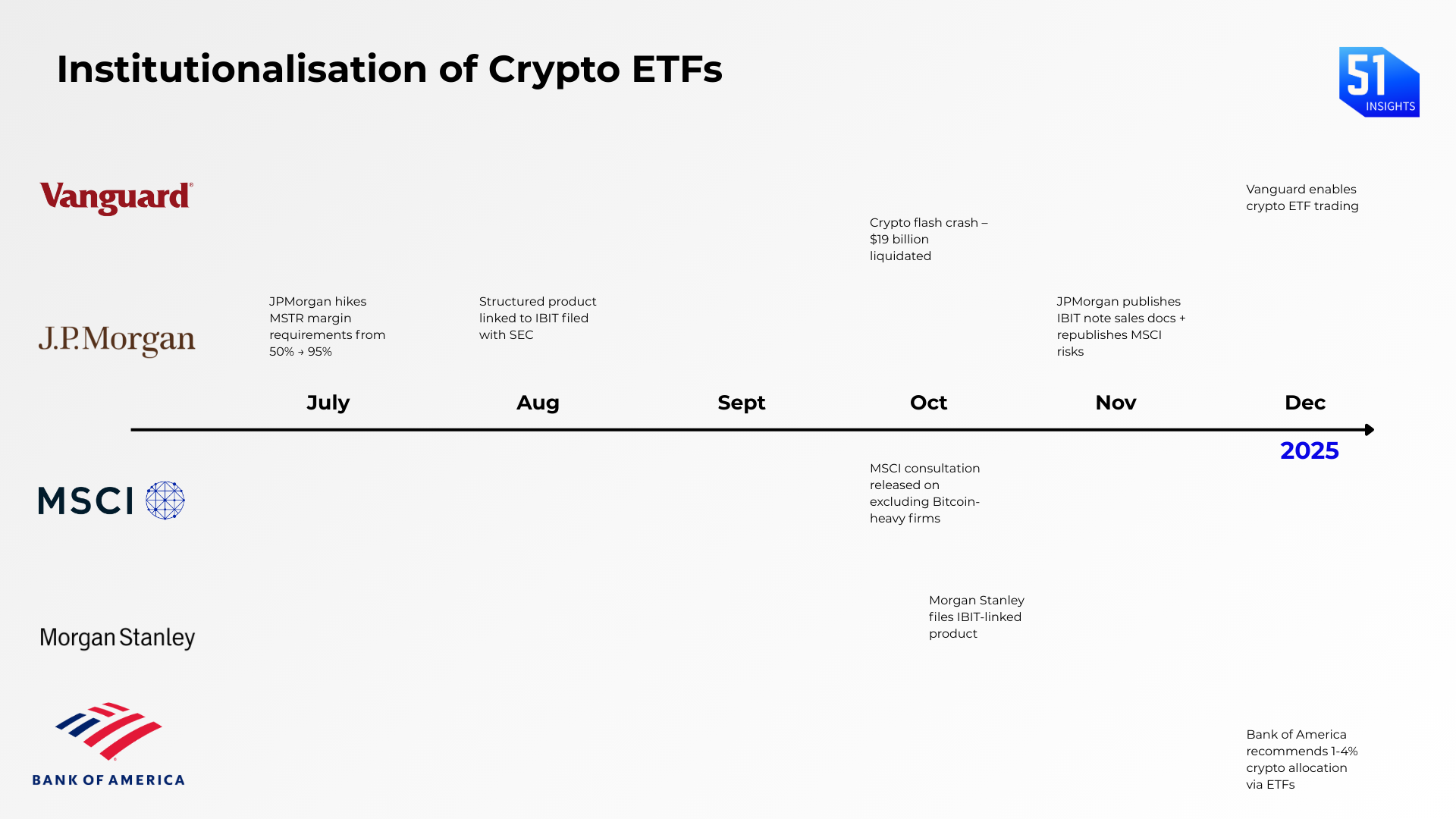

The catalyst: The real shift came from Washington. For four years, banks operated under quiet but aggressive pressure to avoid crypto. That changed on December 1, 2025. The House Financial Services Committee published a 53-page report titled Operation Choke Point 2.0: Biden’s Debanking of Digital Assets.

The report gave banks something they hadn’t had in years: political cover. It showed that regulators had used quiet pressure, not public rules, to block crypto activity.

Key tactics included:

- FDIC “pause” letters: Banks were told to stop all crypto activity. These letters worked like bans but avoided the public rulemaking process.

- OCC “non-objection” hurdles: Banks needed special approval before offering crypto custody or stablecoin services. These approvals were rarely granted, acting as a silent veto.

- “Reputational risk” threats: Regulators warned banks that working with crypto firms could hurt their supervisory ratings, even when no safety issues existed.

Policy expectations for 2026:

- Rescission of SAB 121: Rescinded by the SEC in January 2025. It forced banks to hold dollar-for-dollar capital against custodied crypto, making custody impossible. Removing it clears the path for Citi, State Street, and others to launch full custody services.

- Charter Parity: The new “Crypto Czar” is expected to push for equal treatment between state-chartered crypto banks and federal banks. This would finally let crypto-native institutions plug directly into national payment rails.

- Basel III implementation: In November 2025, the Basel Committee agreed to fast-track a review of how banks must treat crypto on their balance sheets.

Under the current Basel rules, Bitcoin sits in “Group 2” with a 1,250% risk weight. In practice, that means a bank must hold one dollar of equity for every dollar of Bitcoin exposure. The cost is so high that trading or holding Bitcoin simply doesn’t make economic sense.

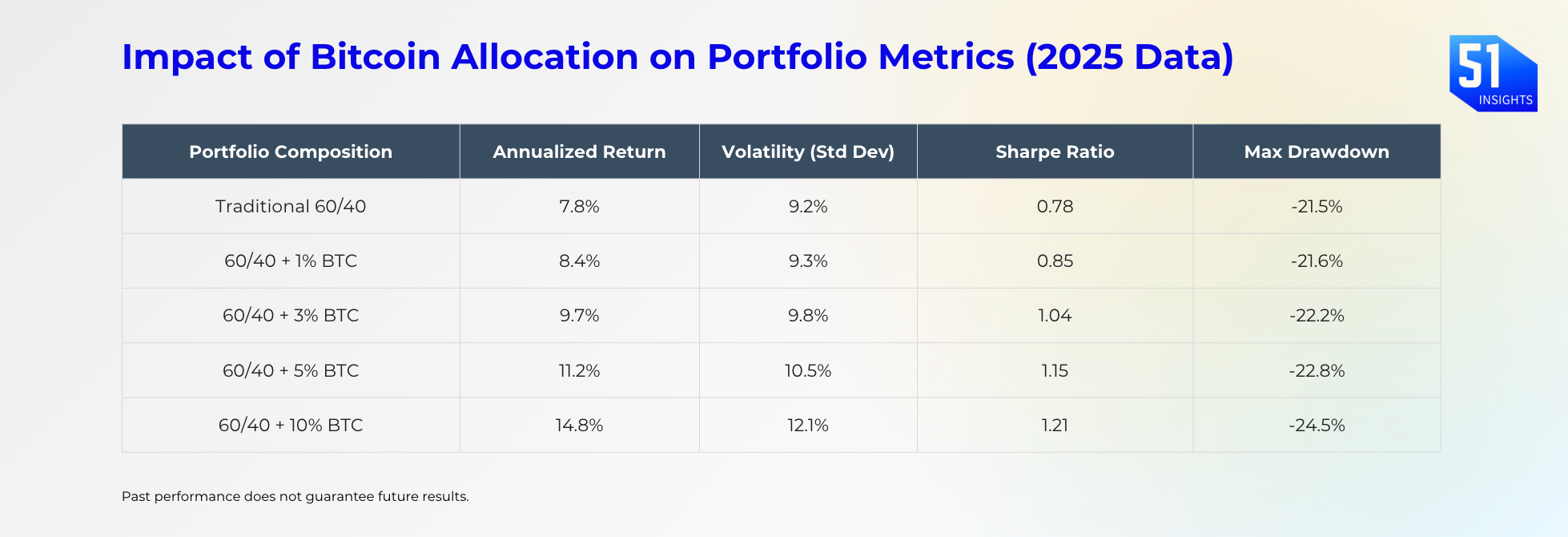

The optimal allocation: A 3% allocation to Bitcoin increased annualized returns by nearly 200 basis points (from 7.8% to 9.7%) while increasing portfolio volatility by only 0.6% (from 9.2% to 9.8%).

🙌 Work with us: We arm financial institutions and digital asset leaders with bespoke research, thought leadership to shape the most important conversations, scale trust, and win business.

Why it matters

- End of reputational risk of crypto ETFs: BofA just moved to neutralise the reputational risk of crypto ETFs by doing the opposite of what everyone expected: incentivising advisors to sell more of them. Overnight, the largest wealth-management firms become a distribution arm for BlackRock and Fidelity’s crypto products. It’s less a crypto bet and more a client-demand concession.

- The Wall of Money: The math is staggering. Bank of America, Morgan Stanley, Wells Fargo, and UBS Americas collectively manage ~$14 trillion. Even a conservative adoption curve moves markets: if just 50% of their client base allocates 1% to crypto, that generates $70 billion in inflows. For context, the entire first year of U.S. spot Bitcoin ETFs attracted roughly $36 billion. We are looking at a potential doubling of flows from a single channel.

Our take: The great rebundling

For the last five years, fintechs and crypto-native firms unbundled the bank. They offered better UI, yield, and access to crypto. But now, the regulatory dam (Basel III) is breaking.

- The Play: G-SIBs (Global Systemically Important Banks) aren’t just going to offer crypto; they are going to internalize it.

- The Result: Custody and settlement – services that crypto startups built entire business models around – are about to become features, not products. Banks will bundle these services into their existing product suites

Investor alpha

The “crypto-native premium” is evaporating. As banks commoditize access, the value capture shifts from exchanges charging high spreads to infrastructure owners and the asset itself. The 2026 cycle will favor regulated incumbents who can bundle crypto with broader wealth management, squeezing margins for standalone exchanges.

Long: BlackRock (BLK). They own the product (IBIT), the largest Bitcoin ETF by market cap, and the institutional rails (Aladdin). As wirehouses open the floodgates, the issuer with the deepest liquidity wins the “winner-take-most” ETF game.

Long: Bitcoin (BTC). The asset remains the ultimate beneficiary of the “Great Synchronization.” A 1-4% allocation becoming standard across $14T in wirehouse assets creates a structural, price-insensitive bid that arguably isn’t fully priced in.

Most people think this is just about “price go up.” It’s not. It’s about access.

This week, $11T Vanguard started allowing clients to buy crypto ETFs. Vanguard is #1 in U.S. retirement savings and index mutual funds. It controls the deepest pool of passive retirement capital.

Trillions of dollars in wealth management capital have been structurally locked out of this market. The gates just swung wide open.

Today’s Market Signals

- European banks led by BNP, ING push ahead on euro stablecoin plan. Link

- Russia is likely to loosen crypto rules. Link

- Fusaka upgrade is live on the Ethereum mainnet. Link

- Kraken acquires Backed Finance. Link

- UK passes bill applying property laws to crypto. Link

Take care,

Marc & team

Download the PDF